Article 3.8 Markets: the road to redemption

By Robin Wigglesworth

Financial Times January 31, 2013

Developing nations have largely tackled their poor exchange rates, high inflation, crushing debt burdens, trade imbalances and budget deficits that helped sink them in the 1980s and 1990s.

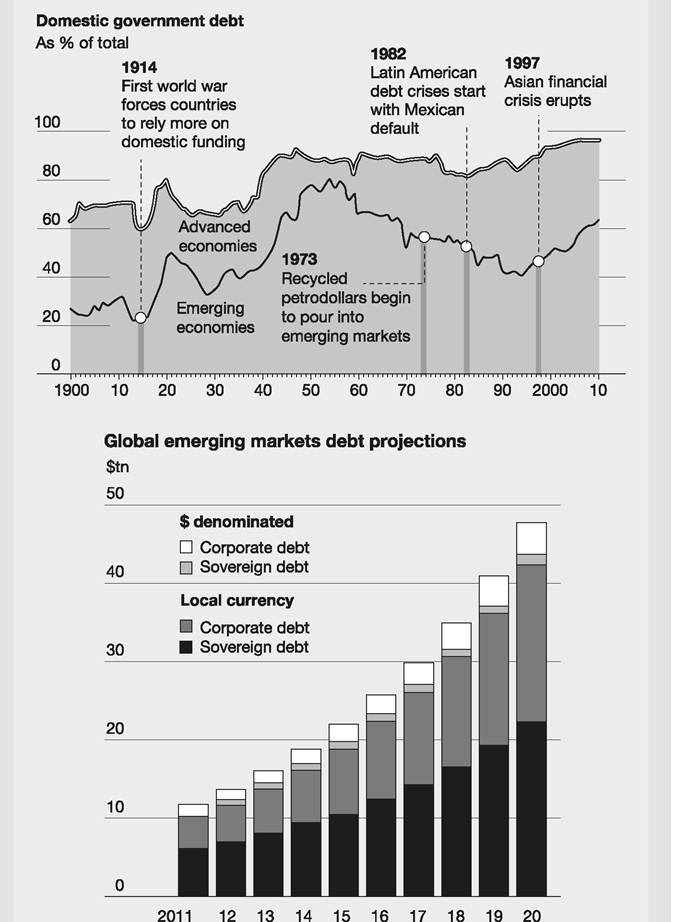

One of the most remarkable shifts is the rapid growth of their domestic bond markets. Over the past decade they grew fivefold to about $10tn by late 2011, according to the latest comprehensive data, which is estimated to equal almost one-sixth of the world's total bond stock.

This is a revolutionary development. Throughout modern economic history, most countries that have needed long-term loans have been forced to borrow abroad in one of the world's major currencies, predominantly the US dollar. Although many have had banking sectors or even local bond markets to tap, the domestic lending capacity has often been limited, and the duration of the loans has been exceedingly short.

More than a decade ago, the economists Barry Eichengreen and Ricardo Hausmann named the emerging markets' inability to borrow abroad in their local currency as ‘original sin'. Professor Hausmann: ‘It seemed to be a huge, persistent problem that all emerging markets were born with, and had remarkable problems getting rid of'.

Original sin is pernicious. Borrowing in foreign currencies can both trigger and exacerbate financial and economic crises. When a country's debts are denominated in foreign currencies, it forces policy makers to keep exchange rates pegged or heavily managed. If the rate buckles, the authorities have to burn through valuable reserves and raise interest rates to protect the value of the local currency - even in the midst of a recession if necessary.

Almost inevitably, the peg breaks, the local currency tumbles, the foreign currency- denominated debt burden becomes too great and a destructive government default ensues.

Spurred by these crises, emerging market policy makers have spent the past decade getting their finances in order. Crucially, they have nurtured and developed domestic bond markets denominated in local currencies.

‘We saw with our own eyes how hard [the Asian financial crisis in 1998] hit our neighbours, and how harshly the IMF treated them - far worse than it is treating the eurozone,' Cesar Purisima, the Philippine finance minister, told the Financial Times. ‘We learnt lessons from that.'

The changes across emerging markets are eye-catching. The domestic Mexican peso bond market, for example, exploded from about $28bn in US dollar terms in 1996 to $445bn in late 2011. South Korea's bond market surged fivefold to $1.1tn over the same period, while Poland's zloty market grew sevenfold to $203bn.

It has been a gradual process. Local institutional investor bases have often had to be started from scratch through reforms that encourage domestic pension and insurance industries to take root. Above all, inflation - the nemesis of bond investors but a perennial problem in emerging markets - had to be tamed.

‘When I started trading, emerging markets were the wild west,' recalls Sergio Trigo Paz, head of emerging market debt at BlackRock. ‘Local markets were considered no-man's land, even domestically, due to hyperinflation.'

Kenneth Rogoff and Carmen Reinhart have shown that the share of domestic debt to total government debts in emerging markets declined gradually from a peak of about 80% in the 1950s to a low of about 40% in the early 1990s. But by 2010 the percentage had climbed sharply back to more than 60%. In fact, experts now say domestic debt levels could return to those highs of the 1950s.

‘There were very large local bond markets before, but high inflation pretty much wiped them out,' says Mr Rogoff, an economics professor at Harvard. ‘Things are changing. Developing countries have been very keen to rebalance their borrowing away from foreign markets.'

The financial crisis reinforced this trend.

Domestic bond sales now account for the vast majority of government borrowing in the developing world, perhaps as much as 90% of it in 2012.International investors have become increasingly infatuated by the economic prospects for the developing world and have piled into local bond markets in recent years. From less than $150bn in March 2009, foreign holdings of local currency emerging market bonds climbed to well over $500bn last year.

The rating agencies have also cheered the rise of local bond markets and have rewarded developing countries with better grades. ‘One of the key reasons for the improvement in emerging market resilience and robustness - and the increase in their ratings - is the changing make-up of their debt,' says David Riley, head of sovereign ratings at Fitch Ratings.

Although positive, more vibrant local bond markets do not completely inoculate countries from crises. Deep local markets can even act as a temptation for governments to borrow excessively. Once they do, many countries have in the past found it easier simply to inflate the debts away - throttling local bond markets in the process. Some have simply defaulted. For example, Russia's short-term debt market allowed it to delay its inevitable default in 1998, but exacerbated the ensuing chaos. Local bond markets are also of little help if a country has a current account deficit. Countries that import more than they export need foreign currency inflows to make up the difference, whether through borrowing or overseas investment. Even governments with healthy budget surpluses can run into trouble if the current account is negative.

It also remains tricky to sell longer-term bonds locally. While some have managed to lengthen the ‘duration' of their markets, even some of the more advanced emerging economies struggle to sell bonds with a maturity longer than 10 years.

‘Original sin is receding for some countries, but mostly for the advanced ones,' says Marie Cavanaugh, managing director and member of the sovereign ratings committee at Standard & Poor's.

‘Poorer, less developed emerging economies are often still very dependent on foreign capital.'Of the almost $10tn worth of locally denominated debts tallied by BofA, almost two-thirds are in Brazil, China and South Korea. Many smaller countries have found it harder to nurture local markets.

In fact, the IMF has started to become concerned that the current eagerness of investors to lend to emerging economies could lead some of these smaller states to forget the hard-learnt lessons of the past and borrow too much in dollars.

Countries such as Zambia and Mongolia have been identified as being at particular risk of reviving the bane of original sin. Mongolia late last year sold a $1.5bn bond - equal to a fifth of its annual economic output in a single offering.

Some fund managers also fret that emerging market companies could become future sources of instability, after selling record amounts of dollar-denominated corporate bonds in recent years.

Professors Hausmann and Eichengreen agree that original sin is a less pressing problem than in the past, but argue that improvements are the result of a drastic curtailment of dollar borrowing - not a rise in international investor participation on local bond markets. Indeed, these days some countries have imposed barriers to keep foreign investors out of their markets, rather than enticing them in. Capital inflows can cause currencies to appreciate, making a country less competitive. Foreign investors are often more fickle than local ones, and sharp outflows can unsettle local markets.

Sources: Datafrom C Reinhart and K Rogoff, ‘The Forgotten History of Domestic Debt,’ NBER, 2010; Ashmore Group.

Nonetheless, the rise of domestic bond markets has proved a tremendously positive development not just for emerging economies but also for the wider international financial system. Rather than being sources of instability - as was often the case in the past - many emerging markets are now self-funding carthorses for the global economy.

The progress of the past decade is already striking. As long as policy makers do not forget the lessons of past crises, local bond markets are likely to continue to gain in size, vibrancy and importance, experts say.

FT

Source: Wigglesworth, R. (2013) Markets: the road to redemption, Financial Times, 31 January.

Africa has underdeveloped local bond markets, but even here many of its countries are now welcomed in the international dollar-denominated market - see Article 3.9.