Article 15.7 Rebound in sales of risky assets raises fears over quantitative easing's legacy

By Tracy Alloway

Financial Times October 27, 2014

‘Bankruptcy? Repossession? Charge-offs? Buy the car YOU deserve,' says the banner at the top of the Washington Auto Credit website.

A stock photo of a woman with a beaming smile is overlaid with the promise of ‘100% guaranteed credit approval'.On Wall Street they are smiling too, salivating over the prospect of borrowers taking Washington Auto Credit up on its enticing offer of auto financing. Every car loan advanced to a high-risk, subprime borrower can be bundled into bonds that are then sold on to yield-hungry investors.

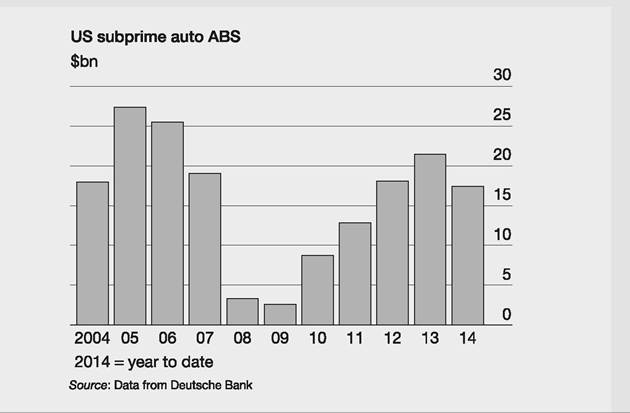

These subprime auto ‘asset-backed securities' have, like a host of other risky assets, been beneficiaries of six years of quantitative easing.

When the Fed began asset purchases in late 2008 the premise was simple: unleash a tidal wave of liquidity to force nervous investors to move out of safe investments and into riskier assets.

It is hard to argue that the tactic did not work; half a decade of low interest rates and QE appears to have sparked an intense scrum for riskier securities as investors struggle to make their return targets. Wall Street's securitisation machine has kicked back into gear to churn out bonds that package together corporate loans, commercial mortgages and, of course, subprime auto loans.

The question now is whether the rebound in sales of risky assets will prove to be a toxic legacy of QE in a similar way that the popularity of subprime mortgage-backed securities was partly spurred by years of low interest rates before the financial crisis.

‘QE has flooded the system with cash and you're really competing with an entity with an unlimited balance sheet,' says Manish Kapoor of West Wheelock Capital. ‘This has enhanced the search for yield and caused risk appetites to increase.'

The subprime auto loan market is a case in point.

Lured by the higher returns on offer from investing in subprime auto ABS, investors have flocked to buy the securities.Washington Auto Credit, just one of many similar companies in a burgeoning industry, helps would-be car owners find financing for their vehicle purchases by connecting them with a growing crop of subprime car lenders. On its website, it lists Flagship Credit Acceptance, a relatively new auto lender backed by the private equity firm Perella Weinberg, as one of its partners.

Like other subprime auto lenders, Flagship has been able to grow its business by tapping strong investor demand for subprime auto ABS. So strong is that demand that Flagship has been marketing ABS with a ‘prefunding’ feature - in effect selling securitised bundles of auto loans before the loans have even been made.

Such prefunding features were a hallmark of securitisation markets before the crisis, when demand for residential mortgage-backed securities was so high that it outstripped supply of new loans. Now a similar dynamic appears in play, prompting concerns that investors’ relentless search for yield will once again end poorly.

There remains a lingering unease that investors are being herded into asset classes that may not be adequately compensating them for the risks involved. Some are already leveraging their portfolio and using derivatives to help amplify their returns during a period of unprecedented low interest rates.

FT

Source: Alloway, T. (2014) Rebound in sales of risky assets raises fears over quantitative easing's legacy, Financial Times, 27 October.

Covered bonds

Covered bonds are similar to the securitised asset-based bonds described above, in that a specific group of assets, e.g. mortgage receivables, is used to back up the claims of the bond holders. But covered bonds give investors extra layers of protection compared with other types of ABS.

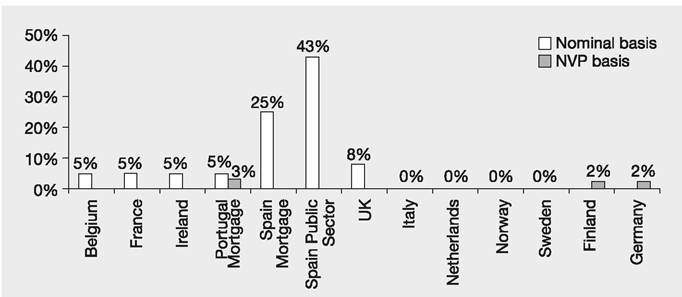

First, only banks are permitted to issue them and investors have full recourse to the bank's resources. This applies even for those issued through a special purpose vehicle which on-lends the proceeds to the originating bank (either through a loan or by buying its bonds). Thus if the covered bonds do not pay on time investors can obtain payment from the bank that issued them, albeit indirectly, through the SPV.Furthermore, if the issuer goes bust, covered bond holders have priority claims on the assets (mortgages, etc.) held in the cover asset pool. This is always a segregated collection of financial assets, separate from the assets of the bank. Covered bond holders rank above unsecured creditors of the bank in being able to claim the assets in the pool. Thus covered bond holders are protected from the failure of the bank because they have a group of ring-fenced assets they can turn to, while, at the same time, if the bank is fine but the pool of assets turns out to be a dud, investors can turn to the assets of the bank held outside of the cover asset pool. In most jurisdictions the value of the assets in the cover pool is required at all times to exceed the value of the covered bonds by a prescribed amount: over-collateralisation - see Figure 15.3.

There is also the protection offered of dynamic cover pool maintenance, meaning that the bank has an ongoing obligation to maintain sufficient high-quality assets in the cover pool as collateral to satisfy the claims of

Figure 15.3 Legal minimum over-collateralisation levels for covered bonds in Europe

Source : European Covered Bond Council http://ecbc.hypo.org European Covered Bond Fact Book 2014,

European Covered Bond Council http://ecbc.hypo.org/Content/default.asp?PageID=501

covered bond holders at all times. Under this the bank is required to add further assets to the cover pool to compensate for matured or defaulted assets (e.g.

house owner not paying his mortgage). This contrasts with most securitisations, where the sponsoring institution is not obliged to replace defaulted assets, so the losses are borne by the bond investors.On top of that protection, covered bonds can be issued only in strict legal and supervisory settings. Supervision typically includes:

• a special cover pool monitor

• periodic audits of the cover pool by the cover pool monitor

• arrangements for ongoing management and maintenance of the cover pool should the bank become insolvent to ensure continued payments to covered bond holders.

In most of the 29 countries with covered bond markets the monitor is a public authority, e.g. the banking supervisory authority. In other countries the issuing organisation (e.g. bank, SPV) appoints an external auditor (outside its control) to regularly audit the cover pool, as well as an external trustee to safeguard bond holders' interests.

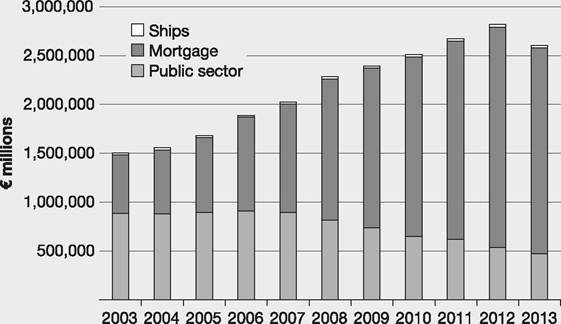

The financial assets held within the cover pool include loans and bonds. There might also be derivatives designed to hedge interest rate and currency risk, but equities, property and commodities cannot be included. The most common pool asset is mortgage loans secured on residential or commercial property, but in many countries there is a large market in covered bonds where the underlying assets are loans to public entities such as regional or local authorities. Ship loans comes in a distant third.

Figure 15.4 shows the growth of this market, which in 2013 had more than ˆ2.5 trillion outstanding, with an increasing shift towards mortgage-backed covered bonds and a decrease in the importance of public sector CBs.

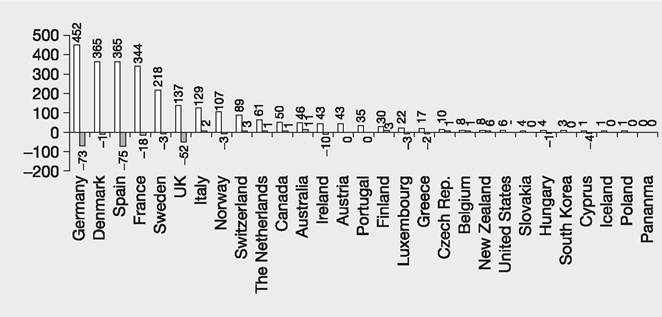

We can see clearly from Figure 15.5 that the covered bond market is more significant in some European countries than others. Germany takes nearly 20% of the outstanding covered bond market (its covered bonds are called Pfandbriefe). Spain, Denmark and France all have around ˆ350 billion outstanding. The UK accounts for 5% (nearly ˆ137 billion), while the US, with less than 0.3% of the market, is only just getting going.

Figure 15.4 Total outstanding covered bonds outstanding bonds, 2003-2013

Source: Data from European Covered Bond Council http://ecbc.hypo.org European Covered Bond Fact Book 2014, European Covered Bond Council http://ecbc.hypo.org/Content/default.asp?PageID=501

Figure 15.5 Outstanding covered bonds by country as well as change versus 2012 in billions of euros

Source : European Covered Bond Council http://ecbc.hypo.org European Covered Bond Fact Book 2014, European Covered Bond Council http://ecbc.hypo.org/Content/default.asp?PageID501

About three-quarters of covered bonds are denominated in euros, with US dollar and UK pound issues accounting for only a small fraction of the total. More than 97% in a typical year are issued with fixed-rate coupons, rather than floating rates.

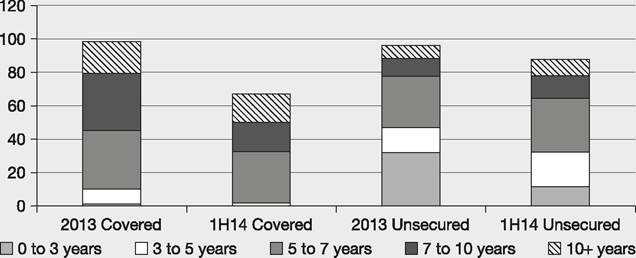

Figure 15.6 Covered bond and senior unsecured euro new issues by maturity, billions of euros

Source : European Covered Bond Council http://ecbc.hypo.org European Covered Bond Fact Book 2014, European Covered Bond Council http://ecbc.hypo.org/Content/default.asp?PageID=501

Some are short bonds, but most are medium-term bonds - see Figure 15.6.

Because of their high level of backing, covered bonds are usually given high credit ratings (AAA) and are therefore a relatively low-cost way for financial institutions to raise money. Having said that, the AAA rating is far from automatic - see Article 15.8.

More on the topic Article 15.7 Rebound in sales of risky assets raises fears over quantitative easing's legacy:

- Article 15.7 Rebound in sales of risky assets raises fears over quantitative easing's legacy

- Michel Foucault's provocative critique of the modern prison system, first published in 1975, raises important questions about the evolution of justice in the West.