Article 5.6 Europe looks for common default process

By Andrew Bolger

Financial Times August 11, 2014

European companies have been able to access a flood of high-yield loans and bonds over the past few years - so far with remarkably few defaults, thanks partly to low interest rates.

But rating agencies and lawyers warn that investors may not appreciate the complexity of the different European insolvency procedures they may have to deal with, when the market returns to more normal conditions.

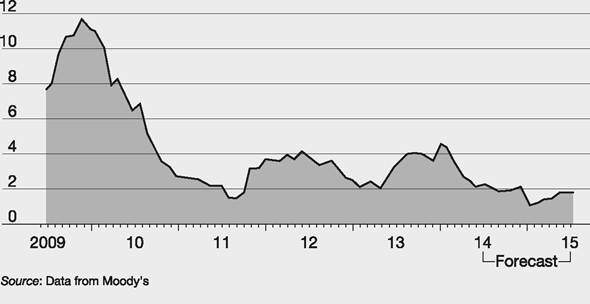

Moody’s says the default rate among high-yield issuers was 2.2% in the second quarter, down from 3.4% at the same stage last year. It expects the global high-yield default rate to finish this year at 2% - well below the historical average of 4.7% since 1983.

‘The benign default rate outlook is supported by robust liquidity which has continued for quite some time,’ says the rating agency. ‘Lowly rated companies have been able to access the capital markets and refinance their debt with issuer friendly terms, which will probably keep the default rates low into the first half of next year.’ However, no one expects the present benign conditions to last once interest rates start to increase.

Michael Dakin, a partner at the law firm Clifford Chance, likens the recent sell-off of high-yield bonds to ‘blowing the froth off the cappuccino'. But he predicts a ‘flood' of selling when the currently ‘ludicrously low' level of company defaults moves back closer to its historic average.

One potential problem is that US investors are used to dealing with corporate reorganisations conducted under the Chapter 11 procedure, which applies in all states, and is subject to the US bankruptcy code, providing for valuations of the debtor's assets and ranking of competing claims.

| Companies that defaulted in Europe over past year... Non-financial corporate defaults in EMEA | Defaulted amount ($m) | |||

| Company | Country | Industry | Date | |

| Songa | Norway | Energy | Dec 20 2013 | 6βo∣ |

| ATU | Germany | Retail | Dec 92013 | 620 |

| Invitel | Netherlands | bgcolor=white>TelecomJul 15 2013 | 457∣ | |

| Codere | Spain | Gaming | Sep 16 2013 | 300 |

| Cognor | Poland | Metals & mining | Nov 29 2013 | 164∣ |

| Travel port | US | Technology services | Mar 4 2014 | 135 |

| PagesJaunes | France | Media publishing | Apr 11 2014 | 28∣ |

| Schoeller Area | Netherlands | Packaging | Aug 22 2013 | 21 |

| Ideal Standard | Belgium | Consumer products | Mar 24 2014 | - |

| Total | 2385 | |||

...

but default rates are forecast to stay lowEurope spec grade default rates (%)

‘In Europe, there is no common process, law or statutory timetable equivalent to Chapter 11,’ says Philip Hertz, joint leader of the restructuring and insolvency group at Clifford Chance.

‘While high-yield products may have originated in the US, a European high-yield transaction, with a European issuer and a primarily European business, is a European deal in restructuring terms. If that deal falters, its restructuring will be largely driven by European considerations.’

But there are moves afoot to develop a more consistent regime across Europe. Continental European companies such as the German building materials group Monier, Italian directories publisher Seat Pagine Gialle and Spanish retailer Cortefiel, shifted jurisdiction to the UK to access more creditor-friendly, court-sanctioned schemes of arrangement, despite reforms in their own jurisdictions.

Many UK companies have used such schemes to restructure not only their liabilities governed by English law, but also non-English law liabilities.

FT

Source: Bolger, A. (2014) Europe looks for common default process, Financial Times,

11 August.

Bond ratings in the Financial Times

The Financial Times shows credit ratings daily in the tables titled ‘Bonds - Global Investment Grade' and ‘Bonds - High Yield & Emerging Market', together with yields to redemption (‘bid yield' - based on the bid price offered by market makers) and other details - see Tables 5.3 and 5.4. These give the reader some idea of current market conditions and the redemption yield demanded for bonds of different maturities, currencies and risk. The ratings shown are for August 2014 and will not necessarily be applicable in future weeks because the creditworthiness and the default risk of a specific debt issue can change significantly in a short period.

A key measure in the bond markets is the ‘spread', which is the number of basis points a bond is yielding above a benchmark rate, usually the government bond yield to maturity for that currency and period to redemption.Bond credit ratings are available direct from rating agency websites, www.standardandpoors.com,www.moodys.com, and www.fitchratings.com.

Note the higher variation in the price, yield and spread of the high-yield bonds, compared with investment-grade bonds.

| Aug 7 | Red date | Coupon | Ratings | Bid price | Bid yield | Day’s chge yield | Mth’s chge yield | Spread vs Govts | ||

| S* | M* | F* | ||||||||

| US $ | ||||||||||

| BNP Paribas | 06/15 | 4.80 | BBB+ | Baa2 | A | 103.28 | 0.98 | 0.03 | -1.13 | 0.89 |

| GE Capital | 01/16 | 5.00 | AA+ | A1 | 0 | 106.09 | 0.64 | -0.02 | -0.08 | 0.55 |

| Erste Euro Lux | 02/16 | 5.00 | A- | 0 | 0 | 104.24 | 2.11 | -0.03 | -0.17 | 1.65 |

| Credit Suisse USA | 03/16 | 5.38 | A | A1 | A | 107.24 | 0.89 | - | -0.05 | 0.28 |

| SPI E&G Aust | 09/16 | 5.75 | A- | A3 | A- | 107.50 | 2.07 | -0.04 | -0.08 | 1.63 |

| Abu Dhabi Nt En | 10/17 | 6.17 | A- | A3 | 0 | 113.54 | 1.79 | 0.01 | -0.05 | 0.73 |

| Swire Pacific | 04/18 | 6.25 | A- | A3 | A- | 114.04 | 2.26 | -0.07 | -0.06 | 1.38 |

| ASNA | 11/18 | 6.95 | A- | Baa2 | A | 119.10 | 2.19 | -0.06 | -0.18 | 0.58 |

| Codelco | 01/19 | 7.50 | AA- | A1 | A+ | 121.29 | 2.40 | -0.16 | -0.17 | 0.79 |

| Bell South | 10/31 | 6.88 | A- | WR | A | 123.05 | 4.88 | -0.04 | -0.17 | 2.45 |

| GE Capital | 01/39 | 6.88 | AA+ | A1 | 0 | 134.85 | 4.51 | -0.02 | bgcolor=white>-0.151.26 | |

| Goldman Sachs | 02/33 | 6.13 | A- | Baa 1 | A | 120.02 | 4.52 | -0.04 | -0.15 | 2.09 |

| Euro | ||||||||||

| JPMorgan Chase | 01/15 | 5.25 | A | A3 | A+ | 102.21 | 0.04 | -0.52 | -0.49 | 0.01 |

| Hutchison Fin 06 | 09/16 | 4.63 | A- | A3 | A- | 108.16 | 0.71 | -0.07 | -0.12 | 0.71 |

| Hypo Alpe Bk | 10/16 | 4.25 | 0 | Caa 1 | 0 | 92.01 | 8.33 | 0.02 | 2.01 | 8.32 |

| GE Cap Euro Fdg | 01/18 | 5.38 | AA+ | A1 | 0 | 116.03 | 0.64 | -0.04 | -0.09 | 0.60 |

| UniCredit | 01/20 | 4.38 | BBB | Baa2 | BBB+ | 113.61 | 1.74 | 0.01 | 0.05 | 1.43 |

| ENEL | 05/24 | 5.25 | BBB | Baa2 | BBB+ | 126.60 | 2.19 | -0.10 | -0.13 | 1.27 |

| Yen | ||||||||||

| Deutsche Bahn Fin | 12/14 | 1.65 | AA | Aa1 | AA | 100.21 | 0.95 | 0.01 | 0.18 | 0.92 |

| Nomura Sec S 3 | 03/18 | 2.28 | 0 | 0 | 0 | 104.49 | 1.00 | -0.04 | -0.05 | 0.92 |

| £ Sterling | ||||||||||

| Slough Estates | 09/15 | 6.25 | NR | 0 | A- | 104.82 | 1.90 | -0.02 | -0.07 | 1.11 |

| ASIF III | 12/18 | 5.00 | A+ | A2 | A+ | 110.20 | 2.48 | 0.00 | -0.17 | 0.79 |

US $ denominated bonds NY close; all other London close. S*- Standard & Poor’s, M*- Moody’s, F*- Fitch.

Source'. Thomson ReutersTable 5.4 High-yield and emerging market bonds, 7 August 2014

| Aug 7 | Red date | Coupon | Ratings | ||

| S* | M* | F* | |||

| High Yield US$ | |||||

| Bertin | 10/16 | 10.25 | BB | Ba3 | 0 |

| High Yield Euro | |||||

| Kazkommerts Int | 02/17 | 6.88 | B | Caa1 | B |

| Emerging US$ | |||||

| Bulgaria | 01/15 | 8.25 | BBB- | Baa2 | BBB- |

| Peru | 02/15 | 9.88 | BBB+ | A3 | BBB+ |

| Brazil | 03/15 | 7.88 | BBB- | Baa2 | BBB |

| Mexico | 09/16 | 11.38 | BBB+ | A3 | BBB+ |

| Philippines | 01/19 | 9.88 | BBB | Baa3 | BBB- |

| Brazil | 01/20 | 12.75 | BBB- | Baa2 | BBB |

| Colombia | 02/20 | 11.75 | BBB | Baa2 | BBB |

| Russia | 03/30 | 7.50 | BBB- | Baa 1 | BBB |

| Mexico | 08/31 | 8.30 | BBB+ | A3 | BBB+ |

| Indonesia | 02/37 | 6.63 | BB+ | Baa3 | BBB- |

| Emerging Euro | |||||

| Brazil | 02/15 | 7.38 | BBB- | Baa2 | BBB |

| Poland | 02/16 | 3.63 | bgcolor=white>A-A2 | A- | |

| Turkey | 03/16 | 5.00 | NR | Baa3 | BBB- |

| Mexico | 02/20 | 5.50 | BBB+ | A3 | BBB+ |

US $ denominated bonds NY close; all other London close.

S*- Standard & Poor’s, M*-Source,. Thomson Reuters

| Bid price | Bid yield | Day’s chge yield | Mth’s chge yield | Spread vs US |

| 113.06 | 3.85 | 0.03 | 0.14 | 3.26 |

| 100.75 | 6.52 | 0.17 | -0.38 | 6.52 |

| 102.75 | 1.72 | 0.68 | 0.39 | 1.68 |

| 104.31 | 0.92 | 0.00 | -0.37 | 0.87 |

| 103.78 | 1.20 | -0.03 | -0.10 | 1.16 |

| 121.25 | 1.12 | - | 0.27 | 0.66 |

| 131.48 | 2.34 | -0.05 | -0.04 | 0.72 |

| 148.20 | 3.05 | 0.17 | 0.12 | 1.41 |

| 143.64 | 3.11 | 0.03 | 0.06 | 1.51 |

| 111.50 | 4.98 | 0.25 | 0.72 | 3.35 |

| 147.38 | 4.33 | -0.03 | -0.13 | 1.91 |

| 112.88 | 5.61 | 0.19 | -0.15 | 2.37 |

| 103.05 | 0.95 | -0.25 | 0.06 | 0.92 |

| 104.73 | 0.40 | -0.01 | 0.11 | 0.40 |

| 105.50 | 1.39 | 0.04 | -0.11 | 1.38 |

| 120.85 | 1.53 | 0.02 | -0.04 | 1.14 |

- Moody’s, F* - Fitch.

5 CREDIT RATINGS FOR BONDS 167

Crisis of confidence

CRAs advance the argument that their ratings are mere opinions and are thus protected under free speech laws. They have no contract with the investing institutions, nor do they have a fiduciary duty to them, so say the agencies. Thus they can publish an opinion without being liable for mistakes or misleading statements.

But a lot of weight is placed on bond ratings by financial institutions and investors who rely on them for investment decisions. They can feel aggrieved if a bond rating fails to live up to expectations. It has been suggested that during the run-up to the financial crisis of 2008 the CRAs gave unduly high ratings to bonds that were shaky. Many have called into question the CRAs' judgement when it became apparent that many bonds rated ‘A' and above were, in fact, worthless. Just before Lehman Brothers went into bankruptcy, its credit rating was A, and Bear Stearns was downgraded from AA to A shortly before the company became insolvent. It would seem that the CRAs seriously underestimated the risks undertaken by these and many other companies. In particular, the CRAs have been criticised for not spotting the dangers in a number of bonds which gained their income from thousands of US mortgages, and several lawsuits were launched, with the CRAs being accused of causing financial loss through their perceived as inaccurate ratings.

There have been some serious legal challenges to the CRAs' claim that an ‘opinion' should not lead to claims of carelessness or negligence if their judgement turns out to be wrong. Article 5.7 shows the state of the law in Australia, which will probably have an impact on other jurisdictions: CRAs have a duty of care to investors, not just their paymasters, the issuers.