Article 7.3 Sub-Saharan market: high yields fire appetite for African Eurobonds

By Fiona Rintoul

Financial Times November 3, 2013

Investors have flocked to Eurobonds as an attractive alternative to bonds issued in local currencies such as Nigeria's naira.

In October 2007, Ghana became the first sub-Saharan African country outside South Africa for 30 years to issue a dollar-denominated bond. Its $750m Eurobond, which had an 8.5% coupon rate, was four times oversubscribed and signalled a flurry of successful African Eurobond issues.

Countries such as Gabon, Ivory Coast, Namibia, Nigeria, Senegal, Rwanda and Zambia have all since issued sovereign bonds. Corporate issues have taken place in Nigeria and Ghana, and there has been a government-backed agency issue in Mozambique.

African Eurobonds offer high yields and a way into the African story for fixed- income investors wary of the currency and liquidity risks associated with even higher-yielding local currency bonds.

Antoon de Klerk, portfolio manager for emerging markets fixed income at Investec Asset Management, cites the example of Rwanda, which issued a $400m Eurobond in May with a 6.625% coupon that was nearly nine times oversubscribed.

‘Unless you believe Rwandan fundamentals have changed since then, it remains a good investment opportunity,' he says.

Of course, changes to US monetary policy affected the investment. But Mr de Klerk believes the scenario is not as dire as it is sometimes depicted.

‘Something people miss a lot is the yield protection, which means you run relatively low interest-rate risk,' he says. ‘The yield movements in the US and Rwanda were similar during the sell-off, but after the sell-off the US still only yielded 2.8%, while Rwanda yielded 8.7%.'

According to Vimal Parmar at Burbidge Capital, it is now likely to take place this December or early next year. On the basis of other African Eurobond issues, investors may ask for a higher yield than was expected when the issue was planned.

Ghana certainly paid a premium to investors on its second Eurobond issue in July, but Zambia's 15 times-oversubscribed issue in October shows investor appetite for African Eurobonds is still keen.There have been judders: the Seychelles and Ivory Coast have defaulted on Eurobonds. On the other hand, Eurobonds attract new investors. ‘Anything that diversifies funding sources from traditional concessional loans, which haven't got Africa that far, is definitely good,' says Stephen Charangwa, fixed-income portfolio manager at Silk Invest.

In the meantime, Angola, Cameroon, Tanzania and Uganda also plan debut Eurobond issues, as does Ethiopia when it has secured a credit rating.

FT

Source: Rintoul, F. (2013) Sub-Saharan market: high yields fire appetite for African Eurobonds, Financial Times, 3 November.

© Andrew Macdowall.

Eurobonds are distinct from euro bonds - euro bonds are bonds denominated in euros and issued in the eurozone countries. Of course, there have been euro-denominated Eurobonds issued outside the jurisdiction of the authorities in the euro area; these are euro-Eurobonds.

Eurobonds can be described as ‘external bonds', but the more precise definition of ‘bonds sold outside the jurisdiction of the country of the currency in which the bond is denominated' is more descriptive. So, for example, the UK financial regulators have little influence over Eurobonds issued in Luxembourg and denominated in sterling (known as Eurosterling bonds), even though the transactions (for example interest and capital payments) are in sterling.

Eurobonds are medium- to long-term instruments with standard maturities of three, five, seven and ten years, but there are also long maturities of 15-30 years driven by pension fund and insurance fund demand for long-dated assets. Because they are issued outside the country of the currency of issue, they are not subject to the rules and regulations imposed on foreign bonds. One such requirement for foreign bonds is to issue a detailed prospectus, which can be expensive.

More importantly Eurobonds are not subject to an interest-withholding tax. In many countries the majority of domestic and foreign bonds are subject to a withholding tax by which income tax is deducted before the investor receives interest. The fact that Eurobond interest is paid gross without any tax deducted has appeal for investors keen on delaying, avoiding or evading tax. The EU and the US would like to introduce regulations and minimise tax evasion. But theUK, the world centre for Eurobonds, is sticking to its tax exemption, making it difficult for other jurisdictions to tax this source of income - this stateless money will flow to where it is most advantageous to lenders and borrowers, thus any tax rules in one or a few countries only will be bypassed.

Eurobonds are also bearer bonds, so holders do not have to disclose their identity. All that is required to receive interest and capital is for the holder to have possession of the bond. Originally this meant physically held bonds, but today many bearer bonds are held in a central depository so that trading and post-trade settlement can take place electronically - a paperless system. The clearing organisations (e.g. Euroclear or Clearstream) ‘present' the bonds for coupon payment on the appropriate dates. The anonymity from the government authorities makes tax avoidance even easier. In contrast, domestic bonds are usually registered, allowing companies and governments to identify the owners and ensure that taxes are paid.

Despite the absence of official regulation, the International Capital Market Association (ICMA), a self-regulatory body based in Zurich, imposes some restrictions, rules and standardised procedures on Eurobond issue and trading. Securities dealers from dozens of countries accept rules on issues such as standardised methods of calculating bond yields, procedures for settling secondary market transactions and computerised mechanisms for reporting trades in the market.

The development of the Eurobond market

In the 1960s many countries (e.g.

the USSR), companies and individuals held surplus dollars outside the US and were reluctant to hold these funds in American banks where they would be subject to US jurisdiction. Also rigorous US tax laws were offputting, as was the tough regulatory environment in the US domestic financial markets, making it more expensive for foreign institutions to borrow dollars in the US. These factors encouraged investors and borrowers alike to undertake transactions in dollars outside the US. London's strength as a financial centre, the UK authorities' more relaxed attitude to business and its position in the global time zones made it a natural leader in the Euro markets.The market grew modestly through the 1970s and then at a rapid rate in the 1980s. By then the Eurodollar bonds had been joined by bonds denominated in a wide variety of currencies. The market was stimulated not only by the tax

and anonymity benefits, which brought a lower cost of finance than for domestic and foreign bonds, but also by the increasing demand from transnational companies and governments needing large sums in alternative currencies and with the potential for innovatory characteristics. The Eurobond market was further boosted by the recycling of dollars from the oil-exporting countries, which generated vast amounts of dollars needing an investment home, and by other countries not wanting to keep dollar assets in the US, e.g. Iran, and by American companies choosing not to send profits to head office because of the high tax rates if they did so. Apple, for example, had more than $150 billion held outside of the US in 2014, while eBay said it faced a tax charge of $3 billion on $9 billion of foreign earnings it was bringing back to the US that it had been storing offshore.

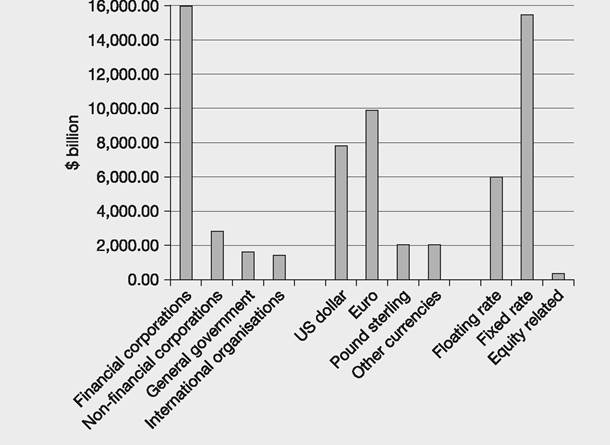

In 1979 less than $20 billion worth of international bonds were issued in a variety of currencies. By the end of 2013 the rate of new issuance had grown to about $900 billion, with a total amount outstanding of about $23,500 billion (these were mostly Eurobonds, but some were foreign bonds) - see Figure 7.1.

Figure 7.1 International bond and note (including foreign bonds) outstanding, December 2013

Source: Data from BIS Quarterly Review, March 2014 www.bis.org

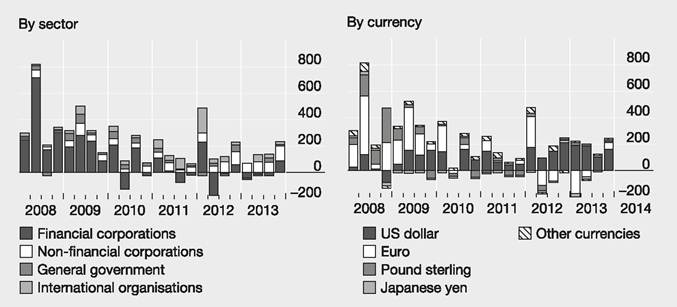

Figure 7.2 Net international debt securities issuance

Non-financial corporations account for a relatively small proportion in most years - see Figure 7.2. The biggest issuers are the banks and other financial institutions. Issues by governments and state agencies in the public sector account for a small fraction of issues. Other issuers are international organisations such as the World Bank, the International Bank for Reconstruction and Development and the European Investment Bank (also referred to as supranational organisations).

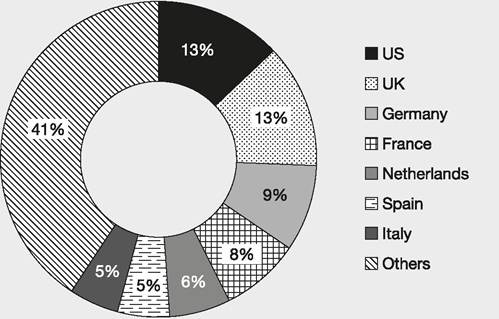

Even though the majority of Eurobond trading takes place through London, sterling trades are not as important as USD and EUR trades, and what is more, it tends to be large US and other foreign banks located in London that dominate the market. While American issuers are the largest, they account for less than one-seventh of all the issues because the issuing organisations are dispersed all over the world - see Figure 7.3.

Since the financial crisis Eurobonds have become increasingly important for financing European businesses, the growth in the market assisted by reduced appetite in banks for business lending and the ability to sell across the eurozone - see Article 7.4.

Figure 7.3 Percentage share of international bonds (including foreign bonds) outstanding at the end of 2013, by nationality of issuer

Source: Data from BIS Quarterly Review, March 2014 www.bis.org