Article 16.2 India cuts interest rate to revive growth

By Amy Kazmin

Financial Times March 19, 2013

India’s central bank has lowered a key interest rate by 0.25% as it seeks to revive an economy that has slowed to the same pace as during the global financial crisis.

The Reserve Bank of India cut its key repo rate to 7.5%, as concerns about India’s faltering economy outweigh worries about persistently high inflation.

But in its outlook, the central bank warned that the ‘headroom for further easing remains quite limited’, with inflation expected to remain stuck at levels that are ‘not conducive for sustained economic growth’.

The RBI also left the cash reserve ratio unchanged, disappointing many who had expected a slight reduction.

India’s economy grew just 4.5% from October to December, the slowest pace in 15 quarters - sharply down from the near double-digit growth rates recorded earlier in the decade.

Indian businesses have been complaining that high interest rates, coupled with policy gridlock on such issues as land acquisition policies, are constraining economic expansion.

Lending facility/discount rate changes

There is an option for banks to borrow additional reserves from the central bank, the standing lending facility. In some countries it is called discount window borrowing. The European Central Bank offers loans at the marginal lending rate in its marginal lending facility. In May 2014 when the main refinancing rate was 0.25%, if banks were forced to borrow under the marginal lending rate they paid 0.75%. In the US, the Federal Reserve offers (a) a primary credit discount rate for very short-term (usually overnight) lending to banks in sound condition, set in May 2014 at a level of 0.75% (at a time when the Fed Funds target was 0-0.25%); (b) a secondary credit discount rate for banks not in sound financial condition, where the interest rate is even higher at 1.25%; and (c) a seasonal discount rate for special situations.

In the UK, with the target Bank Rate at 0.5% in May 2014, the BoE would lend to banks under the operational standing lending facility at 0.75%. In more normal times the standing lending facility/primary credit discount rates are usually 100 basis points above the target Bank Rate.The BoE's operational standing lending facility is designed to allow banks a way of managing unexpected day-to-day shortages of reserves, which may arise due to technical problems in the commercial bank's own systems or in marketwide payments and settlement infrastructure. These funds are available in unlimited size. Standing lending facility borrowing is used by generally sound banks in normal market conditions on a short-term basis, typically overnight, at a rate above the normal open market target rate. But given the higher interest rate it is used sparingly.

For banks in severe shock there is usually another facility, which is even more expensive to borrow under. The BoE also has a discount window facility, which is aimed at banks experiencing firm-specific or market-wide shock. Rather than cash being borrowed from the BoE, the more usual form of borrowing is UK government bonds, gilts, which are lent for up to 30 days (or 364 days for an additional fee). The BoE hands over the gilts and receives in return less liquid collateral in a repo-type deal. These less liquid securities are much more risky than sovereign bonds, e.g. the collateral put up could be securitised bonds or a portfolio of corporate bonds. Once it is in receipt of the gilts the borrowing bank then obtains cash by lending them in the market - another repo. The discount window facility borrowing is designed only to address short-term liquidity shocks and the fees are set to ram home the extraordinary nature of this type of help with reserves. The BoE states that ‘the fees are set to be unattractive in “normal” market conditions so that participants use the facility as back up rather than a regular source of liquidity'.

In normal conditions banks will be most interested in using the standing lending facility. This type of borrowing can allow an increase in reserves in the financial system and therefore an increase in the money supply. When the standing lending facility loans are repaid the total amount of reserves, the monetary base and the money supply will fall.

If the interest premium (above Bank Rate, Fed funds rate, etc.) charged in the standing lending facility falls then an increasing number of banks will be tempted to cut things fine on excess reserve levels, leading potentially to more borrowing at the lending facility rate. If the premium rises then few banks will borrow this way. Thus banks rein in their lending to customers for fear of having to borrow themselves at punitive interest rates. The standing lending facility rate acts as a back-stop for the open market target interest rate. The money market rate will not rise above the standing lending facility rate so long as the central bank remains willing to supply unlimited funds at the facility rate.

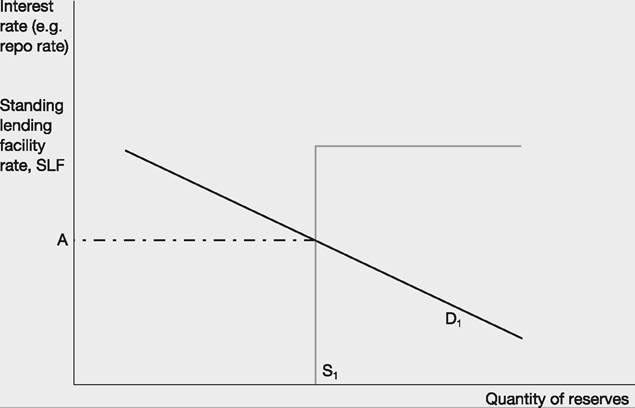

If we introduce the possibility of large volumes of supply of money (reserves) from the central bank at a high interest rate then we have the upside-down L-shaped supply curve shown in Figure 16.4. If the demand curve D1 is the

Figure 16.4 Standing lending facility availability changes the supply curve

relevant demand schedule for aggregate bank reserves then the horizontal portion of the curve - bank borrowing from the central bank at the standing lending facility rate - does not come into play. Banks will continue to borrow and lend in the money markets but not from the central bank,[39] and the equilibrium interest rate remains at A. This is the case most of the time: changes in the standing lending facility rate have no direct effect on the market interest rate.

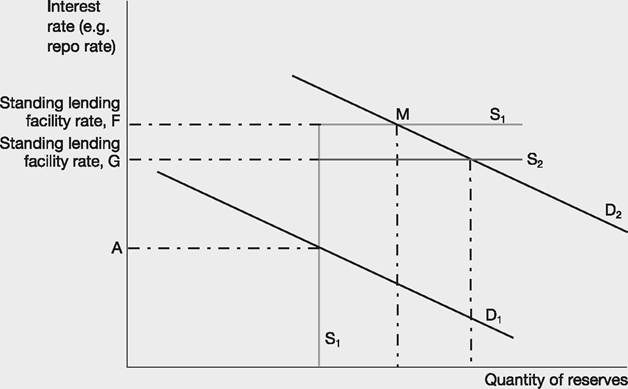

Now, consider the case where there has been a shock to the system and banks increase their demand for reserves all the way along the curve - the demand curve has shifted to the right, from D1 to D2 in Figure 16.5.

Indeed, it has shifted so much that banks now borrow from the central bank at the standing lending facility rate to top up their reserves - see demand curve D2 intersecting the supply curve at the standing lending facility rate at point M. Now, if the central bank moves the lending facility rate up or down the point of intersection with the demand curve shifts and thus the market interest rates change. If the central bank wanted to lower interest rates it could move the lending facility rate from, say, F to G, leading to increased borrowing from the central bank and an increased money supply.

Figure 16.5 Standing lending facility rate lending

A few decades ago adjusting the standard lending facility/discount rate was the main way in which many central banks effected monetary policy, but the problem with this approach became increasingly apparent. It is difficult to predict the quantity of lending facility/discount rate borrowing that will occur if the lending facility/discount rate is raised or lowered, and so it is difficult to accurately change the money supply. Today changes in this rate are used to signal to the market that the central bank would like to see higher or lower interest rates: a raising indicates that tighter monetary conditions are required with higher interest rates throughout; lowering it indicates that looser, more expansionary, monetary conditions are seen as necessary.

Reserve requirement ratio changes

The power to change the reserve requirement ratio is a further tool used by central banks to control a nation's money supply. A decrease in the reserve requirement ratio means that banks do not need to hold as much money at the central bank (the demand curve for reserves shifts to the left) and so they are able to lend out a greater percentage of their deposits, thus increasing the supply of money. The new loans result in consumption or investment in the economy, which raises inflows into other banks in the financial system and the deposit or money multiplier effect takes hold, as shown in the Example' Money creation - the deposit multiplier' above.

The process of borrowing and depositing in the banking system continues until deposits have grown sufficiently such that the new reserve amounts permit just the right amount of deposits - the target reserve ratio is reached. At least that is the economic theory, but the recent financial crisis taught us that it is not quite as simple as that if individuals, corporations and banks lack confidence to borrow and lend.The main drawback to using changes in the reserve ratio, even in ‘normal times', is that it is difficult to make many frequent small adjustments because to do so would be disruptive to the banking system (e.g. a sudden rise can cause liquidity problems for banks with low excess reserves). Open market operations, however, can be used every day to cope with fluctuations in aggregate monetary conditions. Article 16.3 discusses the lowering of reserves in China to stimulate the economy.