Article 3.1 Foreign investors dump Treasuries at record pace

By Tracy Alloway and Vivianne Rodrigues

Financial Times August 15, 2013

Worries over the end of the Federal Reserve's bond-buying programme spurred foreign investors to sell US Treasuries at the fastest pace on record in June.

The Treasury showed that outflows of longer-term US securities, which include government debt as well as equities, reached $66.9bn in June. Foreign investors sold $40.8bn worth of Treasury bonds, the highest monthly sell-off on record.

June's sell-off in US securities coincided with a wider downturn in fixed income markets as investors fretted over the future of the US central bank's ‘quantitative easing' policy; deflating asset prices and roiling many big market participants.

The central bank could start to ‘taper' its unprecedented monetary stimulus later this year and end bond purchases in 2014, Ben Bernanke, Fed chairman, said in June. A decision to wind down the central bank's emergency economic policies would indicate that the US economy is recovering but could also spur more bouts of market volatility, analysts say.

After selling Treasuries in May, private foreign accounts based in the Caribbean, Belgium and Luxembourg - a proxy for hedge funds - bought back a combined $19bn of US government debt in June.

‘I wouldn't be surprised to see a big swing back in flows when July figures come out,' said Mr Miller [director of fixed-income strategy at GMP Securities]. ‘There's only so much large holders of Treasuries can sell, [as] they all need to keep exposure to the Treasury market, given its depth and liquidity.'

China remained the biggest investor of US government bonds but pared back its holdings by $21bn to $1.28tn between May and June. Japan, the second-biggest investor, cut its holdings by $20bn to $1.08tn.

Total outflows of $66.9bn surpassed the $59bn seen in November 2008, just after the collapse of Lehman Brothers which sparked the global financial crisis.

FT

Source: Alloway, T. and Rodrigues, V. (2013) Foreign investors dump Treasuries at record pace, Financial Times, 15 August.

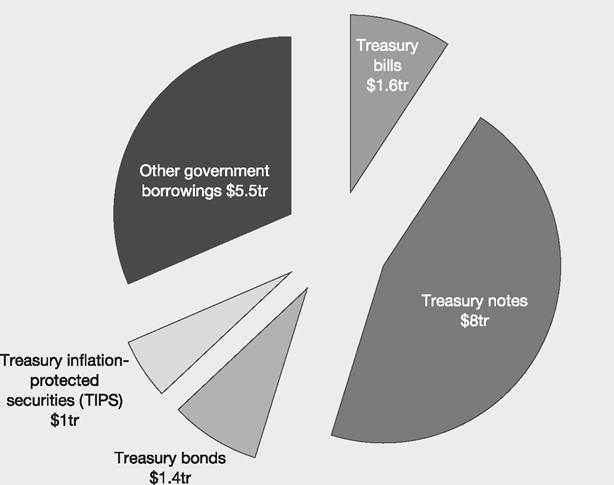

The US Public Debt stood at nearly $17.5 trillion in February 2014. But about $5 trillion of that was accounted for by one area of government owing another area of government money, thus the net amount (owing external investors) was around $12.5 trillion. Nearly $12 trillion of Treasury-issued marketable securities are held by outside investors, including notes, bills, bonds and TIPS (explained on page 67) - see Figure 3.2. Most of the rest is owned by government-managed trust funds and savings bonds.

Figure 3.2 US government public debt, February 2014

US Treasury securities are initially sold at government-run auctions; the auction bids are based on the yield amount and every bidder pays the same price, which is set by the auction. The securities are issued electronically, although some older ones exist in paper form. At the auctions, only banks, brokers or dealers may make competitive bids, up to a maximum of 35% of the total amount on offer, and they are allocated some, or all, of the requested amount. Individuals may participate in the auctions through TreasuryDirect or through a broker (or bank), up to a maximum of $5 million, and they are guaranteed to receive the amount requested, but they will pay the price that is the outcome of the competitive bid auction. At the close of the auction all non-competitive bids are accepted, followed by competitive bids starting with the lowest yield, until the amount of bids accepted reaches the sum the government wishes to raise at that particular auction, and that yield becomes the accepted bid.

Treasury bills (T-bills) range in maturity from 1 day to 52 weeks, with 4-week (28 days), 13-week (91 days) and 26-week (182 days) bills being the most common. They are sold at a discount to par value by auction every week, except for the 52-week bills which are auctioned every 4 weeks.

They are zero coupon securities, i.e. they do not pay a dividend; any gain for an investor results from the difference between the purchase price and the selling price.Treasury notes have a coupon payable every six months. They have a maturity of two, three, five, seven or ten years and are sold at roughly monthly intervals. Notes are sold in increments of $100. The minimum purchase is $100.

Treasury bonds are auctioned every few months, have maturities greater than 10 years (usually 30 years) and pay interest twice per year. Bonds are sold in increments of $100. The minimum purchase is $100. Notes and bonds are referred to collectively as Treasury coupon securities.

Treasury inflation-protected securities (TIPS) are index-linked bonds whose principal value is adjusted according to changes in the Consumer Price Index (CPI). They have maturities of 5, 10 or 30 years and interest is paid twice yearly at a fixed rate on the inflation-adjusted amount. TIPS are sold in increments of $100. The minimum purchase is $100. If an investor buys in the primary market $100,000 of TIPS offering a 2% annual coupon (1% per six months) with 10 years to maturity, and inflation in the first six months is 1.5%, the principal amount rises to $101,500. The first semi-annual coupon will be 1% of the new principal amount, i.e. $1,015. The upward adjustment of principal amount for inflation occurs before each of the subsequent coupon payments, thus raising the coupon by the CPI. At maturity the investor will receive the final principal amount including adjustment for ten years of inflation. To protect against deflation the holder receives at maturity the adjusted principal or the original principal, whichever is greater.

Treasury floating-rate notes (FRNs) were introduced in January 2014. Auctions of FRNs take place each month, with original issues in January, April, July and October, and reopenings in the other months, that is, the auction of additional amounts of a previously issued security. They pay quarterly a rate of interest that varies according to the rates on 13-week T-bills (a slightly higher rate is given - ‘spread over bills'). FRNs are sold in increments of $100. The minimum purchase is $100. Article 3.2 explains that the US Treasury has chosen to introduce FRNs as a way of attracting lenders worried that interest rates might rise unexpectedly over the life of the bond (a fixed-rate bond would then fall in price, but with the coupons rising on the FRN, it may maintain its price).