Article 3.3 Investors be warned: the bond market must turn some time

By John Authers

Financial Times February 27, 2015

Records were made to be broken. There were plenty of headlines for new equity highs this week, particularly the first new record close in 15 years for the UK's FTSE 100.

But a high after 15 years does not necessarily trigger much cause for alarm. Even if this is not an obvious time to buy UK stocks, it is hard to make the case that they are overblown.But then comes the bond market. Here, history suggests that prices have entered into new and undiscovered territory. But because that territory is so new, history has few precedents to help predict what might happen next.

This week's publication of the annual Barclays equity-gilt study demonstrated that UK gilts have outperformed stocks over the past 25 years - a remarkable outcome that implies that bonds' outperformance cannot be sustained. Over the longer term, as Neil Collins details elsewhere in these pages, equities have comfortably outperformed.

But by the standards of government bonds, UK gilts are not that impressive. Negative yields, meaning that investors are in effect paying the government for the privilege of looking after their money, are now available on bonds from Germany and Switzerland. This sounds crazy. Why would anyone do this?

In fact, negative yields can be explained by a number of factors. First, there is the fear of deflation. If you think the buying power of money will decline, it makes sense to buy a bond whose value will also decline.

Second, there is second-guessing the actions of central banks. If they will be buying at whatever price, then buy bonds, even at a negative yield, and sell to them later. The European Central Bank is about to launch into indefinite bond purchases, and the Bank of Japan is in the midst of a continuing bond-buying campaign. They can print money so they can be relied on to buy.

Third, there are demographics. As populations age, so it makes sense for more people to buy bonds that provide an income in retirement, and for more pension funds to buy them so that they can afford to make guarantees for the future. This is particularly true when governments change regulations to force them to do so, thereby arguably forcing them to lend cheap to the state.

Fourth, there is supply. There are fewer safe assets than there used to be. US mortgage-backed debt is, naturally, no longer considered to be in that category; the number of corporations with the top triple-A credit rating is also now negligible; and government bonds issued by peripheral eurozone countries are now regarded as very risky.

Hence, naturally enough, the few truly safe assets that are left become even more valuable - to the point where investors will even accept a negative yield.

Finally there is demand. Foreign exchange reserve managers have steadily bought bonds, particularly Treasuries, as insurance against crises. China's huge build-up of Treasury bonds, which arguably kept rates artificially low, was dubbed a ‘savings glut' as long as a decade ago. Now, the eurozone's huge and growing trade surplus should deepen that savings glut - and force bond yields down.

In the short term, it is eminently possible for bonds' price rise to continue, even though they have reached a historic extreme. The experience of last year, when substantially nobody was ready for bond yields to pivot downwards once again, makes that clear.

Richard Batley, economist at Lombard Street Research, points out that the money coming from the ECB and the Bank of Japan will be more than enough to counteract any decline in the balance sheet of the Federal Reserve, according to their announced plans.

But investors may have learnt the wrong lesson from 2014. Yes, bond yields can continue to fall, and even go negative. But that does not mean that they can never reverse.

Demographics have helped bonds (and equities) for the past three decades, and are in the process of reversing in the western world and even in China.

Once there are fewer savers as a proportion of the population, and more people gradually selling bonds as they live into their retirement, so this will be a big headwind for bond prices. And at some point, central banks will stop offering their support, even if that point is still in the future.And the pain when they do could be considerable. Investors have grown accustomed to low or even negative interest rates, and have developed a range of securities to act as a proxy for the safe income-producers that government bonds used to be. Look at the growth of real estate or infrastructure investing, for example, or the popularity of high-yielding dividend stocks.

All of these assets would be affected if and when the bond market finally turns.

And the steady exit of banks from fixed-income markets, under pressure from regulators, means that they would not be there to ease the process as bonds finally turn. There have been a few indicators in the past two years that the bond market is vulnerable to short and sharp turns - such as the ‘taper tantrum' in spring 2014, when yields rose, or last October's ‘flash crash', when they fell.

The chief warning of the Barclays study, even though history provides so few precedents, is that the bond market must turn at some point, and that when it does that turn could be violent.

Source: Authers, J. (2015) Investors be warned: the bond market must turn some time, Financial Times, 27 February.

2015

Japanese bonds

The Japanese Ministry of Finance issues Japanese government bonds (JGBs), paying interest semi-annually. In March 2014, the Japanese government had outstanding debt of ¥1,025 trillion ($10 trillion). Medium- and long-term bonds made up nearly 80% of this. Auctions take place regularly (usually monthly) according to a published calendar. Maturities on JGBs can be 2, 5, 10, 20, 30 or 40 years. Inflation-indexed JGBs are also issued for 10-year maturities and floating-rate JGBs for 15-year maturities.

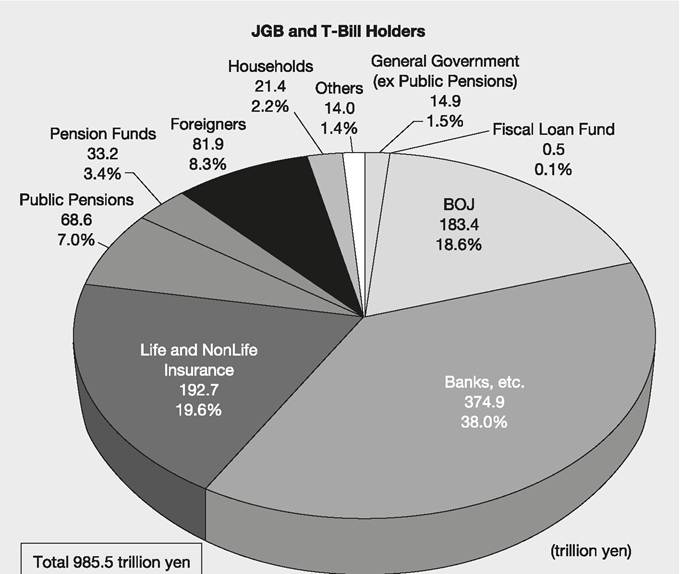

Japanese institutions purchase the majority (about 70%) of these bonds (see Figure 3.7), but retail investors are able to purchase 3-, 5- and 10-year bonds.

Figure 3.7 Breakdown of holders of Japanese government bonds and T-bills, December 2013 (BOJ is Bank of Japan, the central bank)

Source: Japanese Ministry of Finance www.mof.go.jp/english/jgbs/publication/newsletter/jgb2014_05e.pdf

The unit face values of JGBs are:

• ¥10,000 for JGBs for retail investors (3-year fixed rate, 5-year fixed rate, 10-year floating rate)

• ¥50,000 for 2-, 5-, 10-, 20-, 30- and 40-year

• ¥100,000 for 10-year inflation indexed, 15-year floating rate.

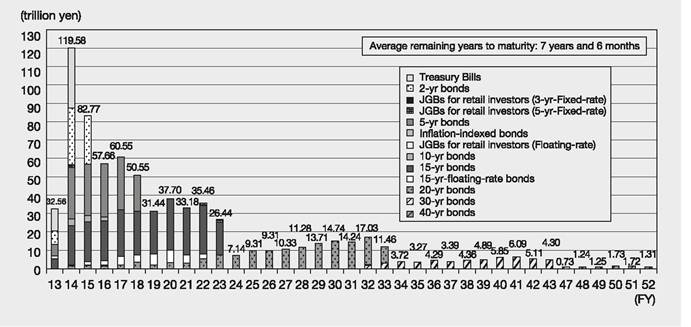

Many JGBs are traded in the over-the-counter secondary market, but trade has been severely constrained by the impact of the enormous quantity of buying by the central bank - see Article 3.4. Foreign investors are encouraged, but still hold less than 10%. A few are traded on the Tokyo Stock Exchange and other exchanges. The average time to maturity of bonds and T-bills combined is seven and a half years - see Figure 3.8.

Figure 3.8 Time-to-maturity structure of outstanding Japanese government bonds in

December 2013 - for redemption years stretching from 2013 to 2052

Source: Japanese Ministry of Finance www.mof.go.jp/english/jgbs/publication/newsletter/jgb2014_05e.pdf