Article 15.4 Banks shun packaged UK mortgage deals

By Christopher Thompson

Financial Times October 9, 2014

A former landfill site 10 minutes' drive from Nottingham's town centre is an unlikely symbol for the fortunes of the UK's struggling mortgage-backed securities market.

In the centre of the Showcase Cinema leisure park, amid knee-high weeds and broken bottles, stands a barn-sized building which used to house the city's biggest nightclub, called Isis. In 2009, amid a deepening recession, police ordered its closure after an R&B music night when a clubber was stabbed. It was not long before the club's owner, James Eftekhari, fell behind on his mortgage repayments.The Isis mortgage was one of 27 ‘sliced and diced' commercial property mortgages that had been rolled up into London & Regional Debt Securitization No 2, a £256m MBS that subsequently defaulted. Five years later, in an echo of the wider sluggishness in the UK MBS market, the nightclub still stands vacant.

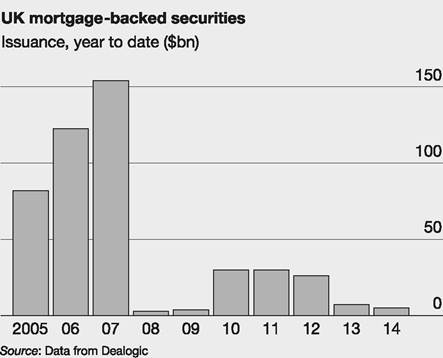

Volumes of UK MBS, whereby banks package together commercial and residential mortgages for sale to fixed-income investors, have traditionally been among the biggest in Europe. But volumes of $5.1bn for the year to date are poised to plumb the lowest annual total since the crisis in 2009.

‘Issuance has gone off a cliff since 2011,' says Ganesh Rajendra at Royal Bank of Scotland.

The primary reason for the fall is simple: banks do not need the funding. After volumes rose in the wake of the crisis - 2010 saw a nearly tenfold increase in ABS issuance year-on-year to $30bn - they declined sharply in 2012 after the Bank of England's ‘funding for lending' scheme (FLS), which offered banks cheaper funding than selling ABS on the open market.

‘Banks' need for securitisation funding has been diminished,' says Neal Shah at Moody's.

‘Banks have been deleveraging their balance sheets over the past few years, and at the same time have had access to various forms of relatively cheap liquidity, including FLS.'Even as volumes shrank investor demand remained robust. The result is that spreads - the amount of interest paid over the London Interbank Offered Rate - have declined markedly.

‘Expectations of new issuance collapsed,' says Dipesh Mehta, a research analyst at Barclays. ‘Before FLS a senior tranche of a residential mortgage-backed security priced at 150 basis points over Libor - now the same senior RMBS tranche is trading at between 30-50 basis points over Libor.'

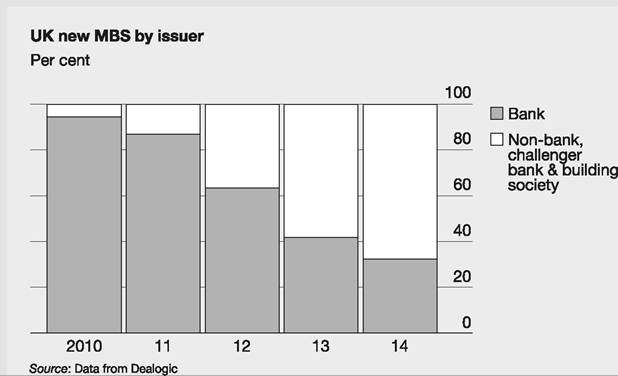

As the big high street banks cut back volumes, challenger banks such as Virgin Money and Aldermore picked up some of the slack, albeit with smaller issues. In 2010 smaller banks and building societies accounted for 5% of MBS issuance. This year they account for two-thirds, according to research by RBS.

FT

You can see in Article 15.5 that the US market has remained extremely strong, with a blip in 2008. Investor confidence grew as it became clear in 2009-2010 that most pre-crisis securitised bonds, e.g. prime mortgage, car loan, credit card securitisations and student loans, were performing as they were supposed to through a recession. This led to high demand from insurance companies, banks, hedge funds and pension funds.