Article 7.4 Eurobonds: a change of gear

By Ralph Atkins and Michael Stothard

Financial Times June 30, 2013

The Autostrada del Sole, which joins Italy's north and south and was completed in 1964, was as much part of the country's postwar revitalisation as Fiat 500 cars and film stars wearing Gucci loafers.

Behind the company that built the toll road was a deal that transformed global finance.On July 1, 1963, Autostrade had issued the world's first eurobond. Despite its name, the bond was dollar-denominated and pitched at US currency investors operating across national borders.

‘Capital at that time was not so accessible and the company wanted to reduce its reliance on the Italian state,' says Giovanni Castellucci, chief executive of Autostrade.

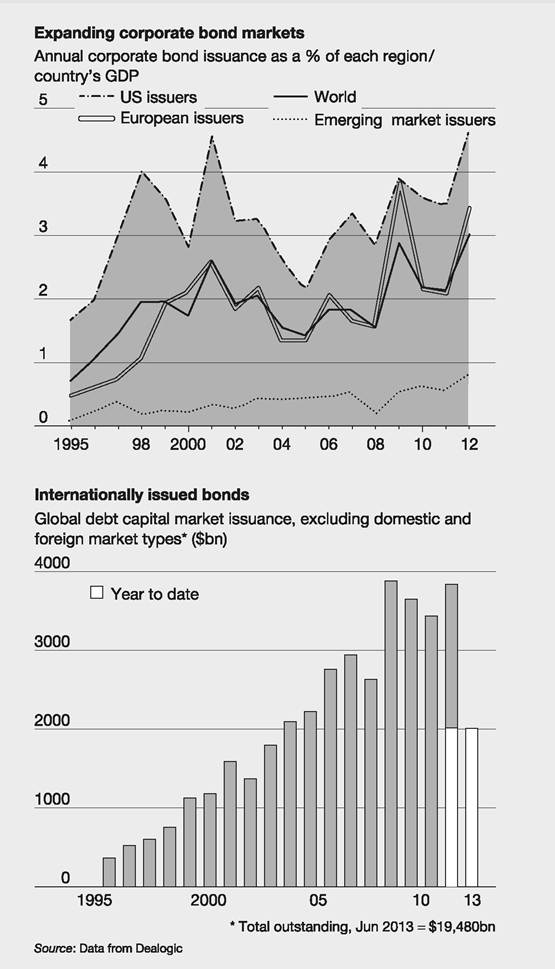

Exactly 50 years later, European corporate bond markets could be on the verge of another significant shift. Today's bond pioneers believe that weaknesses in the continent's banking system and historically low interest rates will encourage companies to tap capital markets much more for finance and rely increasingly less on bank loans.

Traditional bank ties remain strong, especially in continental Europe. On some measures, emerging economies have experienced a bigger shift towards capital market funding of companies since 2008. But just as the launch of eurobonds kick-started the globalisation of corporate finance, the crises of the past six years could bring Europe's markets closer to the depth and liquidity of those in the US. ‘In five to 10 years, I think the European market will look broadly similar to the US market in terms of bank and bond percentages,' says Michael Ridley at JPMorgan. Eurobonds were created out of necessity - as well as changes in the 1960s in US tax rules that encouraged investors to keep dollars outside the country. But their pioneers consider Autostrade's launch issue as part of a broader shift in capitalism in the decades after the second world war.

The success of eurobonds cemented London's position as Europe's financial capital. In 1999, came the launch of the euro, the continent's boldest experiment yet in economic integration. ‘Once the euro came into being, it accelerated hugely the growth of the European corporate bond market,' says Chris Whitman at Deutsche Bank.

The early years of this century saw a wave of issuance as European telecoms companies raised funds to buy 3G licences. ‘That was really the first time European markets had been aggressively peppered on a consistent basis by very large corporate deals,' recalls Bryan Pascoe at HSBC.

Cross-border issuance of corporate bonds has become ubiquitous. ‘Eurobonds largely replaced domestic markets in Europe - there was no point launching a bond in just one country when you can tap an international investor base at no extra cost,' says Chris O'Malley, whose book Bonds without borders will be published next year.

Mr Tuffey [head of investment-grade capital markets and syndicates] from Credit Suisse says: ‘The move towards capital markets in Europe has been slower partly due to uncertainty over regulation but also [because of] the huge players out there defending parochialism. German and French banks, for example, have historically lent to local corporates at generous rates.'

Meanwhile, many smaller European companies remain wary of the extra transparency required under today's more stringent rules. ‘It will be some time before midsized European companies overcome their disquiet about the regular reporting required by capital markets,' says Paul Watters at Standard & Poor's. ‘If you have a relationship with a bank, the detailed information that you provide remains private.' Data on corporate bond issuance show a move this year towards companies funding themselves more in debt markets and relying less on bank loans. Encouraging the shift will be low interest rates and increased concerns about the stability of banks - which have encouraged companies to pay much more attention to their funding requirements - and it could quickly become firmly established if European economies saw stirrings of a revival in growth.

With government finances under severe pressure and banks continuing to struggle, European policy makers want to promote alternative forms of finance. The European Commission has launched initiatives to encourage capital market development.

Paving the possible way ahead has been the rapid development of corporate bond markets in the world's emerging economies. During the past quarter, emergingmarket companies obtained three times as much funding from the bond markets as from bank syndicates, the biggest gap in at least a decade.

Additional reporting by Rachel Sanderson.

FT

Source: Atkins, R. and Stothard, M. (2013) Eurobonds: a change of gear, Financial Times, 30 June.

Types of Eurobonds

The Eurobond market is innovative in producing bonds with all sorts of coupon payment and capital repayment arrangements, for example the currency of the coupon changes half way through the life of the bond, or the interest rate switches from fixed to floating rate at some point. We cannot go into detail here on the rich variety but merely categorise the bonds into broad types.

1 Straight fixed-rate bond

The coupon remains the same over the life of the bond. These are usually paid annually, in contrast to domestic bond semi-annual coupons. The redemption of these bonds is usually made with a ‘bullet' repayment at maturity.

2 Equity related

These take two forms:

a Bonds with warrants attached

An equity warrant, for example, would give the right, but not the obligation, to purchase shares. There are also warrants for commodities such as gold or oil, and for the right to buy additional bonds from the same issuer at the same price and yield as the host bond. Warrants are detachable from the host bond and are securities in their own right, unlike convertibles.

b Convertibles

The bondholder has the right (but not the obligation) to convert the bond into ordinary shares at a pre-set price (see Chapter 6).

3 Floating-rate notes (FRNs)

These have variable coupons reset on a regular basis, usually every three or six months, in relation to a reference rate, such as Libor. The size of the spread over Libor reflects the perceived risk of the issuer. The typical term for a Eurobond FRN is about 5-12 years, but some companies, particularly banks, favour issuing perpetual, or undated, FRNs.

4 Zero coupon bonds

These pay no interest but are sold at a discount to face value so that the holder receives a gain in a lump sum at maturity - also called pure discount bonds. This is of investor benefit in countries where income is taxed more onerously than capital gains.

5 Dual-currency bonds

These bonds pay the coupon in one currency but are redeemed in a different currency. The redemption currency is usually the US dollar and the coupon payments are often made in a currency which offers the issuer the chance of a lower rate of borrowing.

Within these broad categories all kinds of ‘bells and whistles' (features) can be attached to the bonds, for example reverse floaters - the coupon declines as benchmark interest rate, say Libor, rises - and capped bonds - the interest rate cannot rise above a certain level. Many bonds have call back features under which the issuer has the right, but not the obligation, to buy the bond back after a period of time has elapsed, say five years, at a price specified when the bond was issued. This might be at the par value but is usually slightly higher. Because there are real disadvantages for investors, bonds with call features offer higher interest rates. Issuers like call features because a significant price rise for the bond implies that current market interest rates are considerably less than the coupon rate on the bond. They can buy back the original bonds and issue new bonds at a lower yield. Also some bonds place tight covenant restrictions on the firm so it is useful to be able to buy them back and issue less restrictive bonds in their place.

Finally, exercising the call may permit the corporate to adjust its financial leverage by reducing its debt. A Eurobond may also have a ‘put' feature (see Chapter 4).Issuance

The majority of Eurobonds (more than 80%) are rated AAA or AA, although some are issued rated below BBB-. Denominations are usually $1,000, $5,000, $10,000, $50,000 or $100,000 (or similar large sums in the currency of issue - known as 1,000, 5,000 or 50,000 lots or pieces). Details of some international bonds are shown in Tables 7.2 and 7.3 taken from FT.com. The issue process leading to this point is described in Chapter 4. Note the large volume of money raised in this market in one week (selected at random).

Table 7.2 New international bond issues, 7 August 2014

| Borrower | Amount m. | Coupon % | Price | Maturity | Fees % | Spread bp | Book runner |

| US Dollars | |||||||

| Ecobank Nigeria | 200 | 8.75 | 99.011 | aug 2021 | Undiscl | Deutsche Bank/Standard Chartered/Ned | |

| Euros | |||||||

| Hamburg IBB | 300 75 | 1 FRN | 100.747 100.000 | jun 2021 aug 2020 | 6mE | Undiscl Undiscl | CMZ/HSH Nord/ LBBW/WGZ/ IBB |

| Swiss Francs | |||||||

| Canton Ticino | 100 | 0.625 | 101.055 | maj 2022 | Undiscl | Credit Suisse/ BasleKB | |

Bond issue details are online at ft.com/bondissues.

Final terms, non-callable unless stated. Spreads relate to German govt bonds unless stated.Source: Thomson Reuters

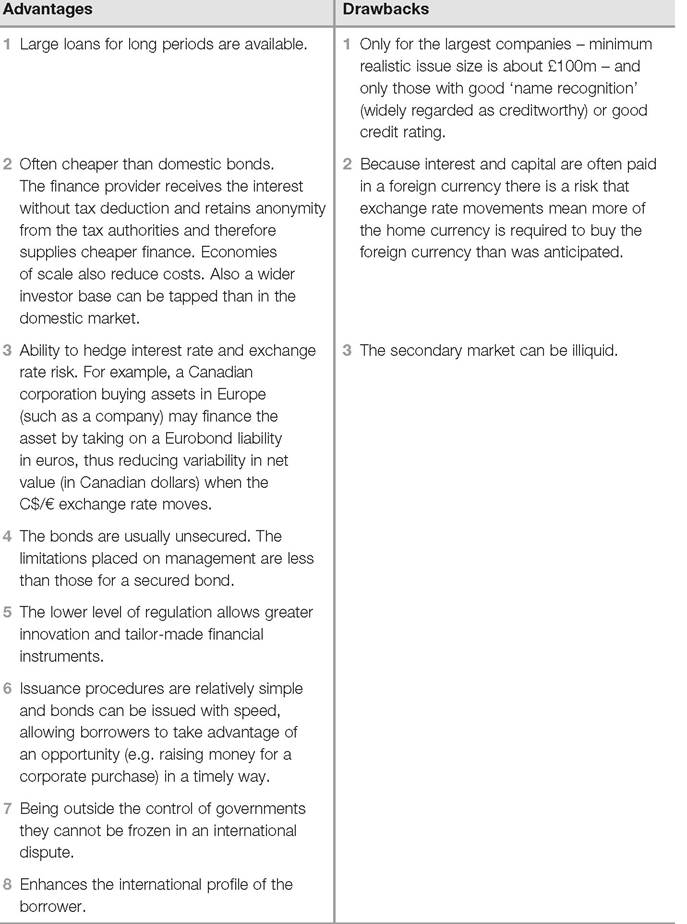

Eurobonds present significant advantages to their issuers relative to domestic bonds - see Table 7.4, which also lists their drawbacks.

Secondary market

Eurobonds are traded on the secondary market through intermediaries acting as market makers. Some bonds are listed on the London, Dublin, Luxembourg, Channel Islands or other stock exchanges around the world. Listing enables some institutions to invest that would otherwise be prohibited. Despite this, the market is primarily an over-the-counter one. Most deals are conducted using the telephone, computers, telex and fax, but there are a number of electronic platforms. The extent to which electronic platforms will replace telephone dealing is as yet unclear. It is not possible to go to a central source for price information. Most issues rarely trade; those that do are generally private transactions between investor and bond dealer and there is no obligation to inform the public about the deal.

Table 7.3 New international bond issues weekly summary, 15 August 2014

| Borrower | Amount m. | Maturity | Coupon % | Price | Launch spread bp | Moodys/S&P Ratings Book-runner |

| US Dollars | ||||||

| American Water Capital Corp | 200 | 01-12-2042 | 4.3 | 99.589 | BofA Merrill/RBC ÑÌ/ÐÂÇß Securities | |

| American Water Capital Corp | 300 | 01 -03-2025 | 3.4 | 99.857 | RBS/BofA Merrill Lynch/RBC ÑÌß Securities | |

| Burlington Northern | 700 | 01 -09-2024 | 3.4 | 99.771 | Citi/BofA Merrill Lynch/Goldman Sachs | |

| Burlington Northern | 800 | 01 -09-2044 | 4.55 | 99.446 | Citi/BofA Merrill Lynch/Goldman Sachs | |

| CBS Corp | 550 | 15-08-2044 | 4.9 | 98.639 | CS/Deutsche Bk∕BofAML√RBS∕UBS∕BNPP∕Mizuho∕SMBC Nikko | |

| CBS Corp | 600 | 15-08-2019 | 2.3 | 99.696 | CS/Deutsche Bk∕BofAML√RBS∕UBS∕BNPP∕Mizuho∕SMBC Nikko | |

| CBS Corp | 600 | 15-08-2024 | 3.7 | 99.76 | CS/Deutsche Bk∕BofAML√RBS∕UBS∕BNPP∕Mizuho∕SMBC Nikko | |

| China Constr Bark | 750 | 20-08-2024 | 4.25 | 99.577 | ANZ∕BofAML√CCB International/Citi/BeutscheBank/HSBC/UBS | |

| Consumers Energy | 250 | 31 -08-2064 | 4.35 | 99.137 | Scotia Capital/Barclays/RBCCM/SuntrustRobinsonHumphrey/WFC | |

| Consumers Energy | 250 | 31 -08-2024 | 3.125 | 99.898 | bgcolor=white>Scotia Capital/Barclays/RBCCM/SuntrustRobinsonHumphrey/WFC | |

| Culfport Energy Corp | 300 | 01-11-2020 | 7.75 | 106 | Credit Suisse | |

| Minerva Luxembourg | 200 | 31-01-2023 | 7.75 | 100 | *Banco BTG Pactual/HSBC/ltauBBA/BofA Merrill Lynch/Santander* | |

| PRICOA Global Funding I | 500 | 18-08-2017 | 1.35 | 99.93 | *Citi∕Credit Suisse/JP Morgan/Wells Fargo* | |

| UBS AG Stamford | 1250 | 14-08-2017 | 1.375 | 99.678 | UBS Investment Bank | |

| UBS AG Stamford | 2500 | 14-08-2019 | 2.375 | 99.836 | UBS Investment Bank | |

| World Bank | 100 | 28-08-2019 | 1.7 | 100.000 | Morgan Stanley | |

| Euros | ||||||

| Baden Wuerttemburg | 300 | 18-07-2022 | 1 | 100.030 | DZ/HSH Nord/HSBC/LBBW/Nord/LB/Nordea | |

| BayemLB | 100 | 13-08-2021 | 1.25 | 99.970 | BLB | |

| BP | 300 | 15-03-2040 | 2.75 | 114.015 | BAML√CMZ∕LBBW∕Nord∕LB∕RBS | |

| HSH Nordbank | 125 | 21-08-2017 | FRN | 99.927 | 3mE+59 bps | HSH Nordbank |

| IBB | 100 | 19-08-2022 | FRN | 100.000 | 3mE+12.5 bps | IBB |

| IBB | 50 | 21-08-2019 | FRN | 99.950 | 3mE+8 bps | LBBW |

| Lower Saxony | 500 | 18-08-2022 | 1 | 99.725 | CMZ/Nord/LB/BLB/LBBW | |

| Sterling | ||||||

| ElB | 200 | 01-02-2019 | 1.5 | 98.565 | Deutsche Bank/HSBC | |

| Swiss Francs | ||||||

| Canton de Vaud | 250 | -/-/2023 | 2 | 112.193 | ZKB | |

| Credit Suisse | 370 | 18-08-2015 | FRN | 100.000 | 3mL+22bps | Credit Suisse |

| Credit Suisse | 155 | 19-08-2016 | FRN | 100.000 | 3mL+27bps | Credit Suisse |

| Municipality Finance | 150 | 17-09-2024 | 0.75 | 101.328 | Credit Suisse | |

| Total | 800 | 29-08-2024 | 1 | 100.584 | UBS | |

| WeIIsFargo | 250 | 30-09-2020 | 0.625 | 100.456 | Credit Suisse/UBS | |

| WeIIsFargo | 250 | 03-09-2024 | 1.25 | 100.513 | Credit Suisse/UBS | |

| Australian Dollars | ||||||

| KBN | 150 | 16-07-2025 | 4.25 | 100.213 | TD∕WBC | |

| Province of Ontario | 225 | 22-08-2024 | 4.25 | 99.096 | TD Securities | |

| Norwegian Krone | ||||||

| VWFS | 500 | 22-08-2017 | 2 | 99.727 | ANZ/Deutsche Bank | |

| Swedish Krona | ||||||

| Hemso Fastighets AB | 200 | 26-01-2016 | FRN | Undisclosed | 3mS+40 bps | DanskeZHandeIsbanken |

| Lansforsakringar Bank | 200 | 21-08-2017 | FRN | 100.000 | 3mS+37 bps | Swedbank |

| VWFS | 500 | 22-08-2016 | 0.96 | 100.000 | Handelsbanken |

Bond issue details are online at ft.com/bondissues. Final terms, non-callable unless stated. Spreads relate to German govt bonds unless stated.

Source: Thomson Reuters

Table 7.4 Advantages and drawbacks of Eurobonds as a source of finance for corporations

Euro medium-term notes and domestic medium-term notes

By issuing a medium-term note (MTN) a company promises to pay the holders a certain sum on the maturity date, and in many cases coupon interest in the meantime. These instruments are typically unsecured and may carry floating or fixed interest rates. Medium-term notes have been sold with a maturity of as little as 9 months and as great as 30 years, so the term is a little deceiving, but the period is usually 5-10 years. They can be denominated in the domestic currency of the borrower (MTN) or in a foreign currency outside the control of the authorities of the currency (Euro MTN). MTNs normally pay an interest rate above Libor, usually varying between 0.2% and 3% over Libor.

An MTN programme stretching over many years can be established with one set of legal documents. Then, numerous notes can be issued under the programme in future years. Such a programme allows greater certainty that the firm will be able to issue an MTN when it needs the finance and allows issuers to bypass the costly and time-consuming documentation associated with each stand-alone note/bond. The programme can allow for bonds of various qualities, maturities, currencies or type of interest (fixed or floating). Over the years the market can be tapped into at short notice in the most suitable form at that time, e.g. US dollars rather than pounds, or redemption in three years rather than in two. It is possible to sell in small amounts, e.g. $5 million, and on a continuous basis, regularly dripping bonds into the market. The banks organising the MTN programme charge a commitment fee on any available funds authorised by the programme but not used. Management fees will also be payable to the syndication of banks organising the MTN facility.

The success of an MTN programme depends on the efficiency of the lead manager and the flexibility of the issuer to match market appetite for lending in particular currencies or maturities with the issuer's demands for funds. The annual cost of running an MTN programme, excluding credit rating agency fees, can be around £100,000. The cost of setting up an MTN programme is high compared with the cost of a single bond issue (and more expensive than most bank debt, except for the very best AAA, AA and some A-rated companies). Many companies are prepared to pay this because they believe that the initial expense is outweighed by the flexibility and cost savings that a programme can provide over time.

Vodafone's MTN programme is one of the most varied I have come across. If you download an annual report you will find a list of over two dozen MTNs in issue, with a wide variety of currencies, maturities and coupon payment intervals (see Vodafone's Notes to the accounts). It has two MTN programmes: a ˆ30 billion medium-term note (EMTN) programme and what is called a ‘US shelf programme'. The US shelf programme (shelf registration or shelf offering or shelf prospectus) is one where there is a single prospectus approved by the Securities and Exchange Commission at the outset under which numerous MTNs can be issued in subsequent years. For each issue the borrower must file a short statement pointing out material changes in its business and finances since the shelf prospectus was filed.

Here is a summary of three examples of Vodafone's MTNs:

• Australian dollars (A$250 million) raised at an interest rate of 6.75% with a semi-annual coupon. Minimum purchase for lenders of A$100,000.

• ˆ1.25 billion raised as a floating-rate note. Interest is Euribor (variable rate in euros - discussed in Chapter 8) plus 35 basis points. Interest is payable quarterly. Minimum denomination of ˆ50,000.

• £250 million raised with a coupon of 5.625% and due to mature in 2025. Interest is paid annually and the minimum denomination is £50,000.

Islamic bonds (sukuk)

From its inception in 1975, when the Islamic Development Bank and the Dubai Islamic Bank (the first commercial Islamic bank) were established to operate in strict accordance with sharia (shari'ah) law, Islamic finance has made significant progress worldwide. It is growing much faster than traditional banking and global Islamic investments now exceed $1 trillion. Most of this is bank based, but some is bond market based (i.e. sukuk).

Sukuk (the plural form of the Arabic word sakk, meaning legal document or certificate, from which the word cheque is derived) are bonds which conform to sharia law, which forbids interest income, or riba. However, Islam does encourage entrepreneurial activity and the sharing of risk through equity shares.

There was always a question mark over the ability of modern finance to comply with Islamic sharia law, which not only prohibits the charging or paying of interest but insists that real assets underlie all financial transactions. Money alone should not create a profit and finance should serve the real economy, not just the financial one. Ways have been found to participate in the financial world while still keeping to sharia law, although certain Islamic scholars oppose some of the instruments created.

Whereas conventional bonds are promises to pay interest and principal, sukuk represent part ownership of tangible assets, businesses or investments, so the returns are generated by some sort of share of the gain (or loss) made and the risk is shared.

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), which is based in Bahrain and sets standards for Islamic finance, defines sukuk as:

certificates of equal value representing undivided shares in ownership of tangible assets, usufructs and services or (in the ownership of) the assets of particular projects or special investment activity.

Sukuk are administered through a special purpose vehicle (SPV), a company set up as a separate organisation for a particular purpose, which issues sukuk certificates. These certificates entitle the holder to a rental income or a profit share from the certificate. Sukuk may be issued on existing assets as well as specific assets that may become available at a future date.

Currently, there is some confusion over whether investors can always seize the underlying assets in the event of default on sukuk or whether the assets are merely placed in a sukuk structure to comply with sharia law. Lawyers and bankers say that the latter is the case, with most sukuk being, in reality, unsecured instruments. They differentiate between ‘asset-backed' and ‘assetbased' sukuk:

• Asset-backed: there is a true sale between the originator and the SPV that issues the sukuk, and sukuk holders own the underlying asset and do not have recourse to the originator in the event of a payment shortfall. The value of the assets owned by the SPV, and thence the sukuk holders, may vary over time. The majority of sukuk issues are not asset backed.

• Asset-based: these are closer to conventional debt in that they hand investors ownership of the cash flows but not the assets themselves; the sukuk holders have recourse to the originator if there is a payment shortfall.

There is no overarching regulator for Islamic finance but the rulings of the AAOIFI are most widely followed in the Gulf. In Malaysia and other parts of Asia other guidelines are adopted.

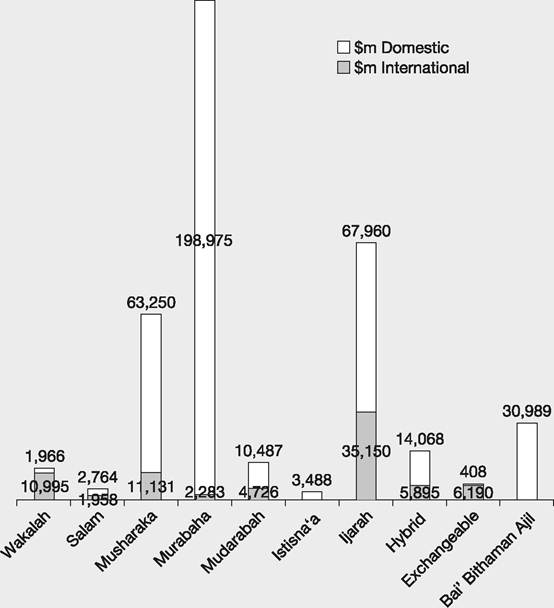

At the beginning of 2013 3,875 sukuk had been issued, 223 international and 3,652 domestic, with a total issuance value of $473 billion. The most common types of sukuk are:

• Bai’ Bithaman Ajil - the issuer sells an asset(s) to investors with the promise that it will buy the asset back at a predetermined price which allows for a profit to the finance provider(s). Payment is on a deferred or instalment basis over a pre-agreed period. The assets generally comprise land, buildings, vehicles and equipment.

• Ijarah - one of the most common sukuk types, this is a leasing contract, for well-defined assets, in which the lessee can gain benefit from the use of equipment or other asset in return for regular lease payments providing a return to sukuk holders. Some types permit legal title to be passed to the user after the end of the lease, others do not. The ijarah contract is a binding contract which neither party may terminate or alter without the other's consent.

• Istisna’a - this is the financing of manufacturing, assembly or construction capacity by arranging money to be transferred from the finance providers prior to production. Payment is made at an agreed price for something that does not yet exist in a lump sum or in instalments. The finance providers may sell the asset once created. It is not necessary that the seller itself is the manufacturer, merely that it causes the manufacture to take place. The item must be described in detail and construction must fit the specifications. Istisna'a is invalid for an existing asset or for natural things such as corn or animals.

• Mudarabah - this is for when a partnership between two parties is formed. One party acts as capital provider(s), giving a specific amount of capital to another person, a named entrepreneur, to make use of the capital given for the benefit of the business. Profits are shared according to a pre-arranged ratio. Losses are borne by the finance providers.

• Murabaha - this a fixed-income bond for the purchase of an asset such as property or a vehicle, with a fixed rate of profit for the finance providers determined by a fixed profit margin. The asset acts as collateral until the contract is settled. It is similar to rent-to-own arrangements, with sukuk holders as owners and creditors until all required payments are made.

• Musharakah - these are for business venture partnerships between two or more people/organisations where money comes from all the partners. A profit and loss sharing contract is made and all partners have a right to share in the management. Profit or losses would be divided according to their contribution.

• Salam - this is a sale whereby the seller undertakes to supply some specific goods to the buyer at a future date in exchange for an advanced price fully paid at spot. Salam is used to finance agricultural goods.

• Wakalah - the organisation that wants to be financed (e.g. a financial institution) acts as an agent for the finance providers to purchase the sharia- compliant products. An example from the UK's HM Revenue and Customs: ‘The investor receives only the agreed ratio against investment. Anything made above that ratio is kept by the financial institution and not given to the investor. Example: an investor agrees to invest a sum with the bank for an agreed return (e.g. 5%). The bank pools the investor's funds with the funds of other investors and its own capital and invests in Sharia compliant assets. At the end of a given period (e.g. a month) the bank returns the invested sum to the investor along with the agreed 5%. Any additional revenue that the bank makes on the customer's money is kept by the bank (e.g. if the bank makes 6% then 5% is given to the customer and the additional 1% is kept by the bank). If the bank does not make the agreed percentage return then the investor gets what has been made whilst the bank gets nothing (e.g. if only 4% is achieved then the investor gets the full 4%).' (www.hmrc.gov.uk/manuals/vatfinmanual/vatfin8500.htm)

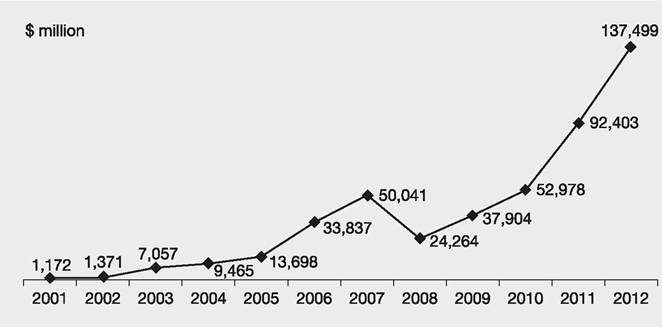

The first sukuk (a Bai Bithaman Ajil) was issued in 1990 in Malaysia by Shell and denominated in the Malaysian currency, ringgit. International sukuk were introduced in 2001 with the $100 million sovereign ijarah issue by the Central Bank of Bahrain, and the market has grown rapidly since then, albeit with a blip as a result of the 2008 global crisis - see Figures 7.4 and 7.5. It is estimated by the International Islamic Financial Market (IIFM) that there is more than $230 billion ($191 billion of domestic and $45 billion of international) sukuk outstanding, and this figure is expected to increase rapidly.

Malaysia takes the lion's share of the domestic market, with nearly 80% of the world total, and has 12% of the international market. United Arab Emirates dominates the international market with 44%, followed by Saudi Arabia with 13%, and then Malaysia. The UK and Luxembourg are important European

Figure 7.4 International and domestic sukuk issuance, 2001-2013

Source: Data from Islamic International Financial Market, sukuk issuance database

Figure 7.5 Amount of sukuk issued each year from 2001 to 2012

Source: Data from IIFM, sukuk issuance database

centres for Islamic finance. In the UK there are more than 20 banks providing this service and numerous professionals skilled and experienced in its complex details. To April 2015 more than US$38 billion had been raised through 53 issues of sukuk on the London Stock Exchange. See Article 7.5 for a discussion on the competition between financial centres for Islamic finance.