DRAW-DOWNS/REMAINING PRINCIPAL/FACILITIES AND CREDIT LINES

This behavior is the case of options where the borrower draws down the agreed remaining principal of loan gradually in accordance with liquidity needs. An example of draw-downs would be a loan applied to the construction industry, where the sum of the total pay-outs is agreed but not the exact payment dates.

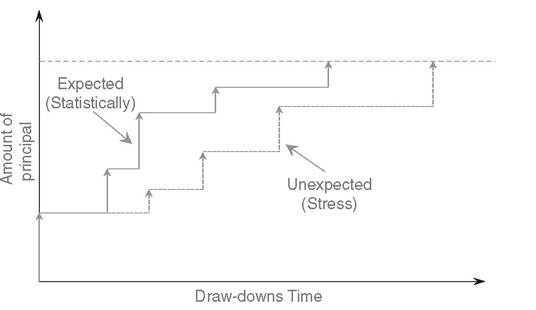

In most instances, the borrower will repay the principal plus the interest after the completion of the project and up to the maturity date.Under normal conditions, credit institutions estimate the payouts based on project plans and statistical observations (see Figure 8.3). Interest payments are not always defined in advance, and thus the expected pattern of “cash ins” depends on future market conditions. Obviously, the value and the evolution of the credit exposure depend on the counterparty's behavior.

Under stress conditions such behavior may not be as expected, e.g., construction projects may slow down or even be postponed and thus the expected draw-downs may be delayed as illustrated in Figure 8.3. In such stress conditions, the credit exposure may be considered as a credit default.2

FIGURE 8.3 Pattern that illustrate the prepayment under statistically normal and stress financial risk conditions

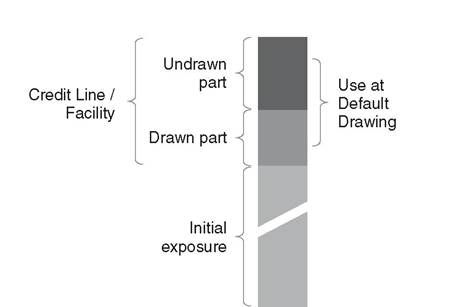

Facilities have similar structure but they are rather short-term credits used mainly to fulfil the current liquidity needs whereas their credit lines define the restrictions and terms3 of the corresponding draw-downs. The drawn part, as illustrated in Figure 8.4, is considered as an additional exposure that could be used by the borrower. The undrawn part is not considered as part of the current exposure but is the maximum future exposure indicating future expected credit loss. The pattern of the facilities/credit lines behavior is the same as of draw-downs except that the principal may or may not be exercised. Under normal conditions, facilities serve the liquidity needs whereas when the counterparty is under stress they can be used to avoid default events leading to the risk of use at default, discussed in the following paragraphs.

The important parameters of such behaviors are the draw-down dates, i.e., PIT time when draw-down happens, the draw-down amount, the maximal draw-down (in case of facility) and the interest rate adjustments.

FIGURE 8.4 Facility exposure and the use at default drawing

FIGURE 8.5 Example of pattern of past to future cash “ins” and “outs” of principal deposits and withdrawing at unidentified maturity saving account

8.3