Article 9.1 ADP: commercial success

The Lex team

Financial Times April 21, 2014

Credit ratings matter. But not always the ones that get the most attention. Fortunately ADP, the payroll processing mainstay, knows the difference.

In early April, after it announced a spin-off of its Dealer Services business - a unit that provides software to motor sellers - ADP lost its rarefied AAA rating. Perhaps that stung. But the spin-off still looks like a canny move for shareholders. And just as important, ADP managed to keep its top-tier commercial paper rating that is central to its business model.Since ADP is an intermediary that makes payroll for employees and withholds taxes for the government on behalf of its client companies, it happens to maintain a large cash portfolio or ‘float’. That float totalled $28bn at the end of the last quarter. It chooses to invest that money in medium-term bonds that generate interest income that flows straight to earnings. But with the cash tied up in these investments, it relies on commercial paper - short-term debt that matures in less than a year and these days costs about 0.2% - to fund working capital.

Commercial paper is typically available to companies of investment grade quality. However, during the credit crisis of 2008 even borrowers who had the A-2/P-2 rating, the second-highest CP ranking, were locked out of that market.

The ADP Dealer Services business constitutes only about 15% of ADP’s current revenue and has been estimated to be worth $5bn (ADP’s current market cap is $37bn). With its debt capacity, the motor business will send back $700m in cash to ADP that will be used to buy back shares. And so ADP will remain a massive business, but only focused on payroll and other human resource functions such as benefits and recruiting management. With its formidable size, its CP rating of A-1/P-1 went untouched. The perfect outcome, if you happened to notice.

FT

Source: Lex column (2014) ADP: commercial success, Financial Times, 21 April.

via a money market fund: the fund buys a range of CP issues (and other instruments) and so, while it is committed to hold each CP to maturity, because it is well diversified, with many securities maturing every day, it is able to pay out to money market fund investors when they demand it. The Federal Reserve Board posts the current rates being paid on US commercial paper by non- financial and financial firms on its website - see Table 9.8.

Table 9.8 US Federal Reserve Federal funds rate and examples of commercial paper rates in August 2014, per cent annualised

| Instruments | 2014 Aug 25 | 2014 Aug 26 | 2014 Aug 27 | 2014 Aug 28 | 2014 Aug 29 | Week ending | 2014 Aug | |

| Aug 29 | Aug 22 | |||||||

| Federal funds (effective) | 0.09 | 0.09 | 0.09 | 0.09 | 0.07 | 0.09 | 0.09 | 0.09 |

| Commercial paper | ||||||||

| Non-financial | ||||||||

| 1-month | 0.08 | 0.07 | 0.07 | 0.07 | 0.06 | 0.07 | 0.10 | 0.08 |

| 2-month | 0.09 | 0.10 | 0.09 | 0.10 | 0.09 | 0.09 | 0.10 | 0.09 |

| 3-month | 0.11 | 0.12 | 0.11 | 0.12 | 0.11 | 0.11 | 0.11 | 0.11 |

| Financial | ||||||||

| 1-month | 0.09 | 0.07 | 0.07 | 0.08 | 0.07 | 0.08 | 0.09 | 0.09 |

| 2-month | 0.12 | 0.11 | 0.12 | 0.11 | 0.12 | 0.12 | 0.12 | 0.11 |

| 3-month | 0.13 | 0.13 | 0.14 | 0.13 | 0.13 | 0.13 | 0.13 | 0.13 |

Source: Data from www.federalreserve.gov/releases/h15/current/

Note issuance facility (NIF)

Note issuance facilities (variously known as revolving underwriting facilities, RUFs, note purchase facilities, commercial paper programmes and Euronote facilities) were developed as services to large corporations wanting to borrow by selling commercial paper or medium-term notes into the financial markets.

The largest corporations often expect to be selling a series of different CPs or MTNs issues over 5-7 years. Instead of handling each individual issue themselves as the need arises they can go to an arranging bank(s) at the outset, which will, at various points over the, say, five years, approach a panel of other banks to ask them to purchase the debt as it becomes needed. The loan obligation can be in a currency that suits the borrower at the time. The borrower can also select the length of life of the paper (say, 14 days or 105 days) and whether it pays fixed or floating interest rates.If there is a time when it is difficult to sell the paper to the banks then the borrower can turn to those banks that have signed up to be underwriters of the facility to buy the issue, or, depending on the deal, borrow from the bank or banks in the syndicate. Underwriters take a fee for these guarantees. Most of the time they do not have to do anything, but occasionally, often when the market is troubled, they have to step in.

Some people draw a distinction between an NIF and an RUF: with an RUF the underwriting banks agree to provide loans should the CP/MTN issue fail, but under an NIF they could either lend or purchase the outstanding CP or notes. However, these definitions do not seem to be rigidly applied.

By allowing borrowers the choice at each point of borrowing of either drawing a loan from the bank(s) at an agreed spread over Libor or selling CP/MTN through banks, the borrower gets the best of both worlds: a bank loan (committed bank facility) fallback, or access to the financial markets in corporate debt instruments. Which is chosen depends on interest rates at the time. One- off fees are payable for arrangement and annual fees for bank participation (actual lending) and commitment (standing ready to lend).

An insider's view

Opus plc agrees a £300 million NIF with a bank for six years. This lead bank asks other banks to join the syndicate.

Opus obtains a credit rating for commercial paper that it might issue. Opus can repay funds drawn down under the NIF at will, without penalty. Opus decides it would like to borrow £150 million starting in eight days for a six-month period. It tells the lead bank that it would like either to take a six-month loan at the rate stated in the NIF loan agreement, which is Libor + 95bp, or to issue CP to a predetermined syndicate of banks and dealers at the rate currently being offered by that dealer group. Currently, six-month Libor is 1.4%, thus the loan will cost 2.35% (annual rate) for six months. The lead bank comes back with the CP interest rate of 2.56%, so Opus decides to exercise its right under the NIF to borrow the £150 million from the banks. For the remaining five and a half years Opus will have the right to repay and then take out fresh loans or issue fresh CPs as the need arises.Really well-known creditworthy issuers can opt to avoid the cost of maintaining the backstop option of access to these loans (arrangement and participation fees) and simply rely on their ability to periodically attract lenders in the CP market under the NIF framework, but they still pay for swinglines and backup. That is, to obtain a credit rating CP issuers must have unused credit lines from banks to provide liquidity in the event of an interruption to the CP market preventing rolling over (the issue of new CP as old ones mature). Swinglines are bank commitments to provide same-day credit facilities to cover a few days of the CP maturities. Backup lines, sometimes uncommitted, are available for the longer maturities. There is a variety of liquidity backups that can be acceptable for this purpose, including cash and securities, but most CP issuers rely on credit lines from banks.

US commercial paper (USCP)

The largest commercial paper market in the world, by far, is the US, distantly followed by Japan, Canada, France, the UK and other developed economies. According to US law, because its maturity is less than 270 days, commercial paper does not have to be registered with the Securities and Exchange Commission, the main US financial regulator, and therefore is not subject to the time-consuming and costly process required by US federal regulations.

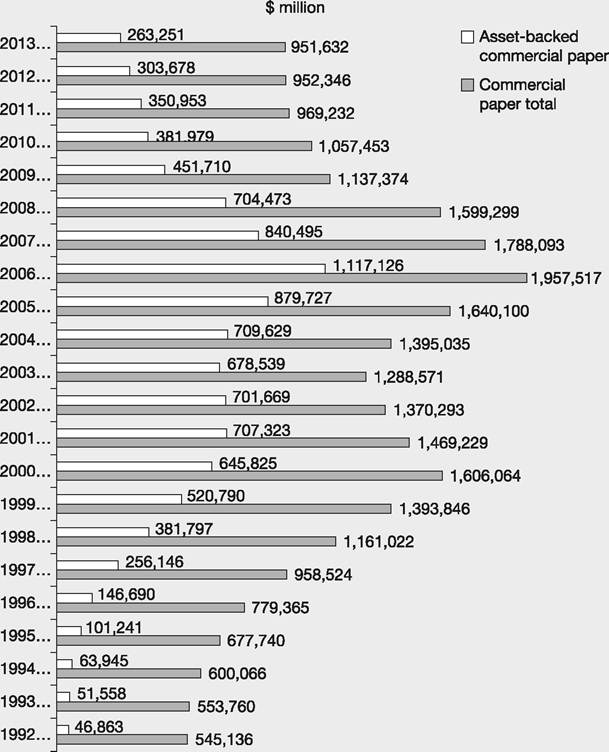

Figure 9.1 gives data for USCP from 1992. The amount of CP outstanding peaked in 2006 at nearly $2 trillion, of which half was asset-backed CP, before succumbing to the worldwide recession and loss of confidence and falling to around $1 trillion.Now about one-third is asset-backed commercial paper (ABCP), i.e. commercial paper secured on the collateral of assets - for example, the issuer has the right to receive monthly interest from mortgage payers, credit card holders, vehicle loans or some other regular income and uses the cash flow from these assets to pay the commercial paper when it becomes due and to provide collateral. The issuers of ABCP are usually special entities/companies set up by a bank. These, special purpose vehicles (SPVs) or structured investment vehicles (SIVs) or conduits, buy the assets (rights to mortgage interest, etc.) after raising money from issuing commercial paper. Thus they are ‘bankruptcy remote' from the parent company that supplied the assets - if they go bust the parent bank can still survive. Also they are perceived as less risky for the investors because of the security of the assigned assets, so if the parent goes bust the lenders still have the collateral (right to mortgage income, etc.) in the conduit.

At least that was the theory, but many conduits and their parent banks disappeared or nearly blew up in 2008 when they could not roll over the ABCP as they were accustomed to doing. When the financial crisis occurred many of these cash flows dried up, causing major problems for both issuers and holders of CP. Rolling over CP became difficult, confidence in this market plummeted and companies found it nearly impossible to obtain the CP funding on which they relied.

The commercial paper market can be very influential in corporate life. For example, in 2005, Standard & Poor's downgraded the commercial paper

Figure 9.1 US commercial paper outstanding, 1992-2013

Source: Data from www.federalreserve.gov

of Ford and General Motors, making their commercial paper unattractive to investors, leading to an increase in the cost of financing to these companies and reducing the global confidence in both the companies and their products. This contributed to their financial crisis in 2009, when General Motors was forced into bankruptcy.

Eurocommercial paper

Eurocommercial paper (Euro-CP) is paper that is issued and placed outside the jurisdiction of the country in whose currency it is denominated. So an American corporation might issue commercial paper denominated in Japanese yen outside of the control of the Japanese authorities and this is classified as Eurocommercial paper. The most common denominations are the euro, US dollar and GB pound, and the main place of issue is London.