Article 3.11 Local authorities turn to capital markets

By Elaine Moore

Financial Times September 30, 2014

Public sector debt is piling ever higher, driven by the lure of low borrowing costs and strong investor demand.

Borrowers ranging from supranational organisations like the World Bank to individual towns and states are issuing record amounts of debt.

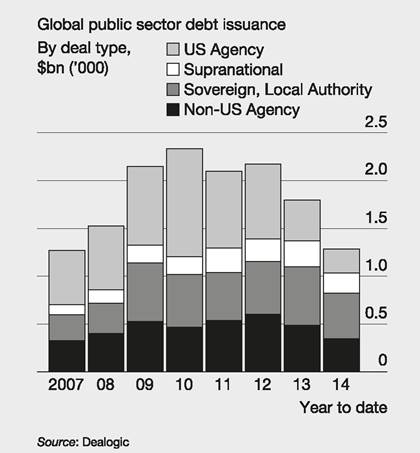

In theory, the sudden rise in debt issued by public sector organisations in the wake of the financial crisis should fall back as the economy recovers. But so far, that has not happened.

Last year, supranationals such as the World Bank, European Stability Mechanism and others issued $267bn - a record level of debt. Local authorities are also borrowing more than ever - issuing $7.2bn in bonds so far this year compared with $3.7bn by the same point last year.

Collectively, quasi-government borrowers make an unwieldy group. At one end of the scale are enormous organisations created by multiple governments in response to political or economic crisis.

At the other end are sub-government authorities with the ability to borrow on capital markets to fund local projects.

Between the two are government-sponsored banks such as Germany's KfW and AFD in France, which fund programmes with specific economic or social functions. These agencies borrowed slightly less last year than in 2012, but still issued a sum of debt that exceeded borrowing in 2010.

All tend to boast similar credit ratings to the governments that back them, and offer a slight bump in yields to investors.

The Belgian sub-sovereign Flemish Community, for example, offers about 40 basis points more than the equivalent Belgian five-year bond, according to Rabobank.

‘Traditionally you get at least a few basis points over sovereign debt yields,' says Matthew Cairns, strategist at Rabobank. However, he points out that the investor base for public debt has broadened from conservative central banks to global banks under the direction of new regulation.

This, combined with the fall in governments, afforded the highest, triple-A credit rating, and the drop in debt issued by US agencies - such as Fannie Mae and Freddie Mac - is pushing up order books.‘The yield makes the sector attractive, but now there is more demand than paper available and yields are falling. We don't know how far that can go,' says Mr Cairns.

Investor appetite for public sector debt has become intense, says George Richardson, head of capital markets at the World Bank Treasury.

In the UK, local authorities are hoping to kick start a market in municipal bonds to take advantage of low global borrowing rates by creating central agencies.

The UK's Local Government Association has said that creating an agency able to issue debt on behalf of councils could save them more than £1bn in borrowing costs.

More than £4.5m has so far been raised to create the Local Capital Finance Company, and the organisers say they hope to raise the first bond by March or April 2015.

Bankers say the success of municipal bond agencies in Nordic countries, Switzerland, Italy and now France, bodes well.

In Sweden, Kommuninvest raises sums that standalone councils would not be able to do, something UK councils will be aware of. Launched in the late 1980s, by the end of last year Kommuninvest's total lending had reached $28bn.

And in the US, the vast municipal bond market, which reached $3.7tn by the end of last year, is an established source of saving for households.

FT

Source: Moore, E. (2014) Local authorities turn to capital markets, Financial Times,

30 September.

Agencies

Agencies (government-sponsored enterprises, GSEs) are set up to fulfil a public purpose and while the debt they issue is not always explicitly guaranteed by the government, there is a strong implication or assumption that the state will step in to make good any shortfall. In the US, a handful of organisations (quasi-governmental) dominate the agency bond market, including the Federal Home Loan Bank System (FHLBS), the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac),[13] Tennessee Valley Authority (TVA) and the Student Loan Marketing Association (Sallie Mae).