Bond equivalent yield (bey) and discount (d) yield compared

Any investor/issuer needs to be able to compare returns with other investments and so it is important that they understand the figures and the basis on which they are calculated, and that they are able to work out the bond equivalent yield (bey).

The bond equivalent yield (also known as equivalent bond yield) is the yield that is usually quoted in newspapers and it allows a comparison between fixed-income securities whose payments are not annual and securities that have annual yields. So a wide variety of debt instrument yields is expressed in the same annual terms, whether they mature in a matter of days, have interest paid every three months or have one yearly interest payment. The bey uses the actual number of days in a year (365 or 366).

Example 14.1

Bond equivalent rate

Imagine a 12-month £100 UK Treasury bill was sold at a discount of 2%, i.e. at £98, the purchase price or market price. We recognise that the investment made is £98 and we gain £2 when it is redeemed in one year. Thus we know that the true rate of return is slightly over 2%.

To be more accurate we calculate the bey:

Given that there is a full year to maturity we know this is going to be the annual rate:

So although the bill was discounted at 2%, the actual return is more than this because the investor did not pay the face value.

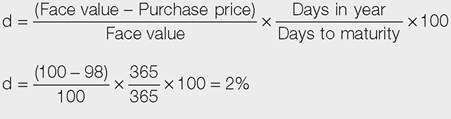

The discount yiel (bank-discount basis or discount rate) is the yield when using the face value as the base rather than the actual amount invested by the buyer. Discount yields are often calculated using a 360-day year count convention (e.g. in US, German, Dutch, French and Italian T-bills), but the UK uses a 365-day year in its calculations.

To calculate the discount yield:

Example 14.2

Discount yield

For a UK T-bill issued at £98 when the face value is £100 and the time to maturity is one year, when there are 365-days in the year: