Article 6.10 Coco sell-off unveils high-yield bargains

By Christopher Thompson

Financial Times August 14, 2014

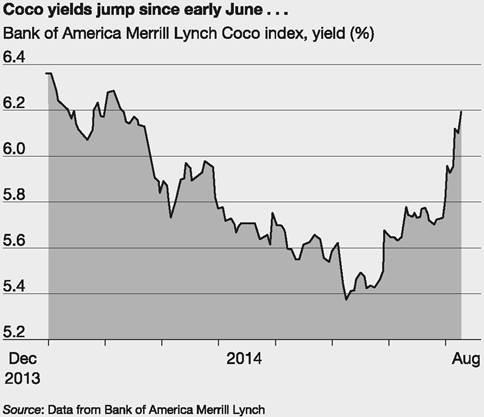

Is that the sound of the coco bubble going pop? Yield-hungry investors have had their appetites sorely tested over the past few weeks as high-risk, high-return contingent convertible bonds, or cocos, recorded their worst monthly performance to date.

Cocos are hybrid bonds which count towards a bank's capital. Banks can issue cocos up to the value of 1.5% of their risk-weighted assets under incoming Basel III rules.

‘Regulatory headwinds and Bank of America Merrill Lynch's ruling that cocos will no longer be eligible for high yield or investment grade indices, has led to a strong sell off in the sector,' says Armin Peter at UBS.

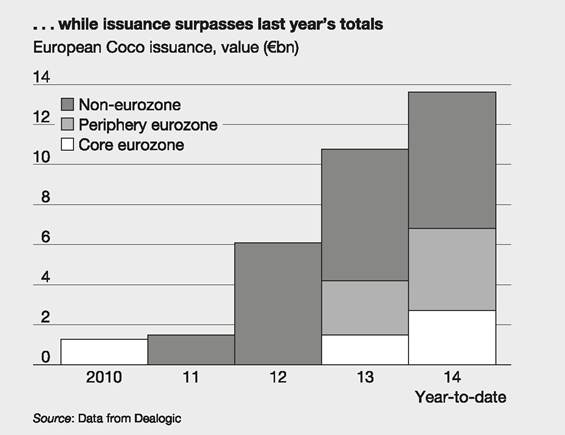

The UK's Financial Conduct Authority earlier this month announced a ban on retail investors buying cocos, which now constitute a ˆ45bn market according to RBS, albeit one dominated by institutions and hedge funds.

Some see the sell-off as restoring a measure of sobriety to what had become an increasingly frenzied market whose gyrations were exacerbated in part due to fastmoney investors selling-out at the first sign of trouble.

The sell-off comes on the back of frantic coco buying. In May average yields hit a record low of 5.54%, while Deutsche Bank reported about ˆ25bn of orders for its maiden ˆ1.5bn coco, underlining investor willingness to shoulder more risk in their hunt for higher-yielding bank assets.

‘When I see cocos at 5.5% I personally don't think I'm getting paid for the risks,' says Jorge Martin Ceron, a portfolio manager at Lombard Odier.

The bond's conversion mechanism - which can allow for coupon cancellations even while the bank is a ‘going concern' and potentially paying dividends to shareholders - remains untested.

Coco supporters point out that European banks' continued deleveraging and recent capital raising has made the prospect of outright conversion, if not coupon cancellations, increasingly unlikely. But the wider market fallout highlights the asset's exposure to ‘tail-risks', or unforeseen events.Regulatory incentives remain for banks to tap the coco market, not least because they offer a cheaper way of raising capital than issuing equity. ‘For banks, using cocos is still a very cost effective way to fill your capital bucket,' says Mr Weinberger [head of capital markets engineering at Societe Generale].

FT

Catastrophe bonds

These are issued by insurance companies. If no major catastrophe, e.g. earthquake in California, occurs they pay coupons and a redemption amount at the end of their lives, usually around three years. If the specified catastrophe does occur before maturity the principal and further coupons are ‘forgiven' by the holders: they get no more money from the insurance company. Thus the insurance company has passed on some of the risk - see Article 6.11.

More on the topic Article 6.10 Coco sell-off unveils high-yield bargains:

- Article 6.4 Loan terms eased in search for yield

- Article 7.3 Sub-Saharan market: high yields fire appetite for African Eurobonds