Article 15.6 Asset-backed securities: back from disgrace

By Christopher Thompson and Claire Jones

Financial Times September 30, 2014

When Ian Bell visited the European Commission in the dark days after the global financial crisis to lobby for ‘high-quality’ asset-backed securities, the veteran financial analyst was given short shrift.

The packages of loans that were sliced and diced and sold off to investors had become one of the symbols of the type of financial engineering that brought on the worst economic crisis since the Great Depression.‘They would listen politely and say, “thanks for coming - don’t call us, we’ll call you”,’ says Mr Bell, the head of the Prime Collateralised Securities secretariat, a body set up in London to monitor the quality of ABS after the crisis.

By late 2013, however, the policy makers were inviting him back to Brussels. ‘When I arrived they were sitting in a room with pads and pens saying, “high-quality securitisation - how can we make it work?” ’ The reason for the volte-face is simple enough: two years on from the promise by Mario Draghi, president of the European Central Bank, to do ‘whatever it takes’ to save the euro.

Mr Draghi gave the eurozone a much-needed respite, pushing euro borrowing costs for banks and governments to record lows. But as concerns have grown in recent months about deflation, Mr Draghi has realised that more radical intervention is needed. He says a reinvigorated ABS market will allow banks to start lending again to struggling small- and medium-sized businesses.

The ECB is expected to announce details on Thursday in Naples of an ambitious plan to buy hundreds of billions of euros of repackaged debt in order to kick-start bank lending.

‘Assets only recently branded as toxic are being heralded as potential saviours,’ says Andrew Jackson at Cairn Capital.

Supporters say a revival in the eurozone’s moribund ABS market would allow banks to trim their bloated balance sheets and free up capital for lending.

This would allow smaller companies to borrow money to invest in their businesses. But it would also entail unprecedented levels of credit exposure for the ECB. Mortgage-backed securities account for about two-thirds of the ABS market.‘The ECB is taking a bet on the credit market, and by opening to mortgage-backed purchases, especially the housing market, which has potentially powerful fiscal implications for the eurozone area,' says Carlo Altomonte, a professor at Bocconi University.

The plan has powerful critics. Last week, Wolfgang Schauble, Germany's finance minister, voiced his unease. ‘I am not particularly happy about the debate started by the ECB about the purchase of securitisation products.'

The ECB and Bank of England consider a revival of the market as a way of transforming European finance from a system based on bank loans to a US-style system weighted more in favour of capital markets.

Europe's bank dependence is stark: banks account for nearly 80% of corporate loans compared with about 50% in the US. With a greater variety of non-bank sources of finance, businesses' access to credit is not solely tied to the fortunes of their high street bank. Proponents of the plan point to the US programme of asset purchases as evidence that it can work in Europe.

The US Federal Reserve has $1.7tn in mortgage-backed securities on its balance sheet as a result of its buying programme since 2009, leading to a sharp rebound in US ABS volumes. The ability to sell historic debts has given banks more lending capacity. Commercial and industrial loans, for example, have risen by 45% to $1.74tn since late 2010.

‘The key takeaway [from the US] is “build it and they will come”,' says Jim Caron at Morgan Stanley. ‘There were many questions about who would invest and would it work. But once the government started to buy [MBS] it kick-started other forms of lending and moved collateral away from banks to non-banks.'

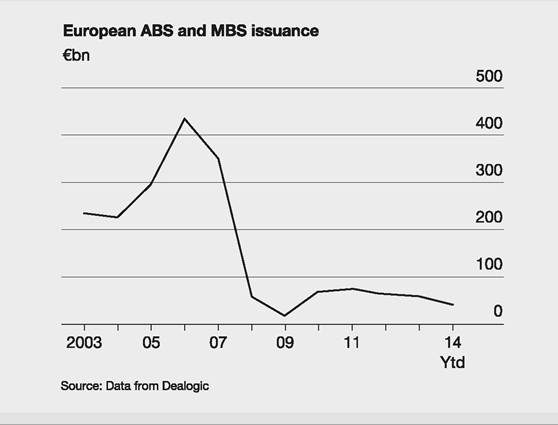

There is also evidence that Europe's inventory of ABS is in better condition than that of the US, where default rates were much worse.

Of more than 9,000 European ABS notes issued during the past decade, only 2% have defaulted or are likely to realise future losses, according to Moody's Investors Service, compared with about a fifth of US ABS.Mr Draghi said the ECB would only buy products that were ‘simple, transparent and real'.

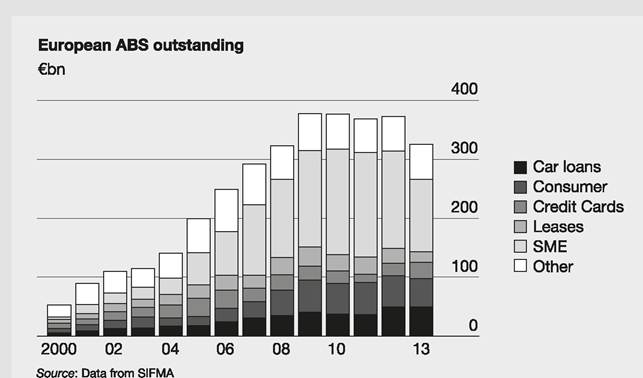

The ECB could start with ABS backed by SME, consumer and car loans, of which there is ˆ300bn outstanding. Most existing ABS are held by banks as collateral in exchange for ECB loans. If the ECB included all banks' outstanding loans and mortgages that could be feasibly packaged, the potential ABS could be ˆ3tn.

FT

Source: Thompson, C. and Jones, C. (2014) Asset-backed securities: back from disgrace, Financial Times, 30 September.

Even sub-prime is making a come-back in the US, with bonds securitised on sub-prime car loans selling particularly well - see Article 15.7. Quantitative easing is discussed in Chapter 16.