COUNTERPARTY-BASED CREDIT ENHANCEMENTS

There are contractual agreements where counterparties agree to cover credit losses. Such agreements defined as guarantees and credit derivatives are the counterparty-based credit enhancements.

In a guarantee contract, a counterparty will continue to fulfill the agreed obligations in case the obligor, e.g., borrower, defaults. The counterparty protection seller in credit derivatives agrees to protect the protection buyer against credit risk events.10.3.1 Guarantees

A guarantee is a counterparty-based credit enhancement where a counterparty agrees to cover the credit losses of a lender, partially or fully, in case the borrower defaults on fulfilling the agreed obligations. Therefore, in the case of a default, a guarantee effectively shifts the credit exposure from the borrower to the guarantor.

In fact, a guarantee is a legal promise to the lender, defined in a new financial contract. The new legal “promise” implies that there is an additional degree of trust between the borrower and the guarantor. This explains why, during the lifetime of the credit exposure, guarantors must always have higher credit rating than the borrower. Therefore, the credit rating of an additional counterparty must be monitored which introduces additional effort and cost when guarantees are used.

The actual value of the guarantee is defined by considering the valuation roles applied in the financial contract that the guarantor agrees to cover. Usually, the values of the exposures and of a guarantee contract are defined with nominal values (NVs).

Loans provided to corporate clients often use a parent or sister company or a related bigger corporate company as guarantors. The reason is that these companies have a higher credit rating, i.e., credit trust. In this case, the hierarchies and group structures of the counterparties can be very useful. The hierarchical levels define the role of the counterparties and the degree of dependency, e.g., who owns whom and how much.

This could also be helpful in terms of collateralization. When considering, for example, that a parent company may guarantee all its legal subsidiaries, the collateralization process—the defining order and amount of credit exposure—plays a key role in loss coverage. Counterparty and guarantee dependencies using hierarchies can also be used in the identification of specific wrong way risk, as explained in the following paragraphs.10.3.2 Allocating guarantees to credit exposures

As with collaterals, guarantees can involve a single or several counterparties or contractspecific exposures. When guarantors agree only to a single exposure, they promise to cover the corresponding potential losses; on the other hand, multiple coverage of credit exposure applies only if the guarantees attached to more than one exposure and/or to the counterparty have multiple exposures.

The degree of complexity for structuring the coverage of credit losses, based on guarantors, depends on the allocation of guaranteed contracts across the different exposures. Consider

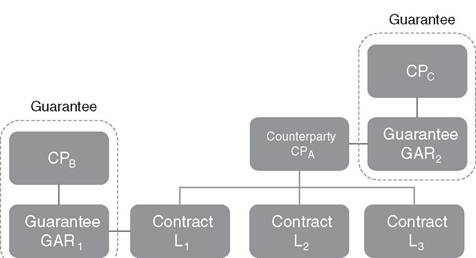

FIGURE 10.4 Example of applying guarantees to credit exposures

Figure 10.4, for instance, where a guarantee GAR1 is allocated to (i.e., covers) a single exposure L1, whilst a guarantee GAR2 is attached to a counterparty CPa and thus allocated to all related credit exposures, i.e., L1, L2, and L3.

10.3.3 Creditderivatives

Credit derivatives are securitization products similar to guarantee contracts with the purpose of protecting investors against credit risk. At the same time, they are more flexible than guarantees. There are several types of derivative contract agreements such as credit default swaps (CDS), total return swaps (TRS), CDS on asset-backed securities, credit spread option, collateralized debt obligation (CDO), CDS index products, and many more.

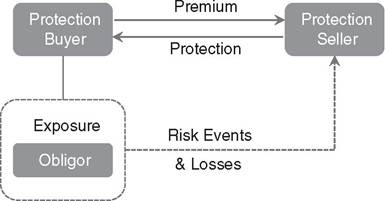

The thing they have in common is that at least one of the underlying variables refers to credit risk event. A more detailed explanation of the structure of derivatives is beyond the scope of this book. What follows simply highlights some of the important characteristics of derivatives that we will revisit later when we discuss marketplace lending.There are three main counterparties involved in credit derivatives: the obligor (also called borrower) who is linked to the underlying credit exposure; the protection buyer (e.g., the lender), who is exposed to the associated credit risk; and the protection seller who provides insurance protection against a credit event and receives a premium. The protection seller guarantees the credit exposure against credit events and covers credit losses that occur, as specified in the derivative agreement. Figure 10.5 illustrates the main elements and simple structure of credit derivatives.

In a sense, the protection seller is acting as a guarantor, agreeing to insurance against a predefined credit event. However, it is sometimes unknown whether such an insurer will be able to fulfill the agreed insurance obligations. On the other hand, protection sellers may have an unclear understanding of the credit exposure and the credit status of the obligors linked to underlying credit exposures. A typical instrument that has fallen into this issue is the collateralized debt obligation (CDO) square financial products, which had rather high degrees of fuzziness in regards to the underlying exposures and credit quality of the protected counterparties.

Credit derivatives may have rules that are more flexible in regards to the counterparty credit events' definitions including, for instance, the credit event of default or downgrading

FIGURE 10.5 Simplediagramillustratingthemain elements and structure of credit derivatives

of the counterparty rating status.

Thus, it is very important that in credit derivatives contracts there is a precise definition of the credit risk events as well as a way to determine1 when these occur.Unlike the other types of credit enhancements, where cash flows appear only in a credit event occurrence (i.e., default), in credit derivatives a steady cash flow of the premium, paid to the protection seller, must be considered and counted as an expense. Moreover, credit events, including defaults, upgrades and downgrades, also cause changes in the market pricing which result in downstream gains or losses in a mark-to-market2 accounting regime.

As mentioned above, there are several credit derivatives in the market. The type(s) of the underlying instruments, the status of the counterparties and the definition of the credit events may increase the complexity in regard to the analysis. Financial institutions are always inventing and structuring new credit derivatives for insuring their credit portfolios and mitigating financial risks. We all know by now how investment banks use this reasoning when packaging subprime loans, turning them into AAA-rated investments. We may witness history repeating itself, right in front of our eyes, with structured portfolios of loans issued from the marketplace lending environment.

10.3.3 Lack of credit enhancements in marketplace lending exposures

The world of marketplace lending is devoid of credit enhancements, such as collateral, that may shield investors against counterparty risk and credit losses. Marketplace lenders have stripped away those processes that make bank lending tedious and hard to comply with. Currently, marketplace lending platforms have very nimble operations and are hardly in a position to assess and accept collateral for their loans. For this reason, loans originated on marketplace lending platforms are entirely uncollateralized. When lenders diversify across several loans3 the lack of collateral may not result in large losses in a loan portfolio. At the same time, if marketplace lenders wish to play in the big league with banks, they need to graduate into the realm of real estate credit. This will require a rethink of their business model and practices. When they have to assess collateral, this will most definitely result in larger overheads, and regulatory requirements for compliance. At this point, marketplace lenders become more like banks. It is uncertain how their loan origination will change when they make the jump.

10.4