Article 15.10 Sales of ultra-safe US covered bonds stall

By Tracy Alloway and Vivianne Rodrigues

Financial Times October 14, 2013

Legend has it that Frederick the Great, the 18th century King of Prussia, sent a sword to George Washington inscribed with the words: ‘From the oldest general in the world to the greatest.'

More than two centuries later, efforts to export to the US one of Frederick's oldest and greatest inventions - covered bonds - have completely stalled.

It is a far cry from the situation in July 2008, when then-US Treasury Secretary Henry Paulson recommended the specially-structured mortgage bonds as a way of offsetting the sputtering of Wall Street's loan securitisation machine.

Six years after the US government first raised the possibility of writing new rules that would help US banks sell the special debt, that legal framework is no closer. When bankers and investors gather in New York this week for a conference about covered bonds in ‘the Americas' there is likely to be little excitement about the prospect of Washington - still in gridlock - creating new legislation for the debt.

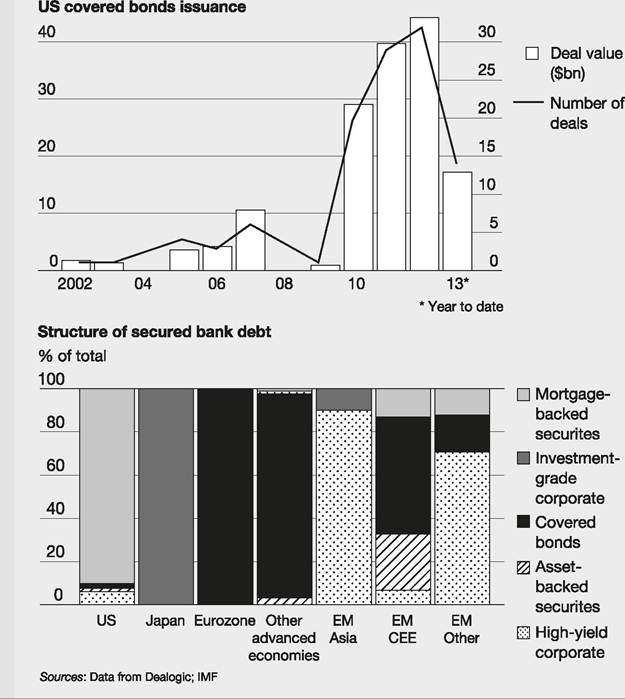

Covered bonds have been a feature of the wider European debt market since Frederick crafted them in 1769 as a way of easing a credit shortage following the devastating Seven Years' War. Early iterations of the bonds allowed creditors to acquire direct claims over Prussian estates, as well as a claim on the debtor.

Giving investors the right to a specific pool of assets differentiated the bonds from so-called ‘unsecured' debt which is not backed by any specific collateral.

This extra recourse remains one of the defining features of modern covered bonds. Even more important is the specially-designed law that accompanies covered bonds in many countries, and which gives investors in the debt added legal protections in the event that the issuing bank goes bust.

While those added protections have made the bonds popular with ultra-conservative investors, they have also impeded the debt's march into the US market.

The Federal Deposit Insurance Corporation (FDIC) is still said to be concerned about the bonds' potential to hoover up assets from a failed or failing bank - making the government agency a key sticking point to new legislation.The lack of a covered bond framework has not stopped the mortgage bonds from being sold in the US. For years, non-US banks, especially Canadian lenders, have been distributing ‘yankee' covered bonds denominated in dollars.

But sales in the US of such bonds have slumped to $17bn so far this year. That is down from $45bn in 2012 and $40bn in 2011, according to data from Dealogic.

The slower-than-expected march of covered bonds into the US is a disappointment for the debt's proponents, who still view the bonds as an elegant solution to the problem of encouraging private investors into a mortgage market which is still largely propped up by government-sponsored enterprises (GSEs).

Some in the market are now looking at alternative ways to make covered bonds work in the US and give banks an opportunity to tap an alternative source of financing, even without new legislation.

FT