Article 5.5 ‘Dash for trash' lifts unrated debt sales

By Andrew Bolger and Robin Wigglesworth

Financial Times May 19, 2014

Now it is the turn of the tiddlers. Even companies too small to be graded by the leading rating agencies - or that choose not to - are benefiting from voracious investor appetite for European corporate bonds.

Mahle, a German car parts maker, SEA, an Italian airport operator, and Bureau Veritas, a France-based inspection and certifying company, are among those to have recently issued unrated bonds.

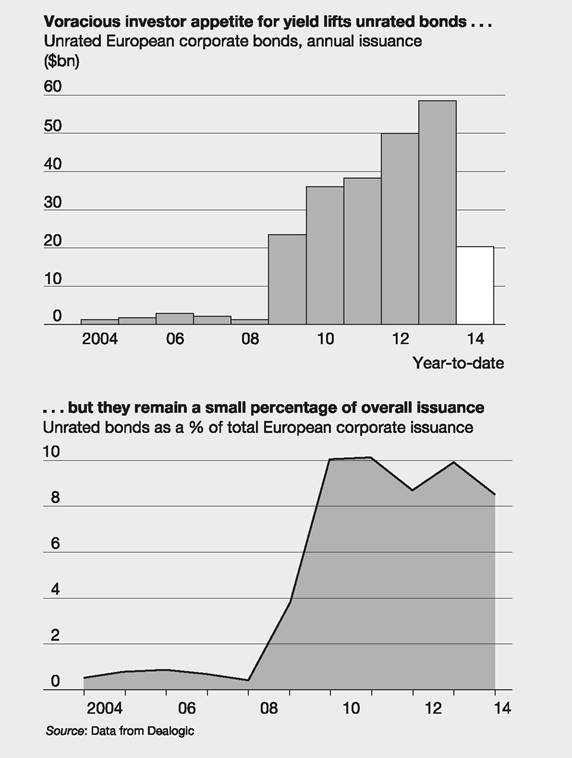

These bring the total volume of unrated corporate bonds issued in Europe this year to more than $20bn, and open up the prospect of yet another record year for grade-less company debt. Last year there were $58bn worth of unrated corporate bond sales.

Other prominent unrated deals so far this year include Sodexo, the French caterer, which borrowed $1.1bn in January, ProSiebenSat, the German broadcaster, which borrowed $828m in April, and CGG, an Irish support services group, which raised $750m in March.

However, unrated bond issues remain relatively rare, given many investors are limited to buying certain grades, and most prefer the transparency that a rating confers. They have accounted for about 10% of the European corporate bond market in recent years.

Unrated bonds also tend to be smaller and less liquid than rated debt. Half such bonds issued over the past three years were for less than $250m. The companies therefore have to pay lenders a premium to the yields at which they would normally expect to issue.

But Rupert Lewis, a debt syndicate banker at BNP Paribas, says that the extra cost of issuing unrated debt has come down over the last couple of years from approximately 100 basis points to 50bp - or potentially less, depending on the company.

‘It's a horses for courses market,' he says. ‘They tend to be companies that don't issue that often and therefore don't want to go through the workload and costs of getting and maintaining a credit rating for infrequent borrowing.

Without a rating they don't go in indices, so a large amount of investors cannot buy, but despite that the cost has definitely come down.'Jean-Marc Mercier, global head of debt syndicate at HSBC, says: ‘A lot of companies don't want to take on the cost, work and management time involved with obtaining a rating - particularly family-controlled companies.'

However, unrated bonds have also been issued by large companies such as SAP, the German software group, which has borrowed several billions of euros via such bonds. Household names that have used the market and subsequently acquired ratings include the Dutch brewer Heineken and Thomas Cook, the UK travel group.

The rating agency Fitch says some household names have been able to take advantage of their higher profiles among retail investors to issue unrated bonds. These include Skanska, the Swedish engineering group; Finnair in Finland; Air France-KLM; and Sixt, the German-based car rental group.

Mike Dunning at Fitch says: ‘UK companies can also access the US private placement market to raise funds on an unrated basis - which is easier than going through the full bond rating process.'

The agency says that a sizeable proportion of the larger issues of unrated bonds display credit profiles that could be classified as investment, or near-investment grade. This is in spite of a significant level of opportunistic issuance by smaller, non-eurozone domiciled corporates.

‘The European institutional bond market is generally receptive to the first, opportunistic, unrated bond from a new issuer, but increasingly looks for a rating if repeat visits, particularly for smaller issuers, are contemplated,' says Tom Chruszcz, an analyst with Fitch.

Source: Bolger, A. and Wigglesworth, R. (2014) ‘Dash for trash' lifts unrated debt sales, Financial Times, 19 May.

FT

A rating decision generally takes a few weeks and is made by a rating committee assessing the evidence, rather than by an individual.

The committee notifies the issuer of the rating and the rationale behind it.The agencies are also available to carry out credit analysis as a service to lenders. They thus produce unsolicited company analysis and credit ratings without necessarily gaining the cooperation of the issuing company (or country).

Post-rating

There is generally a high degree of ongoing interaction between a corporate and its CRA following bond issuance; the relationship is akin to that between a company and its longstanding bank, with a high degree of transparency. In addition to the agency gleaning information through dialogue with the company it will continue to scan publicly available sources. Its monitoring (ratings review) in the months and years following is focused on developments that could alter the original rating. Issues might arise that lead to an upgrade or a downgrade. These are called rating actions. A press release disseminates a change of rating.

The CRAs not only give countries/companies/bonds a credit rating, they also give an outlook, an assessment of what the credit rating is likely to be in the future over the intermediate to longer term: ‘positive ' indicates that the rating might be raised, ‘stable' means not likely to change, ‘negative' means it may be lowered, ‘developing' means it may be raised or lowered. This can be influenced by many things, such as political unrest (e.g. Egypt), natural disasters (e.g. earthquake in Japan and New Zealand) or economic instability (e.g. Ireland, Spain, Greece and Portugal in 2010-2012). But note, outlooks are not necessarily a precursor to ratings changes, just possibilities.

If a company announces or is expected to announce a major corporate move such as a proposed merger it might be placed on credit watch while events unfold. Sometimes the CRA assesses the rating it would give under different scenarios likely to stem from the event. This special surveillance can be short-term or long-term focused, unlike an outlook which has a more distant horizon.

Ranking

In the event of financial failure of a company (liquidation/bankruptcy), the ranking (‘priority') order for bonds is:

1 Senior secured debt holders will be paid first. An example of this would be a mortgage loan secured on the mortgaged asset.

2 Senior unsecured debt is paid next, if any money is left. This is debt consisting of loans which are not secured on an asset(s), but it is stated in the trust deed that they will be near the front of the queue for payouts of annual coupons and of proceeds from liquidation. After this group has been paid the subordinated bond holders may receive nothing.

3 Senior subordinated debt - high-yield or junk bonds, secured or unsecured.

4 Subordinated debt is the last type of debt to be paid out after all other creditors.

The situation becomes more complicated when group companies are forced into liquidation. For example, it is possible for senior debt issued by the holding company to be subordinated to debt issued by a subsidiary (senior or junior) if the subsidiary's lenders have legal access to assets of the subsidiary.

The variety of insolvency regimes across Europe, with different rules on bond priorities following insolvency, is thought to have inhibited bond market growth relative to that in the single system across the US - see Article 5.6.