Article 15.9 ‘Periphery' bank bonds are the comeback assets

By Christopher Thompson, Rachel Sanderson and Miles Johnson

Financial Times October 17, 2013

Banco Popolare was one of three mid-tier Italian banks which together sold ˆ2.75bn of covered bonds last week.

Weakened mid-tier banks in the eurozone ‘periphery’ economies are widely seen as holding back the continent’s broader economic and financial market recovery.

Yet in spite of limited capital, depressed profitability and bulky books of nonperforming loans, some are returning to favour among investors.

Analysts say Italy’s midsized banks are ratcheting up their bond issuances having seen an opening in the market amid indications that Italy’s crippling two-year recession is coming to an end.

Last week UBI Banca, Banca Popolare dell’Emilia Romagna and Mediobanca - three mid-tier Italian banks - issued covered bonds, collectively raising ˆ2.75bn. It was the largest weekly issue ever from Italian non-national champion banks.

With one eye on the European Banking Authority’s stress tests next year, other peripheral banks are expected to follow suit.

‘It’s about boosting market credibility,’ said Ralf Grossmann, head of covered bonds at Societe Generale. ‘There is the best potential [for debt issuance] in the periphery because they have been absent from the market for some time and they want to show investors that “we can do this”.’

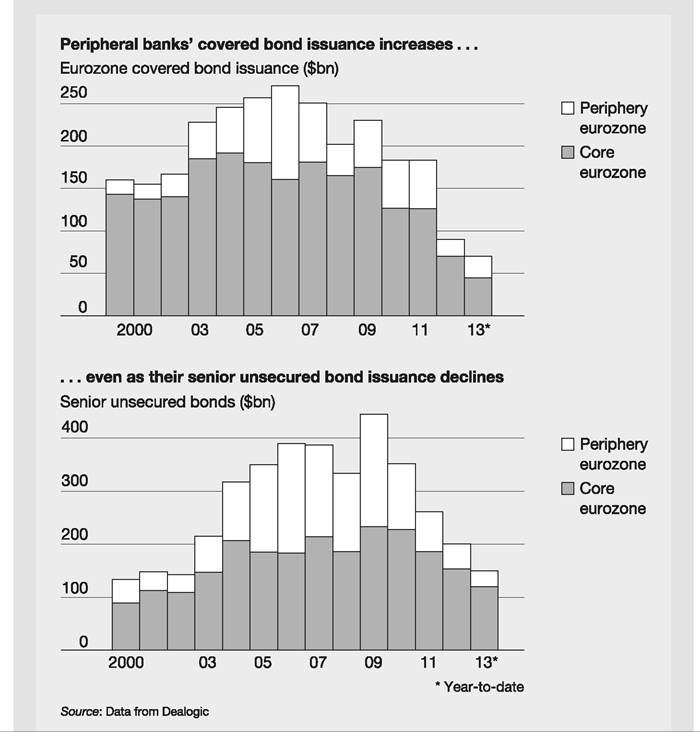

Much of the capital raising has been done using covered bonds - those backed by specific, high-quality assets held by the issuing bank - which are seen as a low-risk form of lending.

Banks in peripheral countries account for more than a third - or $31.7bn - of eurozone banks’ covered bond issuance so far this year, the highest proportion since 2006, according to Dealogic, the data provider.

By contrast, senior unsecured debt issuance, viewed as a bank’s bread and butter funding, has fallen in the periphery year-on-year since 2009.

Since the intervention of Mario Draghi, president of the European Central Bank, Spanish banks have been able to once again issue debt - a process started by BBVA, the country’s second-largest lender by assets, which issued a five-year covered bond back in November last year.

Little wonder they are eager to flaunt their capital raising prowess.

It’s not all plain sailing. Banco Popular [the Spanish bank] struggled to attract significant demand for a ˆ750m bond it issued at the start of September, a sale not helped by uncertainty over US monetary policy at the time.

Moreover, non-performing loans as a proportion of total bank lending continue to rise in Portugal, Ireland, Italy, Greece and Spain, according to research by Royal Bank of Scotland. Mid-tier banks bear the most exposure to bad loans and also to wider sovereign interest rate spreads.

Nevertheless, Oliver Burrows, a credit research analyst at Rabobank, believes the recent deals show the market is increasingly willing to take a punt on the periphery. ‘The fact they’re issuing shows there is a thawing in the market,' he said. ‘It’s not just covered bonds now; we’ve seen a flood of issuance across the capital and credit quality spectrum.’

FT

In the US, covered bonds make up a very small part of the bond universe because the market has been hampered by a lack of legal framework for them - see Article 15.10.