Repurchase agreements (repos)

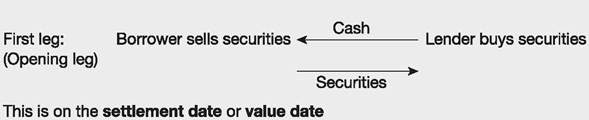

A repo is a way of borrowing large amounts of money for a short time using a sale and repurchase agreement in which securities are sold for cash at an agreed price with a promise to buy them back, or identical ones, at a specified (higher) price at a future date.

The interest on the agreement is the difference between the initial sale price and the agreed buy-back.

One, or a few days, later:

Because the agreements provide collateral backup for the lender, most often in the form of government-backed securities such as Treasury bills, the interest rate is lower than on a typical unsecured loan from a bank. If the borrower defaults on its obligations to buy back on maturity the lender can hold on to or sell the securities they bought in the first leg of the repo. In the absence of such a default if a coupon is payable on bonds during the term of the repo the original owner receives it, maintaining the same economic exposure to the security as though the economic ownership had not been sold. Thus, despite legal title to the securities being transferred, economic benefits and market risk are retained, so if the price of the security falls in the market it is the original owner who suffers the capital loss.

Repos have the advantage that they can be tailor-made to suit circumstances - the maturity can be any number of days and the amount fully variable, whereas many other forms of lending via financial securities tend to be for specific amounts and periods of time.

Repos are used very regularly by banks and other financial institutions to borrow large amounts of money from each other. Secured lending, such as repo lending, increased in volume following the financial crisis as more banks, etc.

became reluctant to participate in unsecured lending, deeming it too risky. Companies do use the repo markets, but much less frequently than the banks do. This market is also manipulated by central banks to manage their monetary policy and maintain stability in their economy (see Chapter 16).The term for repos is usually between 1 and 14 days, but can be up to a year, and occasionally there is no end date, an open repo. Overnight repos are the most common type, where the repurchase takes place the next day. Repos are useful for institutions holding large quantities of money market securities such as T-bills. They can gain access to liquidity through the repo for a few days while maintaining a high level of inventory in short-term securities.

Example 10.1

Repurchase agreement

A high street bank has the need to borrow £26 million for 14 days. It agrees to sell a portfolio of its financial assets, in this case government bonds, to a lender for £26 million. An agreement is drawn up (a repo) by which the bank agrees to repurchase the portfolio 14 days later for £26,005,285.48. The extra amount of £5,285.48 represents the repo rate of interest (an annual rate of 0.53%) on £26 million over 14 days.1 The sterling market day count basis is actual/365.

A reverse repo (RRP) is the lender's side of the transaction, an agreement in which securities are purchased with a promise to sell them back at an agreed price at a future date. Traders may do this to gain interest. Alternatively, it could be to cover another market transaction. For example, a trading house may need to obtain some Treasury bills or bonds temporarily because it has shorted them - sold them before buying - and needs to find a supply to meet its obligations, so it places a reverse repo order to get an inflow of the securities now. In a transaction, the terms repo and reverse repo are used according to which party initiated the transaction, i.e. if a seller initiates the transaction, it is a repo; if the transaction is initiated by a buyer, it is a reverse repo.

Example 10.2

Reverse repo

A bank has £45 million of spare cash for one day. A reverse repo agreement is drawn up, by which the bank agrees to buy £45 million of government securities from a borrower and sell them back the next day for £45,000,517.81. The extra amount of £517.81 represents overnight interest on £45 million at an annual rate of 0.42%.2

Repo deals are usually individually negotiated between the two parties (bilateral repos) and are therefore designed to suit the length of time of borrowing and the amount for each of them, thus there is usually little need for redemption before the agreed date. However, if circumstances change and the lender needs the money quickly it might be possible to arrange an off-setting reverse repo transaction.

Traditionally banks formed the largest group of borrowers in the repo markets, but now, as Article 10.1 makes clear, hedge funds, property funds and mutual funds have overtaken them.