Article 4.3 Electronic trading to muscle in on corporate debt

By Michael Mackenzie, Dan McCrum and Tracy Alloway

Financial Times April 3, 2013

Computers rule on trading desks - except in the corporate bond market, one of the last bastions of telephone based transactions between investors and Wall Street dealers.

But that may be about to change.A recent surge in buying and selling of Dell's corporate bonds, triggered by the news of a leveraged buyout of the company, suggests electronic trading systems are set to muscle into this corner of the bond market.

While advocates of electronic trading are highlighting the shift in behaviour, some say the $9tn US corporate bond market is not designed for a seamless transition to computerised interactions, the way equities and foreign exchange trade.

‘Human judgment is what we're paid for in this business,' says Bonnie Baha, global credit portfolio manager for DoubleLine. With many small debt issues, prices on a screen for thinly traded securities would quickly become stale, she adds.

But for all the attachment to long standing and cosy relationships between sales staff at dealers and investors, changing conditions are leading the way to greater adoption of electronic trading.

Since the financial crisis, higher capital costs and regulatory scrutiny have forced Wall Street banks to sharply reduce their presence in the corporate bond market. With banks holding a smaller ‘inventory' of bonds, it is harder for so-called ‘buyside' investors to buy and sell large amounts of debt.

Coming forward to fill this gap are electronic trading platforms such as MarketAxess, Bonds.com, BondDesk, and TradingScreen. While attracting growing volumes, for the most part, trading on these platforms involves so-called ‘odd lots' or small trades of older bond issues.

At least, that was the case until trading activity in Dell bonds on several platforms surged earlier this year.

For one electronic platform, Bonds.com, the heightened activity in Dell bonds that helped its daily market share jump fivefold to around 10% was a watershed and points to a future solution. ‘It shows the model works, really well, or one like it could,' says Thomas Thees, chief executive at Bonds.com.He says the industry needs to reach a consensus around one trading venue. The dilemma for the industry is that an already fragmented bond market, comprised of thousands of individual bond issues, requires a common solution, not an ecosystem of competing electronic trading platforms. As a host of venues and initiatives by dealers are fighting for leadership, investors have yet to throw their weight behind one of them.

But at some point the investor community needs to take the lead. ‘The buyside has to be very engaged and involved with getting out in front of the liquidity issue, rather than sitting back and waiting for a solution,' says Chris Rice, global head of trading at State Street Global Advisors. ‘We need to take control of our destiny and start supporting emerging bond trading venues.'

Some dealers say efforts to build electronic corporate bond trading platforms have had to start slowly. Electronic trading can help banks reduce costs in their bond-trading businesses, by automating trades and eliminating expensive staff, but the trade-off is greater price transparency and potentially smaller profits per trade. Banks are reluctant to give up their profitable ‘high-touch' dealing in the bonds before they absolutely have to, some dealers say privately. Still, many banks have been experimenting with their own platforms, including Goldman Sachs, Morgan Stanley and UBS.

For many large bond investors, the use of single dealer platforms is limited, given that the dealer selects the bonds being transacted and can also gain an insight into what investors are doing.

FT

Source: Mackenzie, M., McCrum, D. and Alloway, T. (2013) Electronic trading to muscle in on corporate debt, Financial Times, 3 April.

Because most corporate bond market trading is a private matter between the dealer and its customer in the OTC market it is difficult to obtain prices of recent trades; they are not shown in the Financial Times, for example. Some websites provide prices and other details on a few dozen corporate bonds, for example www.fixedincomeinvestor.co.uk,www.hl.co.uk,www.selftrade.co.uk, http:// finra-markets.morningstar.com/BondCenter/Default.jsp.

Corporate bonds are generally the province of investing institutions, such as pension and insurance funds, with private investors tending not to hold them, mainly due to the large amounts of cash involved - the minimum denomination for bonds to be listed on a European stock market under EU Directives without a prospectus is ˆ100,000 (or its equivalent in another currency at time of issue). The par value on one bond, at, say, £100,000, ˆ100,000 or $100,000, is said to have minimum lot or piece. By keeping the denomination above these sizes, thus putting off retail investors, the issuer is exempt from the requirement for high levels of disclosure and ongoing financial reporting (e.g. exempt from yearly and half-yearly reports) because they are issuing to professional investing organisations.

Having said that the main bond market is a wholesale one, I need to add that there is another regulated market in London. In 2010 the London Stock Exchange (LSE, www.londonstockexchange.com) launched the Order Book for Retail Bonds (ORB), which offers retail investors the opportunity to trade a number of gilts, corporate bonds and international bonds, where lots are often £100 or £1,000, with a typical initial minimum investment of £2,000, and the costs of trading are relatively low.

Corporates are able to issue bonds on ORB in sizes smaller (from only £25 million) than on the wholesale markets, where issues are usually £250 million plus. Issuers must apply and be accepted by both (1) the United Kingdom Listing Authority (UKLA), part of the financial services industry regulator, the Financial Conduct Authority (FCA), and (2) the LSE.

Trading is facilitated by competing market makers advertising bid and offer prices on the LSE system during the trading day, 8am to 4.30pm. Retail investors can buy through a stockbroker, wealth manager or other regulated intermediary. Since 2010, companies on ORB have raised more than £4 billion with 42 new issues. Table 4.1 presents some of the issues, showing the amounts raised.Table 4.1 Some bonds available to retail investors on the London Stock Exchange's Order Book for Retail Bonds market

| Issuer | Market | Date Listed | Issue Size |

| Ladbrokes Group Finance plc | ORB | 17-Jun-14 | £100m |

| Paragon Group of Companies plc | ORB | 30-Jan-14 | £125m |

| Premier Oil plc | ORB | 11-Dec-13 | £150m |

| A2D Funding plc | ORB | 21-Oct-13 | £150m |

| Bruntwood Investments plc | ORB | 25-Jul-13 | £50m |

| Helical Bar plc | ORB | 25-Jun-13 | £80m |

| International Personal Finance plc | ORB | 08-May-13 | £101.5m |

| Provident Financial plc | ORB | 27-Mar-13 | £65m |

| Paragon Group of Companies plc | ORB | 05-Mar-13 | £60m |

| EnQuest plc | ORB | 15-Feb-13 | £155m |

| Alpha Plus Holdings plc | ORB | 19-Dec-12 | £48.5m |

| Unite Group plc | ORB | 12-Dec-12 | £90m |

| Tullett Prebon plc | ORB | 11-Dec-12 | £80m |

| St. Modwen Properties plc | ORB | 08-Nov-12 | £80m |

| London Stock Exchange Group plc | ORB | 05-Nov-12 | £300m |

| Workspace Group plc | ORB | 10-Oct-12 | £57.5m |

| Beazley plc | ORB | 25-Sep-12 | £75m |

| Intermediate Capital Group | ORB | 20-Sep-12 | £80m |

| CLS Holdings | ORB | 12-Sep-12 | £65m |

| ICAP | ORB | 31-Jul-12 | £125m |

| Primary Health Properties plc | ORB | 24-Jul-12 | £75m |

| Severn Trent plc | ORB | 11-Jul-12 | £75m |

| Tesco Personal Finance plc | ORB | 23-May-12 | £200m |

| HSBC | ORB | 02-May-12 | £196m |

| Provident Financial | ORB | 02-Apr-12 | £120m |

| Places for People | ORB | 31-Jan-12 | £40m |

| Intermediate Capital Group plc | ORB | 22-Dec-11 | £35m |

| Tesco Personal Finance plc | ORB | 16-Dec-11 | £60m |

| Royal Bank of Scotland | ORB | 07-Nov-11 | £20m |

| National Grid | ORB | 06-Oct-11 | £285.5m |

Figures 4.1 to 4.5 show the secondary bond price movements for some well- known companies.

Figure 4.1 Secondary bond price movements: Aviva

Source: Data from www.fixedincomeinvestor.co.uk

Figure 4.2 Secondary bond price movements: BP

Source: Data from www.fixedincomeinvestor.co.uk

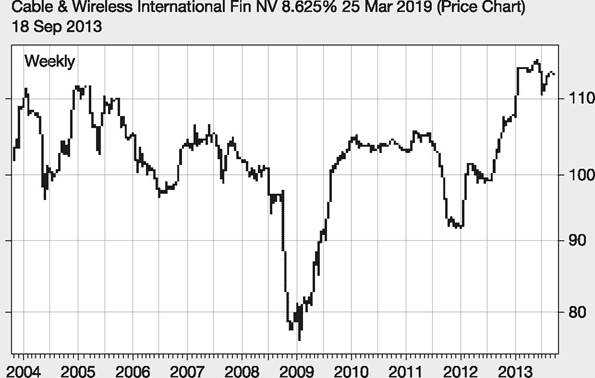

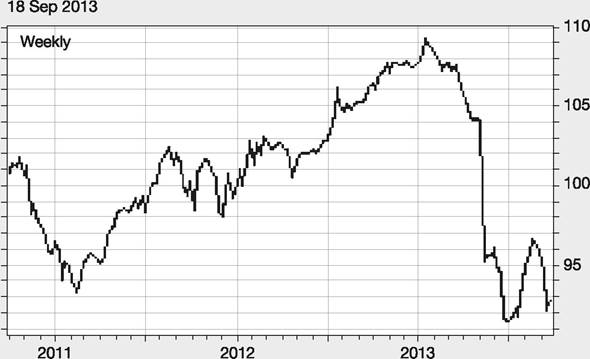

Figure 4.3 Secondary bond price movements: Cable & Wireless

Source: Data from www.fixedincomeinvestor.co.uk

Co-operative Bank 5.125% 20 Sep 2017 (Price Chart) 92.877 +0.11

Figure 4.4 Secondary bond price movements: Co-operative Bank

Source: Data from www.fixedincomeinvestor.co.uk

Figure 4.5 Secondary bond price movements: John Lewis

Source: Data from www.fixedincomeinvestor.co.uk

Case study

Tesco Bank (‘Personal Finance') bond

We now look at a bond issue on ORB in more detail: Tesco Bank's 8.5-year 5% Sterling Fixed Rate Bond issued in May 2012 and due to be redeemed at £100 on 21 November 2020.

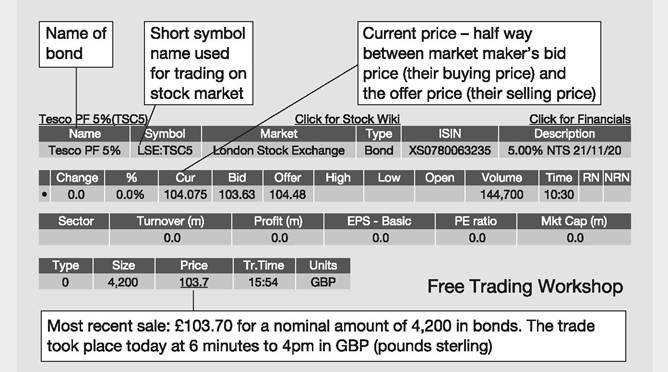

However, it may be redeemed (at 100% of face value), purchased or cancelled by Tesco Bank before then. This may happen if the tax rules change to make Tesco Bank pay more, or in the case of default. Interest is paid on 21 May and 21 November each year.When first issued the minimum purchase was a mere £2,000 and the issue price was 100% of the face value. Barclays Bank and Investec Bank both helped with the sale of the bonds in the primary market. They were book-runners (organisers of the issue) who received in fees 0.75% of the amount raised (0.75% of £200 million, i.e. £1.5 million), of which two-thirds was passed on to eight distributors, stockbrokers who sold the bonds to investors. Barclays Bank and Investec Bank subsequently acted as market makers in the secondary market. Many free financial websites display information about the bond and the trading prices in the secondary market - an example is shown in Figure 4.6, taken from www.ADVFN.com. Trades are settled after two business days (T+2).

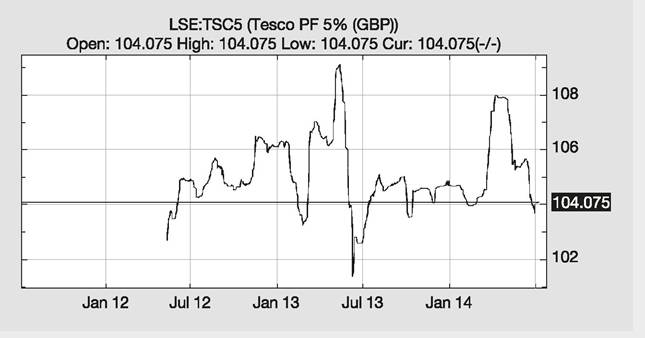

Figure 4.7 shows the price movements of Tesco Bank's bond during its first two years.

Figure 4.6 Trading details of Tesco Bank's bond on ADVFN

Source: advfn.com

Figure 4.7 Price chart of Tesco Bank 5% sterling 2020 bond

Source: advfn.com

Not all the bonds issued in ORB are borrowing with the same level of safety because they may not have the backup from the strongest part of a group of companies under the same ownership - see Article 4.4.