Article 5.9 Scope Ratings aims to shake up hegemony

By Patrick Jenkins

Financial Times April 15, 2013

A new pan-European rating agency is expanding from modest German roots with an ambition to challenge established names such as Standard & Poor’s and Moody’s.

Scope Ratings, a family-owned company based in Berlin, will on Tuesday open a London office, with a focus on banks.The London operation will be headed by Sam Theodore, formerly head of European bank ratings at Moody’s and more recently a regulator first with the UK’s Financial Services Authority and latterly with the European Banking Authority.

The move comes in the same week that another German ratings initiative, by a non-profit arm of the Bertelsmann media group, got under way. On Monday, the Financial Times reported that the Bertelsmann Foundation’s International Non-profit Credit Rating Agency (Incra) had initiated its coverage of US government debt with a AA+ rating.

The established Big Three of the ratings world have been widely criticised for failing to spot the warning signs that led to the financial crisis and for being slow in reforming their methodologies to reflect the post-crisis world.

Scope believes its fresh start in rating the banking industry will allow it to take a less formulaic approach. Mr Theodore and his team will incorporate more qualitative analysis of business models and relations with regulators alongside regulator-style stress-testing of loan portfolios and capital strength.

The agency has no plans to move into sovereign ratings and sees its pan-European role as sharply focused on banks for the time being. It has ambitions to rate 50 to 60 mostly large European lenders over the next 18 months.

A third German ratings initiative - from the consultancy Roland Berger - remains in the planning stage, though company insiders said the project was progressing.

FT

Source: Jenkins, P.

(2013) Scope Ratings aims to shake up hegemony, Financial Times,15 April.

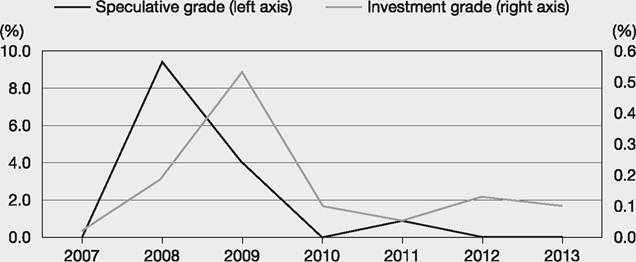

Bond default rates

Table 5.5 and Figure 5.1 show research from Fitch, detailing the proportion of corporate finance bonds that have defaulted one, two, three, four, five and ten years after issue over the period 1990-2013. Notice the large differences in

Table 5.5 Global corporate finance defaults 1990-2013

| Rating | 1-year | 2-year | 3-year | 4-year | 5-year | 10-year |

| AAA | 0 | 0 | 0 | 0 | 0 | 0 |

| AA+ | 0 | 0 | 0 | 0 | 0 | 0 |

| AA | 0 | 0 | 0.11 | 0.28 | 0.46 | 0.36 |

| AA- | 0.06 | 0.06 | 0.06 | 0.07 | 0.07 | 0.21 |

| A+ | 0 | 0.1 | 0.2 | 0.27 | 0.4 | 0.89 |

| A | 0.06 | 0.25 | 0.45 | 0.69 | 0.94 | 2.05 |

| A- | 0.17 | 0.31 | 0.46 | 0.57 | 0.74 | 2.53 |

| BBB+ | 0.13 | 0.28 | 0.51 | 0.82 | 1.16 | 2.39 |

| BBB | 0.09 | 0.64 | 1.29 | 1.97 | 2.58 | 4.79 |

| BBB- | 0.39 | 1.14 | 1.89 | 2.66 | 3.6 | 7.54 |

| BB+ | 0.92 | 2.62 | 4.17 | 5.71 | 7.13 | 10.15 |

| BB | 0.79 | 2.84 | 4.55 | 6.36 | 7.69 | 13.78 |

| BB- | 1.59 | 2.6 | 4.08 | 5.08 | 6.01 | 9.19 |

| B+ | 1.01 | 3.65 | 6.08 | 7.83 | 9.04 | 10.12 |

| B | 2.28 | 5.11 | 8.2 | 11.52 | 14.24 | 13.97 |

| B- | 2.63 | 4.92 | 6.16 | 7.42 | 9.19 | 10.19 |

| CCC to C | 23.51 | 31.48 | 34.96 | 37.01 | 39.58 | 39.54 |

| Investment grade | 0.11 | 0.35 | 0.61 | 0.88 | 1.17 | 2.27 |

| Speculative grade | 2.88 | 5.33 | 7.38 | 9.16 | 10.7 | 13.38 |

| All corporate finance | 0.73 | 1.43 | 2.04 | 2.59 | 3.07 | 4.07 |

Source: Data from Fitch - Credit Market Research Report

www.fitchratings.com/web_content/nrsro/nav/NRSRO_Exhibit-1.pdf

Figure 5.1 Global corporate finance issuer default rates

Source: Data from Fitch - Credit Market Research Report www.fitchratings.com/web_content/nrsro/nav/ NRSRO_Exhibit-1.pdf

default rates between the ratings. After five years only 0.46% of AA bonds had defaulted, whereas 14.24% of B bonds had defaulted.

When examining data on default rates it is important to appreciate that default is a wide-ranging term and could refer to any number of events, from a missed payment to liquidation. For some of these events all is lost from the investor's perspective. For other events a very high percentage, if not all, of the interest and principal is recovered. Hickman (1958)[XIV] observed that defaulted publicly held and traded bonds tended to sell for about 40 cents on the dollar. This average recovery rate rule of thumb seems to have held over time - in approximate terms - with senior secured bank loans returning roughly 60% and subordinated bonds less than 30%. But the average disguises a wide variety, with many defaulted bonds offering nothing and others giving a recovery of 80% or more.