Article 15.3 Securitisation: it's all a question of packaging

By Richard Beales

Financial Times July 25, 2007

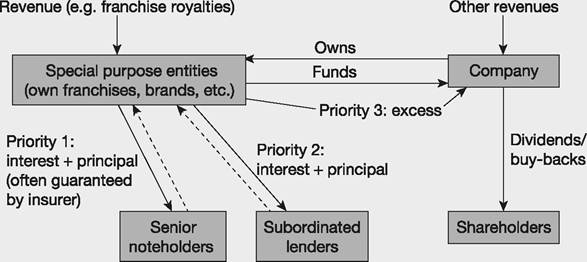

In a corporate securitisation, assets and related cash flows are carved out from a business into special purpose entities (SPEs) and repackaged.

Debt is then raised against the SPEs alone.‘Securitisation isolates a cash flow and insulates it from extraneous events,' says Ted Yarbrough, head of global securitised products at Citigroup.

Depending on the credit quality and the quantum of borrowing, part or all the debt may be highly rated, and there is sometimes a low-rated or unrated subordinated slice of debt as well.

A financing structured this way can achieve higher credit ratings than the business on its own. This partly reflects the structural aspects - for example, the fact that the SPEs can survive a bankruptcy of the umbrella group - and partly the fact that the securities issued are often ‘wrapped’, or guaranteed, by highly-rated bond insurers such as Ambac, FGIC or MBIA in return for a fee.

This is a complex and costly exercise, but can result in much cheaper debt. Once established, a securitisation can be tapped again later if a business grows.

Sometimes securitisation is best suited to part of a business rather than the whole. When applied to an entire business, as with Dunkin’ Brands or Domino’s, the new financing typically replaces all traditional debt.

Rob Krugel, head of the esoteric asset-backed securities business at Lehman Brothers, says: ‘Generally, the constituencies - rating agencies and bond insurers - require that all pre-existing debt is refinanced. There is flexibility on a go-forward basis to issue debt outside the securitisation as well as additional securitisation debt. We generally find that securitisation is so efficient there’s no reason to issue debt outside the structure.’

While a securitisation does involve financial constraints, they can be fewer and less onerous than with traditional bank and bond debt.

Managers would, for example, have greater flexibility to pay dividends or buy back stock.This reflects the fact that financiers in a securitisation look only to the specific assets and cash flows held within the SPEs. But Eric Hedman, analyst at Standard & Poor’s in New York, notes there can be a trade-off in terms of operational flexibility. ‘Prior to the securitisation, Dunkin’ was an owner operator. Now, the company is no longer the franchisor, there’s an SPE. Any new store agreement is for the benefit of the securitisation.’ The company’s management also does not have sole discretion over advertising spending, for example.

And the Dunkin’ Donuts brand is no longer owned by the company. ‘The sign on the wall says “Copyright DD IP Holder LLC”. That’s a bankruptcy-remote SPE set up for the benefit of noteholders [in the securitisation],’ Mr Hedman says.

This kind of shift might not suit all managers. But for some executives - particularly those focused on maximising cash returns to shareholders - such considerations can be outweighed by the financial benefits.

Private equity owners also like the fact that securitisations are ‘portable’ - they can stay in place through a change of ownership. ‘That’s a big hook from the point of view of sponsors,’ says John Miller, US head of financial sponsors at Lehman.

But Mr Yarbrough concedes that the structural demands of securitising their entire business may not suit even the majority of companies. ‘I don’t know how many businesses are really going to completely fit that model,’ he says. ‘But what you will see is securitisation increasingly becoming a part of a financing solution.’ With the help of bond insurers, corporate securitisations can achieve triple-A or at least investment grade ratings, even if the company concerned could not have done so. This attracts the broadest possible range of investors, including pension funds and fund managers at the most highly-rated end, and hedge funds lower down the capital structure.

Mr Krugel says the magic is in the legal separation of the assets and the creation of a tailored package for securitised investors. ‘You're not fundamentally changing the operational risk of the business, but you're putting in place a lot of protections in downside cases.'

He says it is also crucial that the SPEs are bankruptcy-remote. He points to the test case of US car rental group Alamo National.

A securitised financing put in place before the group went bankrupt in 2001 survived the bankruptcy process, and was used for acquisition finance when the company was acquired by private equity firm Cerberus in 2003.

FT

Source: Beales, R. (2007) Secularisation: it's all a question of packaging, Financial Times, 25 July.

2007

The giants in the US market

The really big players in the securitisation market are the US quasi-government bodies of Fannie Mae, the Federal National Mortgage Association (FNMA), and Freddie Mac, the Federal Home Loan Mortgage Corporation (FHLMC), both ‘government sponsored enterprises' (GSEs). They were privately (shareholder) owned companies acting in accordance with US government mandates to provide funding for the housing market. Even then there was an implicit subsidy from the government because everyone knew that bond holders would be bailed out by the government if anything went wrong, thus they could borrow cheaply, being regarded as virtually risk free. Sure enough, in 2008 the government had to bail them out with a $187.5 billion injection of US taxpayers' money. The value of the old shares was wiped out and Fannie and Freddie went into conservatorship, meaning they are owned by the government and profits go to the government.

Fannie and Freddie buy collections of mortgages from mortgage providers and issue bonds backed by the security of these mortgages (mortgage bonds or mortgage-backed securities (MBS)), thereby creating a secondary mortgage market.

They guarantee that the interest and principal on the MBS are paid, thus the ultimate lenders have recourse to the GSE.Ginnie Mae, the Government National Mortgage Association (GNMA), also guarantees the timely payment of principal and interest payments on residential MBS backed by federally insured or guaranteed loans sold to institutional investors. These are mainly loans insured by the Federal Housing Administration (FHA) or guaranteed by the Department of Veterans Affairs (VA). Other guarantors or issuers of loans eligible as collateral for Ginnie Mae MBS include the Department of Agriculture's Rural Development (RD). Unlike Freddie Mac and Fannie Mae, Ginnie Mae neither originates nor purchases mortgage loans.

US mortgage bonds guaranteed by government-owned or sponsored enterprises are known as agency MBS. They make up by far the largest section of the US MBS market - they underwrite more than 80% of new US mortgages. Non-agency MBS are issued by banks or financial institutions, and rely on the quality of the collateral for their credit rating.

The sub-prime crisis

In the old days the government-sponsored enterprises Fannie Mae and Freddie Mac would not take just any old mortgage. They usually insisted that the house owner owed no more than 80% of the value of the house (loan-to-value ratio (LTV)) and the maximum size of mortgage was $417,000. They also investigated the borrower's income, state of employment, history of bad debts (if any) and amounts of other assets. In other words, this system was pretty safe because only the most creditworthy entered it. It was for prime mortgages only.

Now for some innovation: in the early 1990s new lenders emerged who were willing to lend to people who did not qualify as prime borrowers. They would often employ independent firms of mortgage brokers to persuade families to take out a mortgage. The brokers received a commission for each one sold. The number of sub-prime lenders grew significantly over the 12 years to 2005 and the proportion of mortgages that were sub-prime rose to over 20%.

The rise of this market attracted the interest of the big names on Wall Street (e.g. Goldman Sachs, Merrill Lynch, Lehman Brothers, Bear Stearns and Morgan Stanley), which bought up sub-prime lenders. These borrowers could be charged higher interest rates than prime borrowers. They could also be charged large fees for setting up the loan. The sub-prime market boomed. By 2005 the largest US mortgage provider was the sub-prime lender Countrywide Financial, which had grown fast from 1980s' obscurity.A key characteristic of the new lenders was that they lent at different interest rates to different groups of mortgagees classified on the basis of statistical models of likelihood of default. These relied heavily on the borrower's credit score. This score was calculated by examining a number of borrower characteristics, the most important of which became the absence (or low incidence) of missed or delayed payments on previous debts. The statisticians had discovered a high correlation between credit scores and defaults on mortgages in the 1990s and so it made sense to them to carry on with them in the 2000s. The problem was that the statisticians had not fully taken on board the extent to which mortgages in the 2000s were different to mortgages in the 1990s, particularly at the sub-prime end of the market.

Many of the 2000s mortgages required much less documentation than in the 1990s. People were often not even required to prove their level of income; they could just state their income. Nor was it necessary to pay for an independent valuation of the house; borrowers could just state the value of the house. Stated income loans were convenient for those without regular work, but anyone with common sense can see the potential temptation to overstating income to speculate on rising prices (they quickly became known as liar loans on the street - a clue that the mathematicians could have picked up on if they had taken time to glance up from the algebra).

Another change was the help given with the deposit on the house.

Whereas traditionally households would have to find 10-20% of the house value as a down payment, in the new era brokers could offer a second mortgage (called a piggyback) which could be used as the deposit, so 100% of the value of the house could be borrowed. Taking things a stage further, the UK's Northern Rock offered mortgages that were 125% of the value of the house.A further change was the increasing use of mortgages that had very low interest rates for the first two years (teaser rates), but after that they carried rates significantly higher than normal - 600 basis points above Libor was merely the average, many paid much more, i.e. well into double figures.

The more rational players in this market allowed for the qualitative changes that had taken place in the housing markets in the noughties, rather than sim- plistically using a mathematical model developed in the 1990s for estimating default likelihood. Those wedded to quantified data in the statistical series had difficulties adjusting to the new reality.

Originate-and-hold to originate-and-distribute

Traditionally, if a bank grants a mortgage it keeps it on its books until it is repaid. This is called the originate-and-hold model. In this way banks have every incentive to ensure that the mortgagee can repay and can help those few who have temporary problems along the way. Fewer and fewer banks kept mortgages on the books in the 2000s. They preferred the originate- and-distribute model, selling them to other investors, usually through securitisations. Alongside this development was the movement of investment banks to use their own money to invest in securities rather than only provide (lower-risk) advice and other fee-based activities.

In the 1990s only around one-quarter of sub-prime mortgages were packaged up into securitisation vehicles and sold to bond investors. By the mid-2000s three-quarters were. In the good old days Freddie and Fannie dominated this market; in the boom of the mid-2000s the private firms overtook the GSEs and issued vast quantities of mortgage-based securities - over $1,000 billion per year, cumulating to $11,000 billion by 2007. The leaders of this pack included the Wall Street investment banks as well as Countrywide and Washington Mutual.

Pressure was applied to the mortgage brokers to generate more mortgages which could then be repackaged so that the investment banks could generate fees and other profits from the transaction. The mortgage brokers were only too happy to oblige, so they ran after people to sign up for mortgages to receive commission. No job, no deposit, on welfare benefits? Don't worry, we have just the mortgage for you!

Despite losing their lead the GSEs still participated. Apart from holding hundreds of billions of dollars worth of MBS they had created, they also bought more than $1,000 billion of MBS issued by the private firms. They felt safe because they had put in place ‘safeguards'. First, if the loans were at more than 80% of LTV they insisted on insurance being purchased from private insurance firms that paid out in the event of default. Second, the credit rating agencies had checked out the default likelihood on the private MBS they bought and had concluded that they should be granted AAA status. What could go wrong? Well, much of the insurance proved to be worthless as insurance companies went bust, overwhelmed by the sub-prime losses, and credit

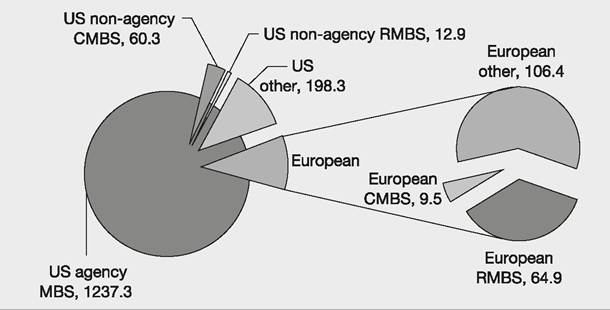

Figure 15.2 Securitisation issuance, 2013, ˆbn

Source : Data from European Securitisation Forum Securitisation Data Report

rating agencies looked foolish in granting high credit scores. Even they got caught up in the rose-tinted vision of the time. (Or did they, as some people suggest, have an incentive to rate excessively high? The debate rumbles on.)

The volume of mortgage payment defaults was too much for Fannie Mae and Freddie Mac and they had to be taken under government supervision in 2008 (they were too big to be allowed to fail) and government guarantees were put in place to try to restore public confidence. Fannie Mae and Freddie Mac, along with Ginnie Mae, still have an enormous slice of the ABS market - see Figure 15.2. Thus, in the land of the free (markets) most mortgage bonds are guaranteed by the government, squeezing out the private securitisation market and producing large profits. The flows of interest and principal payments for commercial mortgage-backed securities (CMBS) shown in Figure 15.2 come from companies paying off mortgages on commercial property (offices, factories, etc.).

European securitisation

The European asset-backed securities market is less than a quarter of the size of the US market. It has always been smaller, but it faltered particularly badly after the 2008 debacle. Also banks are currently not interested in increasing volumes of lending and so do not need to securitise, especially when they can borrow cheap money from the European Central Bank or the Bank of England - see Article 15.4.