Article 4.2 Battle is on to make bonds more transparent

By Stephen Foley

Financial Times May 1, 2013

A retail investor who gets her hands on an Apple bond can sleep pretty soundly. Not only can she be pretty sure the iPhone maker will be good for the interest payments.

If she decides, at some point in the future, to sell the bond, she can be pretty sure there will be a ready buyer there to take it off her hands at the prevailing market price.Would that this could be said for all bonds.

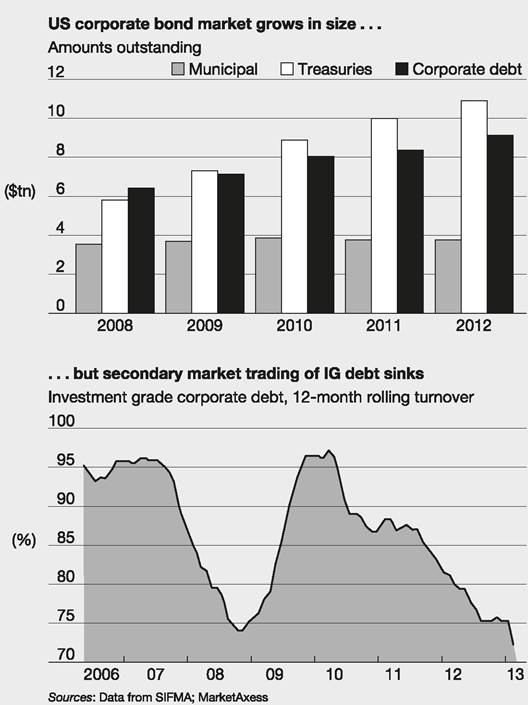

The scale of Apple’s $17bn debt offering means there ought to always be lots of bonds changing hands, and it will be easy to keep tabs on the price at which they are trading. They join an elite group of liquid corporate bonds. Most issues are not so easy to buy and sell.

In fact, of the 30,000 investment-grade corporate bonds trading in the US alone, only 20 trade more than ten times a day, according to MarketAxess. The proportion of the market that turns over in a year has slipped below 75%. The situation in municipal bonds, issued by state and local governments, is even worse.

And that means it is not so easy for a bond investor to be sure of the price she will have to pay if she puts in an order, or end up receiving if she tells her broker to sell.

At an industry forum earlier this month, the independent financial adviser Ric Edelman went as far as to claim investors were, in effect, being ‘lied to... We understand why that happens, that no deceit is intended, but they are shocked to discover what they thought was $105 was in fact $98 and don't know that until they have sold. We have huge education and disclosure problems within the industry.' The issue is getting scrutinised by regulators in the US and Europe like never before. Technological advances bring the tantalising prospect of more liquidity and there is already more transparency on price, at least after bonds have traded.

But the US Securities and Exchange Commission for one is sceptical that the benefits are flowing through to retail investors. They fear that the opacity of the market allows big dealers to take advantage by taking big mark-ups on trades.

The agency is considering demanding more transparency in corporate and municipal bond trading, although it has to weigh concerns that new rules could be detrimental to some big players in the market.

As for investors being able to see a price for their specific bond before they trade, that is a harder problem to crack. Traditionally, there has been no substitute to brokers calling round the trading desks of Wall Street to ask what a specific lot of bonds will fetch.

FT

Source: Foley, S. (2013) Battle is on to make bonds more transparent, Financial Times,

1 May.

Some corporate bonds are sufficiently liquid to trade on the London Stock Exchange and other exchanges in Europe, Asia or the Americas and may also be traded on electronic communication networks (ECNs), which facilitate trading outside stock exchanges, but the vast majority of trading occurs in the over-the-counter market directly between an investor and a bond dealer. Bond dealers stand ready to quote bid and offer prices depending on whether the investor wants to buy or sell. Fund managers, or brokers acting for investors, will have to contact a number of these dealers by telephone to get quote prices. The bid-offer spreads are generally higher than for equities - even large company bonds can have a spread of 15%, but most are less than this.

There have been attempts to shift a large volume of trading on to computerbased systems - see Article 4.3. These electronic trading venues allow investors to input their desired buy or sell offer prices and amounts. Such an offer may be fulfilled by the computer matching up with other clients (or the bank) on the other side of the trade (crossing trade). The competition, transparency and efficiency brought by the electronic systems will, it is hoped, reduce transaction costs. Many such platforms are now operating but they still account for only 1% of trades. Investors are irritated by the splitting of such trades between numerous venues, mostly run by an investment bank with its own agenda (singledealer systems) and would prefer to see one dominant platform (multi-dealer platform) emerge, run in a way that would benefit them. Concern has been expressed that platform providers are using data from the trading venue to inform their own team of traders and market makers - this knowledge might be used against investors. Market makers in the OTC market appear to be somewhat reluctant to shift from one-to-one trades with high spreads allowing them to pocket the difference between bid and offer prices to a computer system doing cheaper automatic trades - turkeys not voting for Christmas, I guess.