Article 15.8 Moody's risk alert sparks covered bond dispute

By Tracy Alloway

Financial Times July 20, 2011

An unlikely dispute has blown up over one of the finance world's oldest and safest assets, drawing in Danish banks, rating agencies and even a George Soros venture.

Rarely do Danish covered bonds, which have their roots in the reconstruction following the 1795 fire that devastated Copenhagen, generate controversy.But Moody's unsettled the 200-year-old market last month by warning that the bonds were carrying a higher refinancing risk.

The rating agency demanded that Danish issuers top up the debt with billions of extra funds to maintain the top ratings.

‘Denmark is one of the biggest, most liquid, most transparent bond markets around and Moody's are picking on them,' says Alan Boyce, chief executive of the Absalon Project.

At the heart of the rating agency's stance is its assertion that Danish covered bonds

- which pool together mortgages - are changing.

Where once the bonds were almost entirely composed of fixed-rate loans, now more than half of outstanding Danish covered bonds - some DKr1,217bn ($231bn) worth

- are for financing adjustable-rate mortgage (Arm) loans, says Denmark's central bank.

But Danish banks have to reissue the bonds before the underlying loans expire, creating a refinancing risk, according to Moody's.

The interest rate that borrowers pay on their loan also changes every time the bond is refinanced, meaning they may have to pay a higher rate if the rollover comes at a time of financial stress for the issuing bank.

‘Typically, Arm loans mature after 20 to 30 years while the covered bonds mature every one to three years,' Moody's says. ‘Hence there is refinancing risk and the issuers' dependence on regular market access to issue covered bonds has increased with the growing volume of Arm loans.'

Covered bond issuers counter by arguing that unique features of the Danish mortgage market mitigate risk.

Mortgages are capped at 80% loan-to-value and the bonds stay on bank balance sheets, aligning the interests of borrowers and the issuing banks, says renowned financier Mr Soros.Issuers say the debt has never defaulted - not even during Denmark's early 19th century bankruptcy - and also survived the 2008 financial crisis relatively well.

Denmark now has over DKr2,300bn in outstanding mortgage bonds, more than four times the country's government bond market.

But Moody's says the refinancing risk for Danish covered bonds may still be up due to the so-called ‘bail-in' rules introduced for failed banks last year by Denmark's government.

The new rules allow banks to fail and impose losses on creditors and have raised Danish banks' funding costs in recent months.

Danske Bank, which issues covered bonds through its Realkredit Danmark business, says it dropped Moody's after the agency estimated it would have to surrender an additional DKr32.5bn of collateral to maintain the triple A rating on its debt.

Smaller issuers say they will turn to other rating agencies such as Standard & Poor's or Fitch, according to Jan Knosgaard, deputy director-general of the Association of Danish Mortgage Banks. ‘The issuers can't understand Moody's decision; they find it very mechanical and very different to the position of other rating agencies,' he adds.

Danish banks have started spreading their refinancing dates throughout the year to limit the risk of big pressure points.

Nykredit Realkredit, Denmark's largest mortgage lender, says it will hive off its funding for adjustable rate mortgages into a separate unit to protect the ratings on its fixed-rate covered bonds. ‘The mortgage bonds have already traded back up since the Moody's announcement, and this is in an environment where everything else in Europe has widened out,' says Mr Boyce.

‘If Moody's want to play hardball, they should look at some other European covered bonds, things like German Public Pfandbriefe, which are stuffed with exposure to eurozone peripherals but still retain their triple A ratings.'

FT

Source: Alloway, T. (2011) Moody's risk alert sparks covered bond dispute, Financial Times, 20 July.

2011

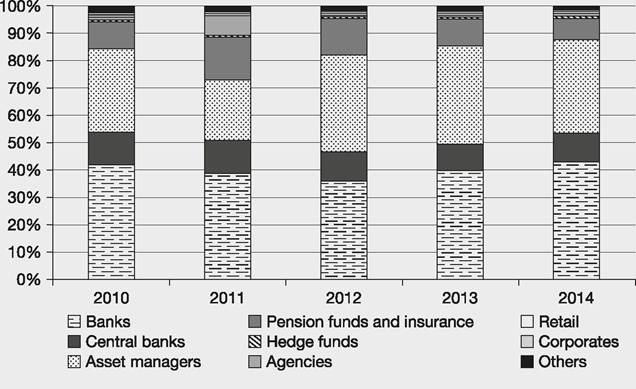

The main investors in covered bonds are banks and investment funds, but there are many others - see Figure 15.7.

Figure 15.7 Allocation of euro-denominated covered bond benchmark issuance by investor type

Source : European Covered Bond Council http://ecbc.hypo.org European Covered Bond Fact Book 2014, European Covered Bond Council http://ecbc.hypo.org/Content/default.asp?PageID=501

Covered bonds originated in 18th-century Prussia, and Europe remains the strongest market for these bonds, where they are well understood by both investors and issuers, see Article 15.9.