Article 16.3 Chinese shares fall despite bank reserve ratio cut

By Gabriel Wildau and Patrick McGee

Financial Times February 5, 2015

Chinese equities fell despite early gains on Thursday after the People's Bank of China loosened policy earlier than anticipated during London trading hours on Wednesday.

China's central bank cut the required reserve ratio for its banks as it stepped up efforts to counter the impact of capital outflows and encourage banks to boost lending amid fresh data showing a weakening economy.

The Shanghai Composite lost 1.2%, having jumped 2.3% at the open on Thursday.

A survey published on Sunday revealed that China's manufacturing sector - a key growth driver - contracted in January for the first time in more than two years. This followed news last month that China experienced its weakest GDP growth in 24 years last year.

In addition, China suffered its largest capital outflow on record in the fourth quarter last year, according to balance of payments data released on Tuesday. The deficit of $91bn on the capital and financial accounts was the worst since quarterly data were first compiled in 1998. China's foreign exchange reserves also fell as investors sold renminbi and bought foreign currency.

‘The most important reason for the cut is liquidity demand in the banking system,' said Haibin Zhu, chief China economist at JPMorgan in Hong Kong...

The required reserve ratio, known as the RRR, specifies the portion of a commercial bank's deposits that must be held on reserve at China's central bank, where it is unavailable for loans and other investments.

For most of the past decade, ‘twin surpluses' on both the current and capital accounts swelled China's foreign exchange reserves and its domestic money supply. In response, the People's Bank of China (PBOC) raised the RRR steadily as a way to sterilise these inflows and prevent inflation. The RRR for China's biggest banks rose from 8% in 2005 to a high of 20.5% in late 2012.

Wednesday's cut of 0.5% brings that rate down to 19.5% - although this is still much higher than any other major economy. With inflows now reversing, economists expect at least one more RRR cut this year.

In depth

The central bank has tried to tread a fine line over the past year by providing a targeted stimulus to support the slowing economy, without exacerbating financial risks by unleashing a new credit binge like the one deployed in response to the 2008 financial crisis.

The central bank's latest easing move followed a cut in benchmark interest rates in November and a series of targeted easing measures last year, which included direct loans worth more than $80bn to specific banks, and RRR cuts for small lenders.

In addition to Wednesday's broad-based cut, the PBOC announced further targeted cuts for so-called city commercial banks, whose loan books tilt towards small business and the agricultural sector - two areas that have long complained of difficulty obtaining credit.

In addition to responding to domestic conditions, economists say the PBOC's move is also a reaction to moves by central banks in other countries, including the recent decision by the European Central Bank to pursue an ambitious programme of quantitative easing.

‘Various countries are raising the stakes when it comes to monetary policy easing,' said Cao Yang, an analyst at Shanghai Pudong Development Bank. ‘China's RRR cut is a move to keep pace.'

id="Picutre 220" class="lazyload" data-src="/files/uch_group74/uch_pgroup310/uch_uch7286/image/image220.jpg">

Source: Wildau, G. and McGee, P. (2015) Chinese shares fall despite bank reserve ratio cut, Financial Times, 5 February.

2015

Choosing between targeting the quantity of reserves and targeting an interest rate level

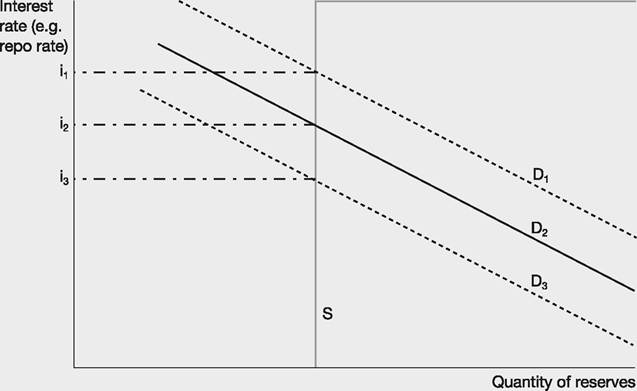

Which is more likely to lead to stable monetary conditions: (a) targeting a fixed aggregate supply of money, or (b) targeting a particular overnight interest rate? Or consider an alternative question leading to a similar conclusion: is it possible to target both the quantity of reserves and the interest rate simultaneously?

To provide answers, examine the situation in Figure 16.6.

The central bank expects the aggregate demand curve to be as described by the solid demand line, D2. However, the reality is that the authorities have only a vague idea of where the demand schedule is. It might fluctuate up to the higher dashed line or down to the lower one as, say, unexpected changes in deposit levels increase or decrease commercial banks' desire to hold excess reserves. Thus, if the central bank rigidly maintains the supply schedule, S, the result could be that from one day to the next overnight interest rates could be quite volatile, fluctuating

Figure 16.6 Targeting reserve levels

from, say, i1 to i3, as the demand curve moves left and right. Such a rapidly shifting overnight rate can be disruptive.

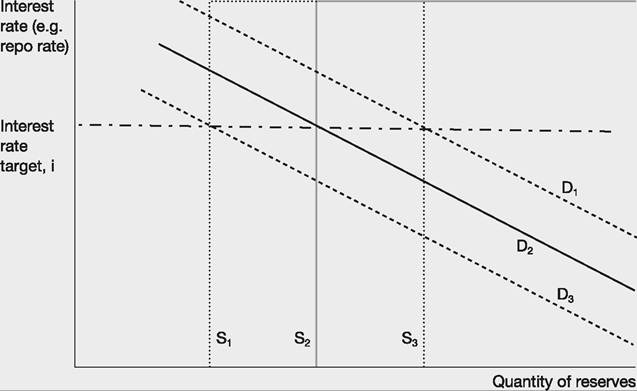

The alternative approach is to target the overnight interest rate and to therefore fine-tune the supply of reserves to achieve the desired interest rate stability - see Figure 16.7. Here the reserves demand curve fluctuations can be accommodated by the central bank response of quickly implementing open market operations to pump in or drain reserves. If the D1 curve comes into play with higher reserves demanded at each interest rate then the central bank can increase supply to S3 by buying securities, achieving equilibrium at interest rate, i. If demand for reserves is low, D3, then the central bank can move to supply only S1, leaving equilibrium at i. It can do this by selling securities or simply not supplying fresh reserves as repo positions come to an end. Thus, the supply of reserves is determined by the commercial banks' aggregate demand for reserves, which is accommodated by the central bank through open market operations in targeting the price of credit.

Interest rate targeting is generally preferred because the central bank can quickly observe changes in the rate, whereas measuring aggregate quantities of reserves involves a time lag.

It can also intervene quickly to control the interest

Figure 16.7 Targeting the interest rate

rate, whereas reserves are not completely controllable. Also, central banks have generally concluded that there is a closer link between interest rates and the goal of the inflation level in the economy than that between monetary aggregates and inflation. For these reasons central banks generally target short-term interest rates.

Following the logic of targeting the overnight interest rate, some monetary economists emphasise that it is the price of credit that determines the quantity of broad money created by banks. So, rather than targeting a deposit multiplier through altering the quantity of the monetary base in an assumed stable ratio of broad money to narrow money, central banks set overnight interbank interest rates, which affect other interest rates. The level of interest rates throughout the economy (mortgages, deposit interest, etc.) creates the demand for broad money - banks may become more or less willing to lend, borrowers become more or less willing to borrow, pay down debt or spend, depending on the interest rates. The impact on broad money then has an impact on the quantity of base money demanded. Thus the demand for reserves is a consequence rather than a cause of banks making loans and creating broad money. Commercial bank decisions on the amount they make available for loans depends on the perceived profitability of lending, which in turn depends on a number of factors, including degree of confidence in a growing economy and the cost of funds that banks face, which is influenced strongly by the interest rate paid on reserves at the central bank.

A central bank decision to lower overnight interest rates is likely to increase the amount of broad money, as long-term loan rates fall and the volume of loans rises. The larger volume of spending and broad money in the economy is likely to cause banks and customers to demand more reserves and currency.

Thus the deposit or money multiplier is seen as working in a reverse way to that described earlier. However, bear in mind that whichever direction the causation goes, broad money has to backed up with reserves. Thus the reserves level can limit changes in the amount of broad money. Interest rates, reserves and long-term bank lending are intimately linked, and controllable, to some extent, by the central bank.Quantitative easing

In extreme circumstances a central bank may find that interest rates have been reduced to the lowest level they could go and yet still economic activity does not pick up. People are so shocked by the crisis - increased chance of unemployment, lower house prices, lower business profits - that they cut down their consumption and investment regardless of being able to borrow at very low interest rates. This happened in 2009-2014. Annualised short-term interest rates in eurozone countries were less than 0.1%, in the UK they were 0.5% and in the US they were between 0% and 0.25%. Clearly, low short-term interest rates were not enough to get the economy moving, even with the additional boost of government deficit spending to the extent that up to one-eighth of all spending was from government borrowing.

In response, another policy tool was devised: quantitative easing. This involves the central bank electronically creating money (‘printing money', but without any more bank notes) which is then used to buy assets from non-bank investors in the market. Thus pension funds, insurance companies and other non-financial firms can sell assets, mostly long-term government bonds (but can include mortgage-backed securities and corporate bonds), and their bank accounts are credited with newly created money (broad money increases). This raises bank reserves. More significantly, the increased demand for government bonds raises their prices and lowers interest rates along the yield curve - so the main influence is on interest rates for medium- and long-term bonds.

Also, it is hoped that the new cash will be used to invest in other assets such as shares pushing up equity issuance, prices and lowering required returns on these assets, thus stimulating investment in companies.In the UK the BoE bought so many bonds in 2009-2013 that it now owns about one-third of all gilts, pushing ten-year yields at times to only 1.5%. Between 2008 and 2014 the Fed bought more than $3.5 trillion bonds (mostly mortgage-backed and government). However, central banks are increasingly anxious about the consequences of ceasing quantitative easing - interest rates might rebound dramatically and devastatingly. Some economists are also worried that inflation might take off at some point given all the extra cash floating about (optimists argue that the central bank can just sell the bonds or wait until redemption to suck cash out of the system, others are not so sure).Japan launched the most audacious quantitative easing plan in 2013: $1.4 trillion in less than one year - see Article 16.4. Many suspect that bubbles are being created in bond and other asset markets.