Article 3.10 EM bonds: are you nuts? Investors are buying bonds with ever less discrimination

Lex column

Financial Times June 11, 2014

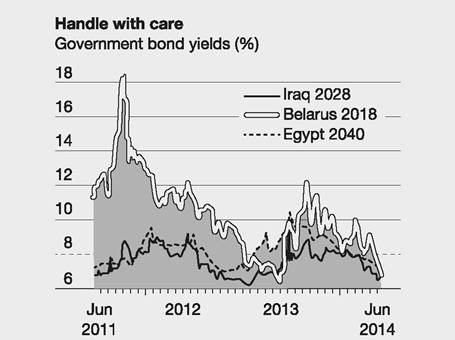

On Tuesday a transnational group of terrorists seized Iraq's second-largest city, Mosul. The army did not resist. Abandoned equipment and millions of dollars left in Mosul's banks are now at the disposal of the Islamic State of Iraq and the Levant.

But never mind that. Would you like to take the government's side for a yield of 6.7%? That is where risk is being priced in Iraq's US dollar bond due in 2028. This would be after the market had digested ill tidings from Mosul.Not so sure of the risk-reward there? Investors may prefer to buy into the stability of the regime of President Abdel Fattah el-Sisi, with Egyptian hard-currency bonds that mature in a quarter of a century. These yield just below 7%. How about Belarus? There is a 6.5% yield on bonds due in 2018. Trust that no revolution in Minsk disrupts cash flows before then.

The point here is not simply that some dodgy sovereigns are being priced with low yields. Risk assets are being bid up generally, even as US Treasury yields have fallen so far in 2014. Foreign-currency EM bonds are still cheaper overall than high-yield

Sources: Data from Thomson Reuters Datastream; Bloomberg

developed-market credit. Even so, investors are beginning to buy these bonds with ever less discrimination.

A brave investor may also argue that fundamentals favour the Iraqi bond. The country sells lots of oil. But 6.7%? EM bond risks may not seem so high when risk has become favoured everywhere. That is not the same as riskless.

FT

Source: Lex column (2014) EM bonds: are you nuts?, Financial Times, 11 June.

Local authority/municipal/quasi-state/ agency bonds

Local authority, municipal, quasi-state and agency bonds are issued by governments and organisations at a sub-national level, such as a county, city or state.

They pay a rate of interest and are repayable on a specific future date, similar in fact to Treasury bonds. They are sometimes called semi-sovereigns or sub-sovereigns. They are an important means of raising money to finance developments, buildings or expansion by the local authority or agency. They are riskier than government bonds (the issuers cannot print their own money as governments might) as from time to time cities, counties, etc. do go bust and fail to pay their debts. However, many issuers, particularly in Europe and the US, obtain bond insurance from a private insurance group with a top credit rating, guaranteeing that the bond will be serviced on time. This can boost an issue's credit rating, as its rating will then be based on the insurer's credit rating, which reduces the interest rate the sub-sovereigns pay.In the UK, local authority bonds or quasi-state bonds are out of favour at the moment, although Transport for London issued a 25-year bond in 2006, and in 2012-2013 raised £1.6 billion with four bond issues with maturities ranging from 5 to 33 years. There has been talk of issuing a ‘Brummie' bond (by Birmingham City Council), but this has yet to be finalised. In July 2013 the city of Leeds raised more than £100 million with an oversubscribed bond issued to finance a social housing project.

US municipals

Municipal bonds (‘munis', pronounced mew-knees) are issued by state and local government departments and special districts. Much of the infrastructure

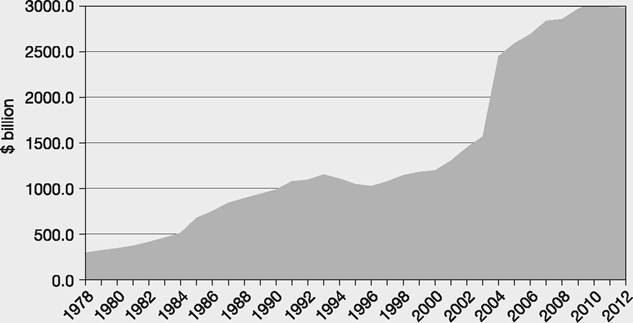

Figure 3.9 State and local government debt in the US over time

Source: Data from Financial Accounts of the United States, June 2013

in the US has been and still is financed by municipal bonds, the first of which was issued in 1812. These bonds have proved to be a valuable source of finance for local communities.

The US muni market is enormous, with a total in outstanding bonds of over $3 trillion in 2012 - see Figure 3.9.

Special districts are independent government bodies managed by a board and they provide some type of service to a particular area, e.g. airports, ports, roads, bridges, public transport, parking facilities, fire services, libraries, parks, cemeteries, hospitals, nursing homes, conservation, sewerage, waste disposal, stadiums, water, electricity and gas. They tend to be issued in minimal denominations of $5,000.General-obligation bonds offer the bond holder a priority claim on the general (usually tax) revenue of the issuer in the event of a default, whereas a holder of a revenue bond receives interest and principal repayment from the revenues of a particular project, e.g. the income from a toll bridge.

Some municipal bond issuers have made bad investment decisions and have gone bust, notably those issued by Orange County, California, in 1994, where the county treasurer lost more than $1.5 billion; by Jefferson County, Alabama, in 2011, which went bankrupt owing $4.2 billion; and by the city of Detroit, Michigan, the former hub of the US motor industry, which in 2013 went down owing $18 billion. Investors who bought bonds where the issuer has gone bankrupt face losing some or all of their investment. Despite these few well-publicised defaults, overwhelmingly municipal bonds provide a valuable service to their communities and their investors with very few problems.

Investors in US municipal bonds issued by state and local governments are usually exempt from federal income tax on the interest they receive. In many states the income is exempt from state taxes. Because of these concessions they usually trade at lower yields to maturity than US government bonds. The investor groups dominating the municipal securities market are households (some investing via mutual funds), commercial banks and some insurance companies able to benefit the most from the tax concessions. Municipal bonds are less liquid than federal government bonds in the secondary market, so investors may have greater difficulty selling in some of the smaller issues and the dealer spreads (bid-ask) can be wide.

Some municipals outside of America

In Japan, the Japan Finance Organization for Municipalities (JFM) established in 2008, issues long-term bonds. Most of these are domestic bonds but some are international issues. The amount outstanding in 2014 was about ¥22 trillion (US$220 billion), which provided loans to finance local projects.

The German Lander (federal states) are also large issuers, with more than ˆ350 billion of bonds outstanding in 2014, about the same as the Netherlands. There are also quasi-state organisations issuing bonds in Europe. In France, Societe Nationale des Chemins de Fer Franςais (SNCF, the state-owned French railway operator), and in Germany, Deutsche Bahn (DB, the state-owned German railway company), are just some of the institutions that have issued bonds. Sweden and Finland both run schemes where local communities join together to issue bonds to raise finance. By keeping the schemes local, the risk is reduced so that the bonds receive higher credit ratings. Article 3.11 discusses some local authority bonds.