Banker's acceptances

A banker's acceptance, also known as an acceptance credit, is a time draft, which is a document stating the signatory will pay an amount at a future date, say in 90 days. Say, for example, that an importer buys goods from an exporter with an agreement to pay in three months.

Instead of sending the bill to the importer, the exporter is instructed to send the document, which states that the signatory will pay a sum of money, at a set date in the future, to the importer's bank. This is ‘accepted' by the importer's bank rather than by a customer. Simultaneously the importer makes a commitment to pay the accepting bank the relevant sum at the maturity date of the bill.The exporter does not have to wait three months to receive cash despite the importer's bank not paying out for 90 days. This is because it is possible to sell this right to investors in the discount market long before the three months are up. This bank commitment to pay the holder of the banker's acceptance allows it to be sold with more credibility in the money markets to, say, another bank (a discounter) by the exporter after receiving it from an importing company's bank. So, say, the acceptance states that ˆ1 million will be paid to the holder on 1 August. It could be sold to an investor (perhaps another bank) in the discount market for ˆ980,000 on 15 June. The importer is obliged to reimburse the bank ˆ1 million (and pay fees) on 1 August; on that date the purchaser of the acceptance credit collects ˆ1 million from the bank that signed the acceptance, making a ˆ20,000 return over six weeks.

While banker's acceptances are similar to bills of exchange between a seller and a buyer, they have the advantage that the organisation promising to pay is a reputable bank representing a lower credit risk to any subsequent discounter, thus they normally attract finer discount rates than bills of exchange.

The holder of the instrument has two guarantors: the importer and the bank. It also has the collateral of the goods underlying the trade.Not all banker's acceptances relate to overseas trade. Many are simply a way of raising money for a firm. The company in need of finance may ask its bank to create a banker's acceptance and hand it over. Then the company can sell it in the discount market at a time when it needs to raise some cash. They are very useful for companies expanding into new markets where their name is not known and therefore their creditworthiness is also unknown; they can take advantage of the superior creditworthiness of the bank issuing the acceptance, which guarantees that payment will be made.

There are three costs involved:

1 The bank charges acceptance commission for adding its name to the acceptance.

2 The difference between the face value of the acceptance and the discount price, which is the effective interest rate.

3 Dealers take a small cut as they connect firms that want to sell with companies that wish to invest in banker's acceptances.

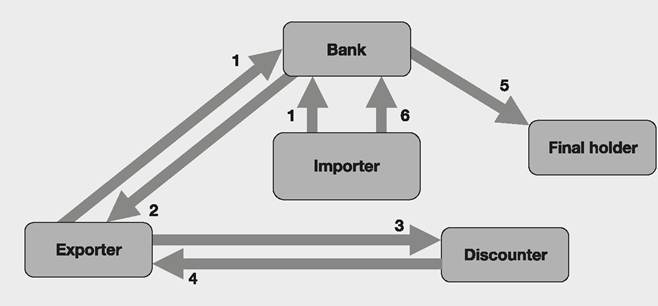

These costs are relatively low compared with overdraft costs. However, this facility is available only in hundreds of thousands of pounds, euros, etc. and then only to the most creditworthy of companies. Figure 11.2 summarises the acceptance credit sequence for an export deal.

1 Banker's acceptance drafted and sent by an exporting company (or its bank) demanding payment for goods sent to an importer's bank. Importer makes arrangements with its bank to help it. Acceptance commission paid to the bank by importer.

2 The bank accepts the promise to pay a sum at a stated future date.

3 The banker's acceptance may be sold by the exporter at a discount.

4 The discounter pays cash for the banker's acceptance.

5 The bank pays the final holder of the banker's acceptance the due sum.

6 The importer pays to the bank the banker's acceptance due sum.

Figure 11.2 Banker's acceptance sequence - for an export deal

Example 11.2

The use of a banker's acceptance

A Dutch company buys ˆ3.5 million of goods from a firm in Japan; it promises to pay for the goods in 60 days' time.

The Dutch company asks its bank to accept the banker's acceptance. Once the bank has stamped ‘accepted' on the document, it becomes a negotiable (sellable) instrument. The exporter receives the banker's acceptance. After 15 days, the Japanese company decides it needs some extra short-term finance and sells the acceptance at a discount of 0.60%, receiving ˆ3,479,000. The exporter has been paid by banker's acceptance immediately the goods have been despatched. It can also shield itself from the risk of exchange rates shifting over the next 60 days by discounting the acceptance immediately, receiving euros and then converting these to yen. And, of course, the exporter is not exposed to the credit risk of the importer because it has the guarantee from the importer's bank.Case study

HSBC Canada's banker's acceptance service

HSBC Canada advertises banker's acceptances (BAs) as a good way of raising money for businesses. Here is a page from its website:

Banker’s acceptances (BAs)

Available in Canadian and US dollars, banker's acceptances (BAs) are an excellent alternative to traditional short-term borrowing or commercial paper.

BAs may provide your business with a lower cost borrowing alternative

A BA is an unconditional non-interest bearing note that is issued by a borrowing company

On acceptance of the BA, HSBC assumes an irrevocable liability for the borrower's debt

BAs are typically more negotiable and reduce your borrowing costs

BAs are typically issued:

• At a discount to face value

In bearer form

• With flexible maturity dates to a maximum of 1 year

• From 30 to 90 days

Source: HSBC Canada website www.hsbc.ca/1/2/business/business-banking/finance/bankers-acceptance