Article 16.1 Turkey's central bank cuts rates despite mounting inflation

By Daniel Dombey

Financial Times May 22, 2014

Turkey's central bank has cut its benchmark interest rate by 50 basis points despite mounting inflation, a move likely to rekindle the debate about the bank's independence.

But in a decision that took some economists by surprise, the central bank - which is formally independent - announced on Thursday that it was enacting a ‘measured decrease' in the benchmark one week repo rate from 10% to 9.5%. The broader range of rates at which the central bank lends money to the banking sector remained unchanged.Last January, the central bank defied [president of Turkey] Mr Erdogan's calls for lower borrowing costs and increased the repo rate to 10%, during a midnight meeting. The move sparked rallies in both the lira and Turkish equity markets, after weeks in which the currency had slid against the dollar.

While the currency has recovered, Turkey's inflation has continued to rise, reaching a two year high of 9.4% in April. Economists expect prices will rise even faster this month.

In its statement on Thursday, the bank argued that a ‘recent decline in uncertainties and improvement in the risk premium indicators' had led to a fall across the board in market interest rates. It insisted that ‘the monetary policy stance will continue to be tight' despite the latest cut.

FT

Source: Dombey, D. (2014) Turkey's central bank cuts rates despite mounting inflation, Financial Times, 22 May.

An alternative, used in many countries, is to lend or borrow in the interbank market to add or subtract reserves and influence rates of interest charged. In the US, for example, the Fed funds rate is targeted.

Repos and reverse repos are, by their nature, temporary interventions because the opposite transaction takes place on maturity, a few days after the first buy or sell. There are times when the central bank wants to effect a more permanent change in the money supply.

Then it can go for an outright transaction, a purchase or a sale (of government bills and bonds), that is not destined to be reversed in a few days.(An alternative way to increase the monetary base is for the central bank to lend money to a commercial bank. The central bank simply credits the commercial bank's account with electronically created reserves. The amount of monetary base is less controllable through this method than through open market operations because the banks may or may not borrow, even if the central bank offers enticing interest rates.)

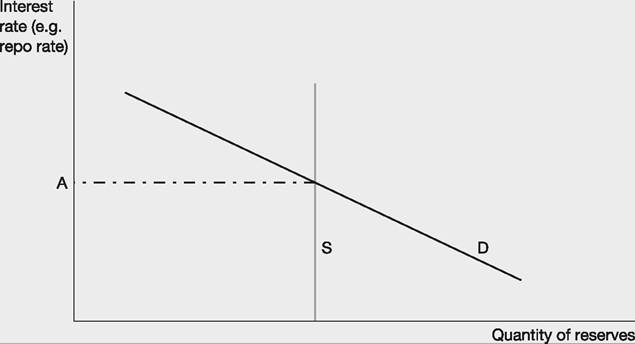

The supply and demand of reserves

Banks trade surplus reserves with each other. They always have an incentive to lend - even if only for 24 hours - if they find themselves with too many reserves. Each day there will be dozens of other banks that find themselves temporarily below the reserve level they need and so they willingly borrow in the market. The main target for central banks is usually the overnight interest rate on loans of reserves from one bank to another. In the US this is the Federal funds rate, in the eurozone it is the overnight repo rate in euros, and in the UK it is the overnight sterling repo rate. Switzerland opts for the Swiss franc Libor target rate. Soon after the official rate changes (typically the same day) banks adjust their standard lending rates (‘base rate' in the UK), usually by the exact amount of the policy changes. This is transmitted through money market rate changes, repos, interbank lending, etc. The impact on longer-term interest rates can go either way when the short-term rates are changed, depending on what the market perceives the future will bring in terms of inflation and additional rises or falls in the overnight interest rate. (A rise in the official rate could, for example, generate expectations of lower future interest rates, in which case long rates might fall in response to a rise in short-term rates.)

If we take the banking system as a whole, the demand for reserves falls as interest rates rise.

That is, the quantity of reserves demanded by banks (holding all else constant) reduces if banks have a higher opportunity cost of keeping money in the form of reserves; they would rather lend it out to clients to achieve higher interest rates. This becomes more and more of a lost opportunity as rates in the short-term interest rate markets rise. Bankers increasingly start to think that they can economise on the excess reserves buffer if interest rates are high. Thus, the demand curve for reserves, D, slopes downwards in Figure 16.2.The central bank usually has a continuous programme of lending into the general repo market and so there is a large quantity of money borrowed by banks from the central bank at any one time. It is through the adjustment to the amount of reserves outstanding that the central bank controls interest rates. The supply curve for reserves, S, is the amount of reserves from the central bank supplied through its open market operations (in more normal times, at least). Equilibrium occurs where the demand for reserves equals the quantity supplied. This occurs at an interest rate of A, providing the short-term interest rate in the market.

Figure 16.2 The demand and supply of reserves

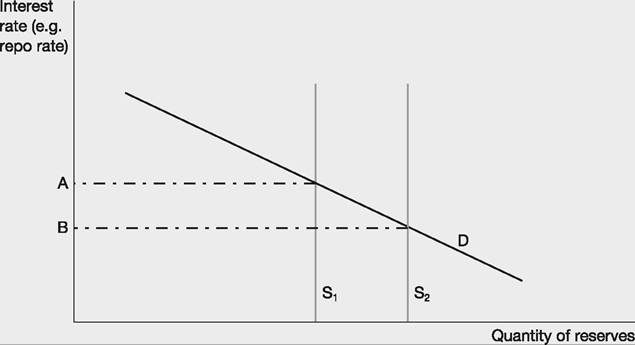

Now imagine that the central bank wishes to lower interest rates. It does this by increasing its purchases of government securities in the repo market, providing a greater quantity of reserves. This pushes the supply curve in Figure 16.3 from S1 to S2, and moves the equilibrium interest rate from A to B. Obviously, if the central bank reduced its reserves outstanding to the banking system by selling additional securities, the supply curve would move to the left and the interest rate would rise.

So far we have discussed dynamic open market operations. That is, where the central bank takes the initiative to change the level of reserves and the monetary base within a reasonably static banking environment.

However, many times the environment is not static because there are a number of factors changing demand for borrowed reserves, e.g. greater or lesser banker confidence in the economy and thus the potential for low-risk lending. Thus, it intervenes - a defensive open market operation - to offset the other factors influencing reserves.

Figure 16.3 An open market increase in the supply of reserves

When the central bank wants to change short-term interest rates it can often do so merely by announcing its new target rate and threatening to undertake open market operations to achieve it rather than actually intervening. The money market participants know that if they do not immediately move to the new rate they will encounter difficulties. For example, if the central bank shifts to target an interest rate lower than previously (i.e. it will lend on the repo market at a new lower rate), then any bank wanting to borrow will be foolish to borrow at a higher rate. Conversely, if the central bank announces a new higher target rate, any bank wanting to lend will be foolish to accept a lower rate than the central bank's target because it stands ready to trade at its stated rate. India targets the repo rate - see Article 16.2.