Article 16.4 Bank of Japan opens floodgates

Financial Times April 5, 2013

This week, Haruhiko Kuroda, the new governor of the Bank of Japan, launched perhaps the boldest ever experiment by the central bank of an important country.

It is not a revolution in monetary policy, since the BoJ is following the intellectual lead of Ben Bernanke’s Federal Reserve. But it is a revolution in Japanese thinking and in the magnitude of the planned action. The Bank of Japan risks doing too much. But Japan already knows well the costs of doing too little. That lesson is one the European Central Bank may yet learn.The BoJ has promised to turn Japan’s slow-motion deflation into inflation of 2% within two years. To achieve this transformation it has now promised to raise purchases of government bonds from a monthly rate of Y2tn ($21bn) to one of Y7tn, to double the average maturity of new bond purchases to seven years and to double the monetary base to Y270tn by the end of 2014.

This is still monetary policy, since the BoJ intends to reverse the purchases. The aim is to force holders of government liabilities to move into riskier assets. The result, it is hoped, will be higher prices for riskier assets, including equities; a weak yen, a stronger economy and so higher inflation.

FT

Source: Financial Times, 5 April 2013.

© The Financial Times 2013

The floor system

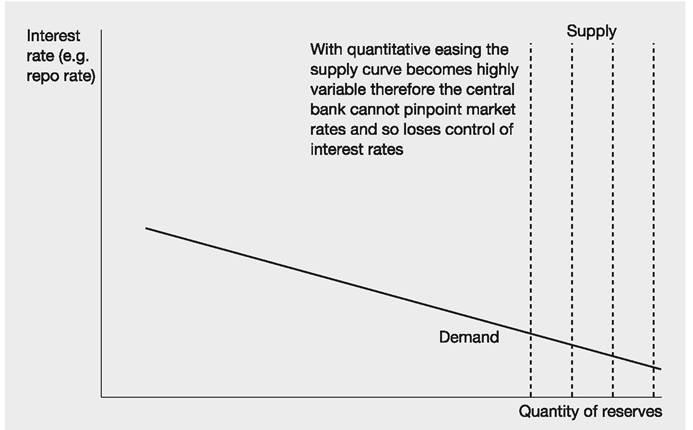

Over the decades central banks have tried all sorts of levers to control inflation, money supply and interest rates. Currently, a popular approach is the floor system. This has been prompted by the pressures caused by the enormous amounts of money pumped in to counteract depressed appetite to invest, borrow and lend.

With quantitative easing the central bank is creating large quantities of reserves far beyond that needed to achieve its target interest rate. Not only this, but the quantity of money goes up in large increments, so the supply curve is all over the place - view the supply curve in Figure 16.8 as moving frequently left to right and back again.

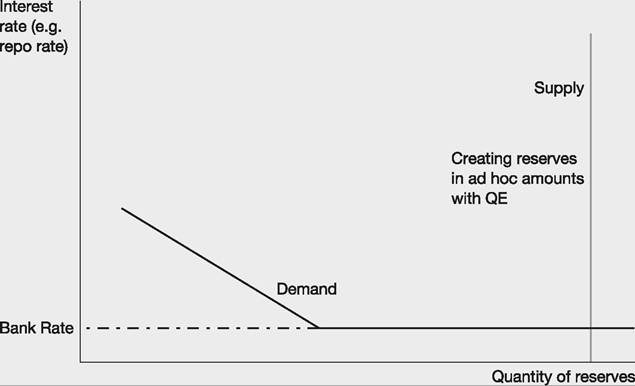

This could lead to uncertainty. To put a floor under the fluctuations the central bank introduces a policy of paying its target Bank Rate of interest (0.5% in the UK) to all reserves lodged by banks with it (even excess reserves). Because commercial banks will not lend their surplus reserves to each other at rates lower than can be obtained by depositing them at the central bank, this has the effect of flattening the demand curve for reserves after the point where there

Figure 16.8 First change: extraordinary circumstances calls for quantitative easing

Figure 16.9 Second change: a floor system, where all bank reserves held at the central bank are remunerated at Bank Rate (Fed Funds rate, etc.)

are sufficient reserves in the system for banks to manage their day-to-day liquidity needs - see Figure 16.9.

This allows the central bank to supply unlimited amounts of reserves without affecting the overnight interest rate - the supply curve can move but the overnight interest rate stays at, say, 0.5%. The central bank establishes a benchmark short-term risk-free interest rate. This will influence the rates that commercial banks are willing to charge or pay on short-term loans or borrowings in the market.

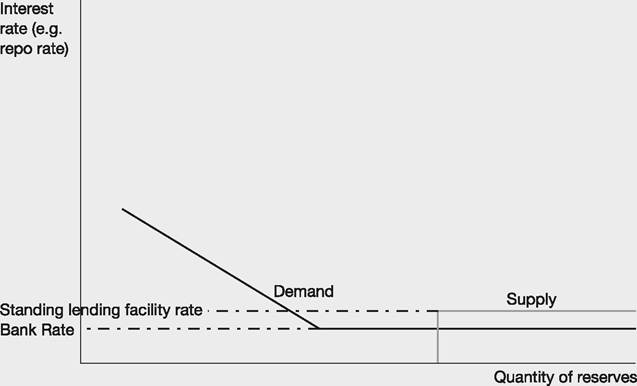

We could, for completeness, also add the standing lending facility rate (0.75% at the time of writing) to the diagram, which would create an upper boundary for interest rates - see Figure 16.10. Commercial banks can borrow as much as they want at this rate and so market interest rates for overnight money will not go above this. Commercial banks will typically be unwilling to borrow in the repo market on worse terms than those available from the central bank. Thus short-term interest rates in the markets are collared within the range bounded by the Bank Rate and the standing lending facility rate regardless of the extent of high-powered money creation. In the UK the short-term interest rate is

Figure 16.10 A floor system combined with a standing lending facility

unlikely to be lifted higher than the Bank Rate given the sheer quantity of reserves sloshing about the banking system, where there are plenty of banks willing to lend overnight to other banks at 0.5%. Collectively, banks would need to come under severe strain for the upper limit of the corridor (0.75%) to be tested.

What did you think of this book?

We’re really keen to hear from you about this book,

so that we can make our publishing even better. Please log on to the following website and leave us your feedback.

It will only take a few minutes and your thoughts are invaluable to us.

www.pearsoned.co.uk/bookfeedback