Article 3.2 Why Uncle Sam needs some novel sweeteners for its bonds

By Gillian Tett

Financial Times January 31, 2014

This week the US government delivered two pieces of noteworthy news. One caused a splash: the Federal Reserve announced another $10bn cut in its monthly bond purchases, the second time it has tapered.

Cue Twitter alerts and headlines.But the real drama came a few hours earlier, when Uncle Sam successfully sold $15bn of two-year floating-rate notes to investors in the first innovation in federal debt for 16 years. The sale of these bonds that reset according to market rates - thus avoiding any losses if rates rise - attracted a startling $85bn of orders; not that you would have noticed from following the media, whether social or mainstream.

On one level this disparity is no surprise. Government bond auctions tend to be technical affairs. The Fed’s taper, by contrast, is replete with drama for global investors, particularly since it could trigger more volatility for emerging markets. But investors and taxpayers would be foolish to ignore the ‘floaters’. What they show is the degree to which Treasury officials are hunting for ways to ensure the US can keep selling its debt to global investors when interest rates rise. And the outcome of those discreet experiments could prove critical to whether that much-debated taper will play out smoothly - or not.

The issue at stake partly revolves around the manner in which the Treasury sells government debt. In the past this was done in a straightforward way: bonds carried fixed interest rates, and most of these were either short-term bills or 10-year ones. Until recently US officials saw little reason to change this approach as demand was sky high.

But now a business-as-usual course is starting to look dangerously complacent. Never mind the fact that the US debt pile has doubled to $17tn in the past decade; and ignore recent fiscal fights and the threat of a new debt-ceiling showdown.

The other challenge haunting the Treasury is the maturity profile of the debt.In the past three decades this maturity has averaged 58 months, meaning it must be renewed almost every five years. During the financial crisis it declined to four years - half the average maturity of most European countries. That produced one oft- ignored benefit: because the Fed has kept rates ultra-low, total interest costs have not risen as fast as total debt. Just like a homeowner on a floating mortgage, low rates have meant low monthly interest payments for the Treasury. Indeed, interest payments now represent 6% of federal outlays; two decades ago it was 15%.

But this benefit comes with a sting that mortgage borrowers know well: if rates increase, interest payments could balloon. And if investors panic about inflation, higher rates or fiscal sustainability, that squeeze could be more intense.

The good news is that the Treasury is aware of this danger, and trying to prepare. In recent months it has had success in raising the average maturity profile by selling more long-term bonds. This stands at 66.7 months, and officials say that by 2020 it could reach 80.

Treasury officials are also trying to help the market absorb future rate rises by offering a more flexible range of instruments. This week's experiment with floaters is one move. However, the Treasury is also selling inflation-protected bonds and officials are getting more proactive about asking large investors - including Asian buyers - what moves will keep them purchasing Treasuries. In March 2014 there were 32 bills being traded, 219 Notes, 64 Bonds, 38 TIPS and 321 STRIPS. Treasuries interest payments are exempt from local and state taxes, but not from federal income taxes.

FT

Source: Tett, G. (2014) Why Uncle Sam needs some novel sweeteners for its bonds, Financial Times, 31 January.

US STRIPS

Treasury STRIPS are similar to UK STRIPS, sold at a discount with maturities of 9 months to 30 years. US government notes and bonds may be converted to STRIPS by financial institutions and government securities brokers and dealers, who create STRIPS after purchasing the non-stripped notes or bonds.

They then ask the Federal Reserve (US central bank) to record the separation of coupons and face value with separate number identifiers on its computer system.

The individual coupons and principal can then be traded as zero coupon securities by dealers. The minimum face amount needed to strip a fixed-principal note or bond or a TIP is $100 and any par amount to be stripped above $100 must be in a multiple of $100. STRIPS may be reconstituted - this might be worthwhile if the package of zero coupon STRIPS is selling in the market at less than the complete Treasury security.Secondary market

US government bills, notes and bonds are traded in an active and liquid secondary market (in an over-the-counter market rather than on a formal exchange), with dealers posting bid (buying) and ask (selling) prices, and trades conducted over the telephone or by electronic communication. The central actors in the secondary market are the primary dealers (largest banks and brokerages in New York, Tokyo and London), which often act as market makers. Notes and bonds usually trade in $1,000 denominations. Settlement normally takes place one business day after a trade. Primary dealers also trade with each other directly or through interdealer brokers who match up buyers and sellers, usually with the advantage of anonymity for the participants. Retail investors buy or sell through banks and brokerage firms.

Prices for notes and bonds are quoted as a combination of whole dollars and as a fraction of a dollar. This may be in decimal terms, i.e. a fraction of 100, but more often the fraction used is 1∕32nd of a dollar. Thus a US Treasury bond price has two parts: (1) the handle, that is, the main number (the first), and (2) the 32nds, that is, the number expressed as a fraction of 32. This can be confusing because a decimal point might be used to separate the handle from the 32nds, despite the fact that the number that follows is not a fraction of 100 but of 32.

Table 3.3 shows the prices of US Treasury notes and bonds of varying maturities on 27 March 2014. The price for a $1,000 five-year note consists of (a) 99 and (b) 19¾ of 32.

(Thankfully our numbers are separated by a dash rather than a decimal point.) To convert into a percentage to determine the dollar amount for the bond we first divide 19¾ by 32. This equals 0.6171875. We then add that amount to 99 (the handle), which equals 99.6171875. So, 99-19¾ equals 99.6171875% of the par value. If the par is $1,000, then the price is $996.171875.Table 3.3 Prices of US Treasury notes and bonds, 27 March 2014

| Coupon | Price | Yield | |

| 2-year | 0.375 | 99-27½ | 0.45% |

| 5-year | 1.625 | 99-19¾ | 1.71% |

| 10-year | 2.75 | 100-14½ | 2.70% |

| 30-year | 3.625 | 101 -15½ | 3.54% |

Source: Data from Bloomberg.com www.bloomberg.com/markets/rates-bonds/government-bonds/us/

This price, which is slightly lower than the face value, demonstrates that the current interest rates (market yields) are higher than the coupon yield of 1.625%, $1.625 per $100. Often notes and bond prices are quoted just with a yield figure, as it is then possible to work out what the market price would be. (These calculations are explained in Chapter 13.) Some very active issues may be quoted in 64ths of a point - in this case a + sign is added to the 32nds. Some traders/writers use even more convoluted and confusing conventions and fractions. It is definitely a weird system, time honoured, but weird.

French bonds

The French Treasury, Agence France Tresor (AFT), is responsible for borrowing to finance the public debt - for 2013 this figure was ˆ169 billion. With this added to the total, France owed investors a sum equal to more than 90% of annual output.

Most of this was raised by selling medium- and long-term securities. AFT sells by auction on fixed dates government bonds with a face value of ˆ1 and a minimum bid of ˆ1 million. Any institution affiliated to Euroclear France[XII] and holding an account with the Banque de France (the central bank) is eligible to bid at the auctions, and they are able to sell the securities on to retail investors. Bids are made and the Treasury accepts the bids from the highest downwards until the target amount is achieved. Bidders pay varying prices according to their bids. The bonds issued are as follows:BTFs (bons du Tresor a taux fixe et a interets precomptes) are government bills with which the government covers its short-term cash position fluctuations. They have a maturity of one year or less and are auctioned every Monday.

BTANs (bons du Tresor a interets annuels) are auctioned on the third Thursday of each month and are two- to five-year bonds with a fixed annual rate of interest. Since the 1st of January 2013, new benchmark securities created on medium-term (maturities of two and five years) are issued under the form of OAT (Obligation Assimilable du Tresor), as it is the case for long-term securities (10 years and more). The specific name of BTAN for medium-term securities has indeed no more the utility it had originally. Existing BTAN continue to be tapped in order to maintain their liquidity.

OATs (obligations assimilables du Tresor) are auctioned on the first Thursday of each month and range in maturity from 7 to 50 years. They are mostly fixed rate, but some have floating rates, pegged to the TEC 10, an index of long-term government bond yields; these are called TEC 10 OATs (because the yield on a bond with close to ten years to redemption is used). There are some index- linked bonds, linked either to the domestic consumer price index, OATi, or to the eurozone price index, OATˆi. Once issued OATs may be supplemented by further issues. Interest is paid once per year.

OATs may be STRIPS.

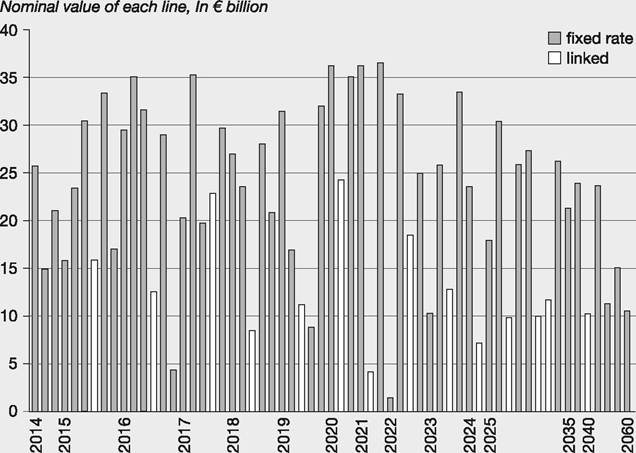

Figure 3.3 French government fixed-rate and index-linked bonds in issue by redemption year. Nominal amounts in ˆ billion in April 2014

Source: Agence France Tresor1 Monthly Bulletin, May 2014 www.aft.gouv.fr/documents/%7BC3BAF1F0-F068- 4305-821D-B8B2BF4F9AF6%7D∕publication∕attachments∕23525.pdf

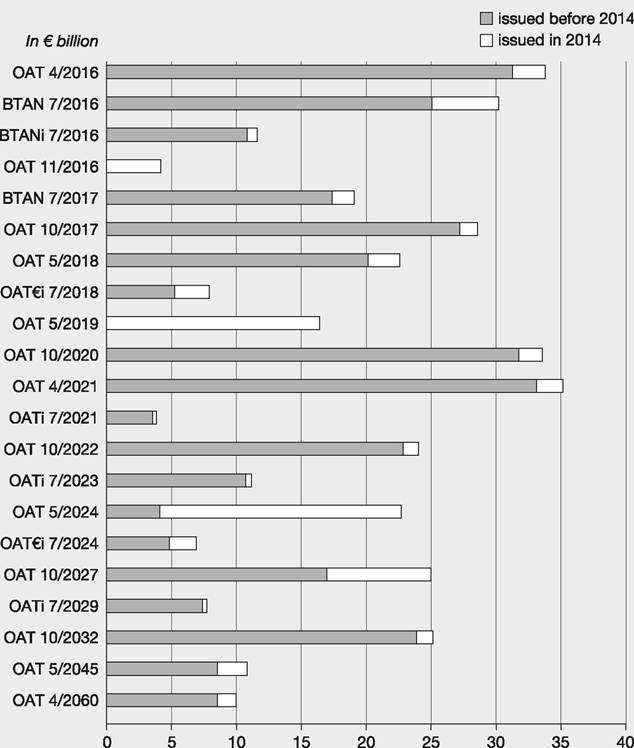

Figure 3.4 French government bond maturity dates. Securities issued during the first quarter of 2014 and total issuance

Source: Agence France Tresor1 Monthly Bulletin, May 2014 www.aft.gouv.fr/documents/%7BC3BAF1F0-F068- 4305-821D-B8B2BF4F9AF6%7D∕publication∕attachments∕23525.pdf

In 2014 the total of these bonds in issue was over ˆ1.4 trillion - see Figures 3.3 and 3.4. Primary dealers commit to market making in OATs in an OTC market.

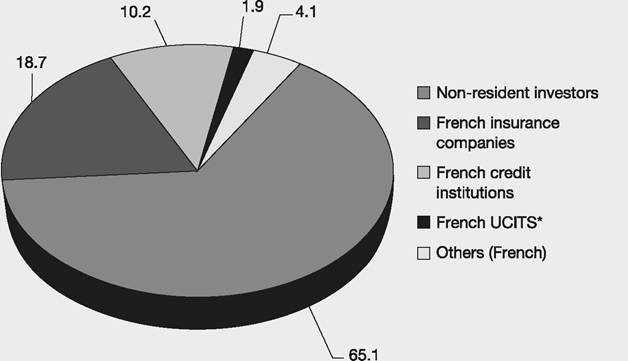

Note that the majority of French debt is held by non-residents - see Figure 3.5.

Structure in % expressed in market value

Figure 3.5 Holders of French government debt at the end of 2013

* Undertakings in Collective Investment in Transferable Securities

Source: Agence France Tresor1 Monthly Bulletin, May 2014 www.aft.gouv.fr/documents/%7BC3BAF1F0-F068- 4305-821D-B8B2BF4F9AF6%7D∕publication∕attachments∕23525.pdf

German bonds

In Germany, the German Finance Agency, Bundesrepublik Deutschland Finanzagentur (BDF), is tasked with managing German government debt. During 2014 it planned to issue securities totalling ˆ205 billion - see Table 3.4.

Table 3.4 German securities issues for 2014

| Security | Share 2014 | Volume 2014 ˆbn |

| Schaetze 2Y | 25.4% | 52 |

| Bobl 5Y | 23.4% | 48 |

| Bund 10Y | 26.3% | 54 |

| Bund 30Y | 3.4% | 7 |

| Capital market | 78.5% | 161 |

| Bubill 6M | 10.7% | 22 |

| Bubill 12M | 10.7% | 22 |

| Money market | 21.5% | 44 |

Source: Data from www.deutsche-finanzagentur.de

The BDF sells via pre-announced auctions arranged by the Bundesbank, the German central bank, with 6-month, 12 -month, 2-, 5-, 10- and 30-year maturities, with a nominal value of ˆ1 and a minimum bid of ˆ1 million. Only the 37 members of the Bietergruppe Bundesemissionen (Bund Issuance Auction Group) can place bids at the auctions. Bids may be competitive or noncompetitive. Competitive bids are made as a percentage of the nominal price and successful bidders pay the actual price bid, with bids being accepted from the highest downwards. Non-competitive bids are settled at the weighted average price of accepted bids. A detailed auction timetable is available from the BDF (www.deutsche-finanzagentur.de). The bills are discount securities and the bonds pay interest once per year.

Unverzinsliche Schatzanweisungen (Bubills) have maturities of 6 and 12 months. They are auctioned most months and generally account for less than 5% of German government securities outstanding in the secondary market.

Bundesschatzanweisungen (Schaetze) are two-year Federal Treasury notes. New Schaetze are issued four times a year, thus at any one time there are eight in issue. They made up about 11% of government debt in 2013.

Bundesobligationen (Bobls) are five-year Federal Notes. There are 3 new Bobl auctions per year and 15 series of Bobls are in issue. Bobls account for about 21% of German government securities outstanding in the secondary market.

Bundesanleihen (Bunds) are 10- and 30-year Federal bonds and form the majority of German government debt, around 60%. There are about 40 bunds in issue. In 2014 three new 10-year bunds were issued, each with a volume of ˆ18 billion. Three issues of 30-year bunds add up to ˆ7 billion. Some bunds may be stripped.

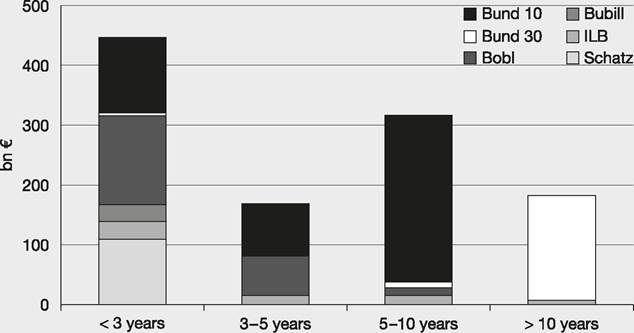

The total amount of German government securities outstanding was over ˆ1.1 trillion at the beginning of 2014 - see Figure 3.6, which shows the total value of bunds, etc., even if they have only a year or two left to redemption. There is considerable trading on the secondary market, at over five times the amount of securities in issue traded each year. The yield to maturity offered on German government bonds usually forms the reference or benchmark interest rate for other borrowings in the euro currency. In other words, it is the lowest rate available, with other interest rates described as so many basis points above, say, the ten-year bund rate.

Figure 3.6 The remaining time to maturity of German government securities, December 2013

Source: Bundesrepublik Deutschland Finanzagentur www.deutsche-finanzagentur.de/en/institutional/ secondary-market

During the darkest days of the eurozone financial crisis investors were so concerned about default risk that they were willing to pay very high prices for government bonds from those countries perceived to be safest. They did this to such an extent that the yield fell to below zero (the capital loss over the holding period outweighed the coupon income). Then with deflation came widespread holding of negative yield bonds - see Article 3.3.