Article 15.5 Sliced and diced debt deals make roaring comeback

By Tracy Alloway

Financial Times June 4, 2014

In early June 2009, the world's securitisation bankers congregated at a London hotel on Edgware Road, not far from the prison cells at Paddington Green police station.

It was a location symbolic of the state of the securitisation industry in the aftermath of the financial crisis, when the bankers who had sliced and diced loans into bonds were in the collective doghouse. ‘Regroup and rebuild' was the humble slogan for that year's ‘Global ABS', or asset-backed securities, conference.

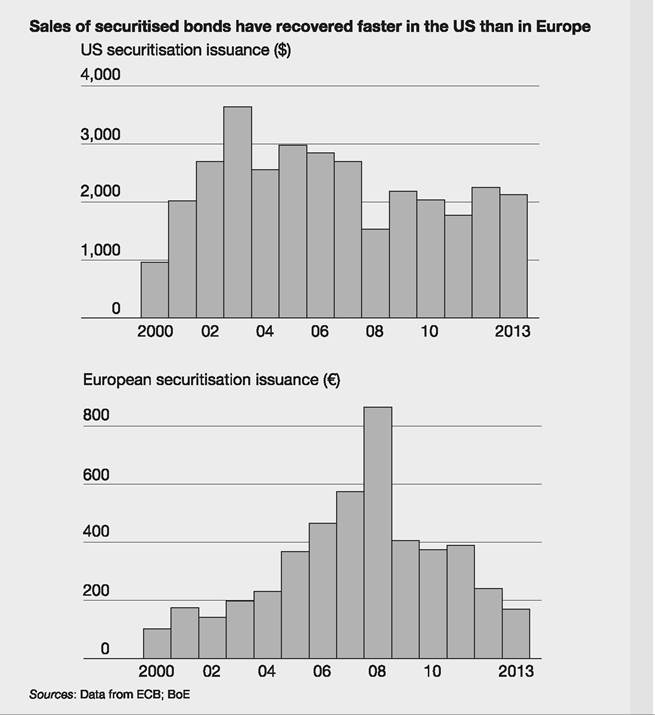

Five years later and bankers are heading to the sunnier climes of Barcelona for the annual ABS gathering. The location is, once again, suggestive of the wider state of securitisation markets - one that features a much brighter outlook.

Certain securitisation deals have roared back in the US. The European market could soon come back to life after a prolonged hibernation.

In the US, the resurgence has been swift. While the kind of subprime mortgage- backed securities that played a prominent role in the build-up to the financial crisis remain dormant, other securitisation deals have rebounded thanks to investors' hunger for yield and low corporate default rates.

Issuance of commercial mortgage-backed securities totalled $102bn in 2013, according to Dealogic data, the highest since the $231bn sold just before the crisis.

In the US investors, such as insurers and pension funds, have long been buyers of ABS. By contrast, much of the pre-crisis demand in Europe for such securities came from local banks and related structured investment vehicles which disappeared in the crisis.

‘[In the US] there was continuous demand for fixed-rate product, whereas in the European market demand was much more dependent on the sale of floating-rate paper,' says Doug Tiesi, chief executive of Silverpeak.

Nevertheless, there are critics who warn that the industry has yet to learn the lessons of the crisis. Adam Ashcraft, head of credit risk management at the Federal Reserve Bank of New York, warned at a conference last year: ‘We haven't done anything meaningful to prevent the securitisation market from doing what it just did.'

Bankers are conscious the industry still needs to rebuild its reputation following the excesses of the past.

FT

It is hoped that the European securitisation market can grow strongly, not least because the European Central Bank and the Bank of England are helping to promote a ‘high-quality' packaged debt market - see Article 15.6.