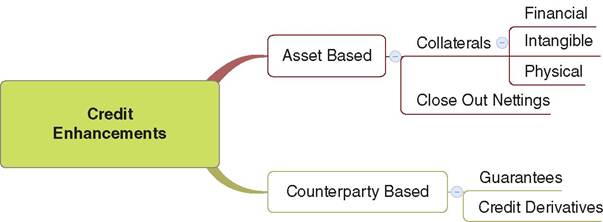

ASSET-BASED CREDIT ENHANCEMENTS

Physical, financial and intangible collateral are assets that reduce the net exposure of a contract and shield against credit losses. These assets legally belong to the borrowers, yet lenders have

FIGURE 10.2 Main types of credit enhancements

the legal rights to liquidate them in case of a default event to cover credit losses.

Whenever one can sell collaterals and readily turn them into cash, we speak of asset-based collaterals.Physical collateral is one kind of asset-based credit enhancement. It describes tangible assets such as real estate and physical commodity goods, such as precious metals, oil, natural gas, etc. In a mortgage loan, typical physical collateral is the house that the borrower purchases with the loan. If he/she defaults, the house undergoes liquidation. It will go on sale to raise proceeds to reduce outstanding credit losses. Note that the market largely determines the value of physical collateral. Thus, in terms of price/value analysis, it is common to link them with price indexes. For instance, for mortgage collateral the House Price Index (HPI) is used to monitor the prices and their possible evolution over time. Note that we rarely link physical collateral to counterparties, so there is no direct counterparty credit risk.

Another kind of asset-based credit enhancement is financial collateral such as stocks, or bond contracts, that are available for liquidation in case of default. Both market and counterparty credit risk factors impact the value of such assets. For instance, credit spreads play an important part in the valuation of bonds, which are used as collaterals.

Intangible assets used as collateral can be intellectual properties, patents, copyrights, trademarks, trade secrets, and others. The value of such assets is hard to estimate accurately, especially after the event of default.

For instance, the value of the trademark is expected to decline dramatically when a corporate defaults; however, the value of patents may hardly decrease at all. These collaterals are usually exercised as one of the last resources for covering credit losses.Close-out netting is applied when a borrower has a number of predefined assets and agrees to make them available in case of default. Close out netting consist of two components: close out, which is the right to terminate the transaction with the defaulted counterparty and any contractual payments; and netting, which defines the right to offset amounts due at termination of individual contracts to determine a net balance (positive/negative values). In other words, the borrower may force these assets into liquidation to cover credit losses. For this agreement to be valid, it is obvious that the availability of the assets must be well set and defined.

Note that any change of rating (e.g., downgrading, default/credit spreads of the assets, considered in the close out process), will impact their values and thus must be counted in the net balance process.

10.2.1 Allocating collateral to credit exposures

Collaterals agreements can either be attached to specific exposures or to counterparties, such as the borrower. In the former case, they are only covering the credit losses of the particular exposures, whereas in the latter they are covering all possible exposures of the counterparty.

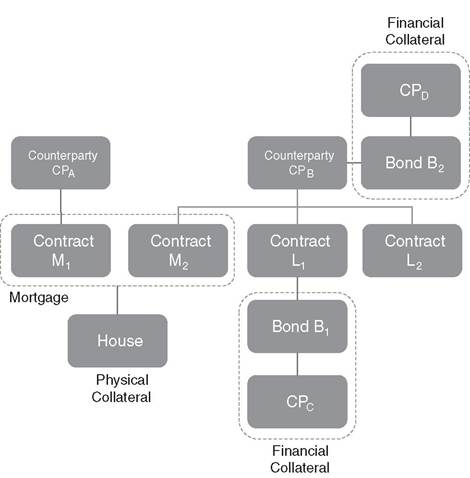

The structure of the applicability and use of collateral may have different degrees of complexity, depending on the types and number of collaterals attached to credit exposures. For instance, there are cases where a credit exposure is shared among counterparties, and a single exposure is attached to more than one collateral directly or indirectly. Let us think about the case illustrated in Figure 10.3, where a house mortgage contract M is shared, defined as M1 and M2, among counterparty CPa and CPB respectively; in such a loan the house is used as the physical collateral.

Moreover, CPB has two other contract loans L1 and L2; the former loan is collateralized by using a bond B1, which has been issued by the CPc. Finally, all the loans belonging to counterparty CPB are also collateralized by the asset of bond B2, which has been issued by the CPD. Both house and bond B1 will be used against losses that may occur

FIGURE 10.3 Example of applying collaterals to credit exposures

in the particular exposures that they are linked to; however, bond B2 will be used to cover the credit losses initiated from any credit exposure of CPb. The sequence of collateral usage may not be straightforward; the collateral management process usually defines it.

10.2.2 Valuing and adjusting asset-based credit enhancements

Depositors are eligible to liquidate asset-based credit enhancements that refer to borrower’s credit exposures. During this liquidation process, the valuation rule plays a critical role. There are several approaches to valuation, such as nominal and fair value, mark-to-market, net present value, and more. Mark-to-market and net present value (NPV) are the most common when it comes to the liquidation of credit enhancements after the credit default event. The choice of several interpretations to value by applying different valuation rules is critical for estimating the net exposures and the marketability at the time of liquidation. For instance, using mark-to-market valuation for a mortgage loan, we need to approximate the price of a house at future possible time of default.

The value of asset-based credit enhancements can also fluctuate through time due to volatile market conditions. Prices of stocks, commodities, and real estate will hardly remain static and will always change in the future. A common way to adjust such volatilities is by applying haircuts. Typically, the approaches for estimating haircuts are based on statistical analysis, i.e., observing the market volatilities of such products, deterministic scenarios based on certain assumptions, and/or VaR models, e.g., historical, parametric, stochastic Monte Carlo, etc. Haircuts of credit enhancements are helpful in identifying their volatility and adjusting the net credit exposures; such value adjustment will also define the expected credit losses.

10.3