Article 6.9 ‘Sudden death' bank bonds on the increase

By Christopher Thompson and Tracy Alloway

Financial Times August 29, 2013

Some call them ‘sudden death' bonds; others talk about ‘wipeout' bonds. Both refer to the potential of some cocos, or contingent convertible bonds issued by banks, to turn debt investors' gold into lead.

Either way, European banks are issuing them in growing numbers despite mounting criticism that they discriminate against investors.As regulators encourage banks to hold more capital where investors would take losses if a bank defaults, cocos are seen as a relatively quick fix when it comes to bolstering tier one capital ratios.

Tier one capital, a key regulatory measure of financial health, is considered the safest portion of a bank's capital and traditionally comprises common equity and retained earnings.

There have been two types of coco to date: those which convert into equity when a bank's capital ratio falls below a pre-agreed trigger and those which are written off entirely.

It is the latter that are proving controversial - and increasingly popular.

‘The bank doesn't have to default to trigger these cocos... the point is they can push losses on to bondholders and provide capital while the bank is still a going concern,' says Jenna Barnard at Henderson.

Such criticism has not deterred the banks, particularly as demand has been buoyed by wealthy Asians who can snap up cocos with borrowed money, bolstering their returns.

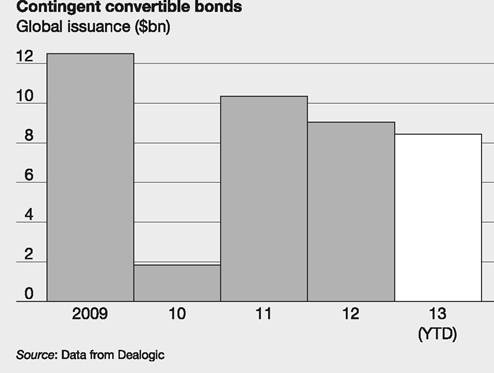

Year to date global coco issuance stands at $8.5bn from eight deals, a record number, according to figures from Dealogic, all from European banks.

Keith Skeoch, chief executive of UK life company Standard Life, describes wipeout cocos as ‘death-spiral bonds'. However, he says they have a role where ‘there is a desperate need, particularly in the banking sector, for the provision of loss absorbing capital'.

Barclays issued a $3bn death spiral coco last November and followed it up with another $1bn issue in April.

They yielded 7.6% and 7.7% respectively.Earlier this month Credit Suisse issued its own $2.5bn wipeout coco, which yielded 6.5%, that followed a $1bn issue from Belgium's KBC with an interest rate of 8%.

The Swiss bank said similar issues would follow, not least as it seeks to lock in historically low interest rates and take advantage of investors’ hunger for relatively high-yielding instruments.

It is why even coco critics, such as Ms Barnard, admit the asset class ‘will become quite hard to ignore’.

Other banks are choosing to plot a middle path.

Societe Generale is preparing what it refers to as a ‘write-down, write-up’ hybrid bond in which investors would take losses if the bank’s tier one capital falls below 5.1%. However, if the bank recovers, bondholders would begin to get their money back.

‘It’s not exactly a coco but it has a writedown mechanism... if the trigger is reached only a proportion will be written down, depending on where the capital ratio of the bank stands,’ says Stephane Landon, Societe Generale’s head of asset and liability management. ‘If the bank gets better this amount can be reinstated and so the bond can be reinstated.’

In the US, a more restrictive definition of regulatory capital effectively prevents US banks from including cocos in their tier one buffers.

US regulators are said to have been scarred by their experience during the financial crisis with other types of hybrid bank instruments combining equity and debt characteristics. Many of these hybrid products failed to absorb bank losses during the financial crisis.

FT