Article 15.1 Sunshine-backed bond to go on sale

By Tracy Alloway

Financial Times November 4, 2013

The world’s first sunshine-backed bond could be sold in the coming weeks after securing a coveted credit rating that should make it palatable to large investors.

SolarCity said on Monday it would sell a $54.4m bond backed by cashflows from the rooftop solar panels leased to US home owners, who can then claim certain tax breaks from the government. Credit Suisse is bookrunner for the securitisation, which will only be eligible to be sold to big, qualified investors.According to people familiar with the proposed deal, the bonds have secured a credit rating from Standard & Poor’s and pre-marketing of the private placement began on Friday.

Bankers have been experimenting with new assets that can be bundled and sold to investors, as they take advantage of resurgent demand for higher-yielding, sliced- and-diced securitisations. For instance, this week bankers also began selling another type of securitisation backed by foreclosed houses that have been turned into rental homes.

Deutsche Bank, Credit Suisse and JPMorgan are marketing the ‘Reo-to-rental’ after securing a surprise triple-A rating from Moody’s, Morningstar and Kroll for the bonds, which are backed by single-family rental properties owned by Blackstone.

Bankers involved in the solar panel deal had a tougher time convincing rating agencies to evaluate the bonds, according to people familiar with the transaction, after struggling to put together a deal for many months.

As talks with rating agencies about the potential deal deepened this year they hit repeated structural snags. Rating agencies usually rely on historical data to judge the risks of bonds defaulting. In the case of solar panel installations, such data is lacking, making it difficult for the agencies to assess the probability of solar panel lessors missing out on their payments.

Some bankers said that despite the risks of investing in a new asset class, the solar bonds could attract interest from investors keen to place money into environmentally friendly assets that can also generate decent returns.

‘There is a pool of capital that wants to invest in these types of assets,’ said one banker at a large US investment bank. ‘People love to talk about clean technology and renewables, because at some level most institutional investors want to invest in things they can put in their annual report with glossy pictures.’

Solar panel companies will also be hoping that a successful sale of the bonds will provide them with an additional source of capital to finance solar panel installations. To date they have mostly relied on financing from big investment banks to help fund their growth.

With additional reporting by Arash Massoudi.

FT

Source: Alloway, T. (2013) Sunshine-backed bond to go on sale, Financial Times,

4 November.

Why securitise?

Securitisation permits banks, etc. to focus on the aspects of the lending process where they have a competitive edge. Some, for example, are better at originating loans than funding them, so they sell the loans they have created, raising cash to originate more loans. Other motives include the need to change the risk profile of the bank's assets (e.g. reduce its exposure to the housing market) or to reduce the need for reserve capital: if the loans are removed from the asset side of the bank's balance sheet it does not need to retain the same quantity of reserves - the released reserve capital can then be used in more productive ways (There is more on capital reserves in Chapter 16.)

A further motive is to adjust the extent of a bank's maturity mismatch. Banking is a business with large amounts of maturity mismatching, that is, they generally borrow short-term money, e.g. deposits from you and me or interbank loans, which might have to be repaid in hours or days, and lend long term, e.g.

for 5 or 25 years. Sometimes a bank reduces the risks inherent in such a mismatch by placing a group of its long-term loans, say mortgages, in an SPV and then receiving cash from the sale of securitised bonds.The process of securitisation

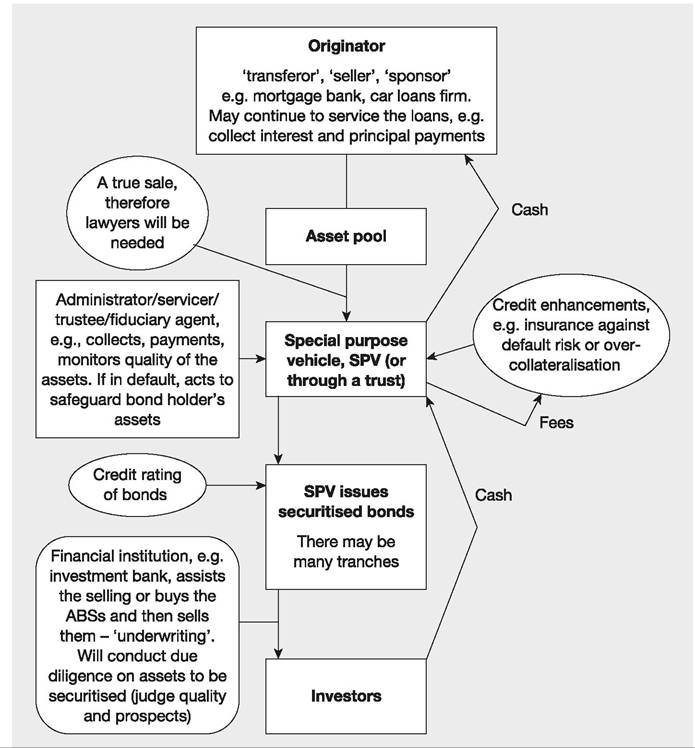

In the most common type of securitisation the originator, the bank or other firm that supplies the assets to be securitised, places them in an issuer, usually an SPV, a company set up for the securitisation - see Figure 15.1. Thus the assets are not vulnerable to the insolvency of the originator, they are bankruptcy-remote.

Credit enhancement is usually sought, which is often a guarantee from a highly rated organisation, e.g. an insurance company, that timely payments on bonds will be made. The credit enhancement when combined with the positive effect of the ring-fencing of assets from the originator frequently allows the securitised bonds to be issued with a triple-A rating. This rating is usually a higher rating than for the originator itself.

The SPV must be a separate entity to be bankruptcy-remote from the originator, even in those cases where the originator has some degree of ownership of the SPV. To make sure, the regulators insist on features such as:

1 The SPV is in existence for securitisation only.

2 It has a board of directors separate from the originator, with independent directors having special powers over when the SPV may place itself in liquidation.

3 The SPV maintains separate assets, bank accounts and record keeping.

4 The SPV pays its own expenses.

5 The originator publicly acknowledges that the SPV's assets are separate and not available to its creditors.

6 There are no inter-company guarantees between originator and the SPV.

7 All business between originator and SPV is conducted on an arm's length basis.

Figure 15.1 The securitisation process

There are different ways of paying bond investors:

• Amortising (pass-through) structure.

As the interest and principal on the underlying assets are received the SPV passes these on in regular payments to the bond holders. Thus, as say mortgagees pay off their mortgages, i.e. the principal is repaid, the size of the asset pool gets smaller - there are fewer outstanding mortgages left in the SPV. This structure is commonly used for home, car and student loan assets. There may be a pre-payment risk with these because the bond holders do not know the proportion of borrowers who will repay their loans earlier than expected. By repaying earlier than expected the overall length of time to maturity of the pool of assets is curtailed.• Revolving structures. The asset pool is topped up with new assets as principal is paid on older ones. In other words, when borrowers pay off their debt principal, the SPV then has cash which can be used to buy, say, more car loans, credit card debt, etc., but only if they fulfil key criteria in terms of quality of the financial asset. Interest payments made by the borrowers is regularly passed on to the SPV bond holders. The replacement of maturing loans carries on in the revolving period, but when the time comes for the amortisation period principal payments are paid to bond holders either periodically or in a single lump sum (bullet or slug methods).

• Master trust. Many batches of securitised bonds can be issued from the same SPV. A large number of mortgages, say, are sold to the SPV, which act as the collateral for a number of securitisations. ABS sold with this collateral backing in a single trust have a variety of different maturities and redemptions. The originator can replenish the asset pool by transferring new mortgages of a comparable credit quality that meet certain pre-defined minimum standards to the trust. Then additional series of ABS, identified by specific dates, can be issued. Thus a recurring process is created with numerous rounds of ABS (often called certificates) issues all backed by a single pool of assets. This is particularly useful where the assets are receivables with a short life, such as credit card receivables that may be paid off in a matter of days or months by the credit card borrowers. New cardholder receivables can take over from the old ones in providing cash flow and security for the ABS. Some of the ABS issued under the master trust may be of lower credit quality (offering high yields) than others.

In the UK, most mortgage-based securitised bonds, RMBS (residential mortgage-backed securities), are from master trusts - see Article 15.2 - with periodic issuing of new bonds and top-ups with new mortgages. In other countries a specific bundle of ring-fenced mortgages is created, against which bonds can be issued.