CHAPTER SEVEN The Businessmen’s War to End All Fraud

On hot mornings in the summer of 1933, the residents of Dallas, Texas, could count on a daily radio bulletin, Sundays excepted. This report did not ruminate about bleak chances for rain nor offer the latest intelligence from swooning cotton markets.

It provided no details about upcoming church socials, no listings of used goods for sale, no chronicle of New Deal political maneuverings in Austin or Washington, DC. Instead, it furnished commentary and counsel about commercial tales so tall that they crossed the line of acceptable economic behavior. The shady pitches included local offers of “Free Lots” that came with a big catch, a “Business Stimulator” method that its promoter guaranteed would bring orders to struggling firms, and a sham employment scheme.1 The inclusion of a fraud report in the Dallas radio lineup was not an idiosyncratic decision by a lone station manager desperate to fill airtime. Similar segments occurred on radio stations across the nation in the 1920s and 1930s, all courtesy of officials working for local Better Business Bureaus (BBBs), nonprofit organizations dedicated to exposing commercial flimflam and providing consumer and investor education.In the first decades of the twentieth century, business fraud became more sophisticated and extensive, mirroring the growth of truly large-scale enterprise. By the 1920s, American marketers had become sufficiently familiar with the psychology underpinning popular consumption and investment to craft emotive sales pitches that played on modern enticements and anxieties, further complicating the question of what counted as deceptive commercial speech. The resulting advertisements included images of soap that somehow anointed its users with sex appeal, depictions of mouthwash that ostensibly functioned as a talisman against halitosis, and visions of fractional shares in oil wells that would magically transport their owners into the ranks of the wealthy.2

Amid this vexing economic environment, Americans increasingly identified prevailing antifraud regulations as insufficient to the tasks at hand.

The most influential early twentieth-century reformers came from a key segment within the country’s business elites, who crafted a far-reaching plan to combat economic duplicity. Concerned about the impact that swindles and misrepresentations were having on commercial culture and economic growth, scores of executives within advertising, marketing, and finance collectively mounted a full-scale campaign against business frauds. Cementing an alliance with the national Republican Party, antifraud reformers created several nonprofit organizations to combat the procurement of credit through provision of fabricated financial information, fraudulent bankruptcy, the sale of spurious medical treatments, false advertising and other deceptive marketing practices, and securities swindles.This chapter probes the business establishment’s diagnosis of the “fraud problem” and its chief remedies for it—campaigns of public education, such as the Dallas radio spots, legal reforms that more carefully defined the requirements of truthfulness in commercial speech, and private policing of those limits, all overseen by novel nonprofit organizations that had close ties to the corporate world, the Better Business Bureaus chief among them. Closely connected to state authorities, these organizations opened up new fronts in America’s ongoing struggles with business fraud. As they did so, they further blurred the lines between public and private regulation.

The early twentieth-century crusade against fraud suggests the need for more refined understandings of how the era’s business elites viewed economic governance. In the broad arena of commercial speech, most of those elites did not want government to remain on the sidelines, nor preferred that the state focus only on industry standard-setting, nor placed their faith in co-optable administrative agencies. Rather, business leaders prodded public servants at all levels to sharpen statutory prohibitions against misleading commercial communication and to beef up criminal enforcement of those measures, though with a big helping hand from the new nongovernmental institutions dedicated to the fight against deception in the marketplace.

Here was a particularly vigorous effort to create “associationalism”—a mode of government-business relations in which the state facilitated substantial intra-industry, and even interindustry, cooperation, with the goal of stabilizing market conditions and solving other socioeconomic problems.3The businessmen’s fight against commercial duplicity further points to the enduring strengths and weaknesses of business self-regulation as a mode of governance. Antifraud organizations quickly developed effective administrative capacity, at least some bureaucratic autonomy, and considerable goodwill among business owners and managers. These assets constituted the hard-won fruits of a social movement of sorts within America’s commercial classes, and they enabled the movement’s leaders to design and carry out a comprehensive strategy to attack commercial misrepresentation. As a result, the campaigns for truthful commercial speech often successfully challenged longstanding entrepreneurial practices that privileged secrecy and promoted narrow short-term economic calculation, thereby fostering more transparent communication between buyers and sellers in many markets. At the same time, key participants in those campaigns often manifested an ethnocentrism that targeted immigrants and flirted with the rhetoric of eugenics. Close relations between dominant corporations and key figures in the antifraud movement, moreover, compromised those leaders' collective vision, encouraging them to ignore some of the era's most serious instances of economic deceit. This episode thus underscores both the allure and the dangers of vesting authority in private regulators, especially when they retain attachments to business elites.

A Cadre of Professional Fraud-Fighters

From William McKinley's election in 1896 to Herbert Hoover's defeat in 1932, Americans confronted recurring assessments that fraudulent behavior pervaded their society. Although such evaluations had ample precedents, the early twentieth-century discourse on commercial fraud conceptualized the problem differently.

Observers now considered the impact of duplicity on a more clearly defined national economy, imagining and even calculating its systemic costs. By the 1920s, government agencies and business organizations placed impressive dollar figures on the price tag imposed by fraud. Credit scams ostensibly amounted to between $250 million and $400 million per year. Insurance swindles reportedly bilked companies out of at least a billion dollars annually, while securities fraud allegedly removed at least that amount from ordinary Americans, and possibly twice that. Estimates of total annual costs from organizational fraud, which also included consumer frauds and real-estate swindles, typically topped three to four billion dollars, a figure that, if accurate, equaled roughly 1 percent of the US gross domestic product. Although the factual basis for these estimates was murky, they passed into conventional wisdom, repeated in editorials, news reports, and cartoons, as with a 1927 depiction of the credulous suckers who bit at fraudulent stock pitches (Figure 7.1).4Newspaper coverage and periodical exposes further made clear that American perpetrators of fraud methodically developed more refined schemes of social mimicry. In the nineteenth century, credit fraud occurred with some frequency but typically represented a one-off response to looming insolvency. By the late 1890s, nationwide rings of “credit trimmers” had emerged, which sought repeatedly to bamboozle manufacturers and wholesalers who sold wares on the basis of unsecured trade credit. These rings first established members of the conspiracy as independent retailers, either by providing falsified

Figure 7.1: The popularization of fraud cost estimates in the 1920s. Reprinted from Commerce, Finance, and Industry, May 1927, courtesy of the Los Angeles Times.

references, buying out existing businesses, or launching stores with names similar to those of well-regarded firms with solid credit.

Once these front enterprises cajoled distant manufacturers or wholesalers to furnish them with substantial inventories, the rings would spirit the goods away for sale by confederates elsewhere. Indebted retailers then either disappeared or falsely declared bankruptcy before moving on to new towns, taking on new commercial identities, and beginning the scheme anew.5Securities fraud similarly came to require significant capital and organizational capacity. As early as 1910, the most effective peddlers of dodgy stocks published financial newsletters and dailies that offered conventional assessments of the securities markets, but also relentlessly puffed selected issues controlled by the promoters who owned the tip sheets. Relying on ever more finely tuned compilations of sucker lists, which concentrated on individuals who had previously fallen for securities scams, fraudulent promoters employed crews of clerical workers to distribute their newsletters and other promotional materials to tens of thousands of potential investors. They also oversaw teams of high-pressure salesmen who either operated out of boiler rooms or through revivalist-style investment meetings and tours. The latter proved especially common in the sale of oil stocks and real-estate investments. In some cases, large-scale stock swindlers even created or gained control over regional stock exchanges, such as the Boston Curb Exchange, to facilitate the market manipulations that persuaded investors that individual stocks were in the early stages of a boom.6

The most expansive flotations of sham companies went to great lengths to convey their bounteous prospects. No self-respecting swindler would attempt to cash in on an oil boom without setting up shop in close proximity to known gushers and constructing impressive-looking derricks and storage tanks. A few of the more enterprising operators “salted” a creek by infusing it with petroleum from buried barrels.7 Fraudulent promoters in the early automobile industry, such as the Pan Motor Company of Minneapolis, employed even more expensive attention to theatrical optics.

Pan Motor's promoters built a mammoth factory and a handful of cars, all to impress visiting journalists and the recipients of the firm's photograph-laden prospectuses.8To business leaders, legal thinkers, and prominent financial journalists, the all-too-rapid evolution of American swindling posed dangers beyond the most direct financial costs to consumers, investors, wholesalers, and insurers. The sap who invested in a fraudulent automobile company withdrew assets from a legitimate savings bank and did not invest in reputable enterprises, thereby increasing the latter's costs of capital. The dupe who purchased worthless items from a fly-by-night mail-order concern or who responded to the deceptive advertising of a local piano store reduced the profits of law-abiding retailers. Through sales of stolen goods, the credit fraud ring brought losses to legitimate retailers and higher overhead costs to defrauded suppliers. At the same time, successful deceptions set dangerous examples for the legions of American young men on the make, who “learn[ed] to think that there is a better way of getting money than by earning it” and who focused on “making plenty of money and keeping out of jail.”9

Perhaps the greatest threat posed by fraud concerned the public faith in America's most important marketplaces, or, as one leading spokesman for the business world put it, “the capital of confidence upon which all progress depends.” When department stores touted discounts on goods that turned out to be unavailable, marketing executives fretted that such bait and switch schemes fed public skepticism about advertising in general. Opinion-makers within fi-

nance worried that duplicitous marketing of stocks and bonds would spawn “sectional prejudice against ‘money centres,’ ” perhaps even “bitter and unreasoning suspicion” of all securities, leading potential small investors to “thrust many a dollar down deeper in the sock.” By the 1920s, Wall Street had become more reliant on investing by ordinary Americans, needing infusions of capital from the socks (and savings accounts) of wage- and salary-earners.10

Some observers of the economic scene even expressed the fear that deceptive practices ran the risk of souring ordinary Americans on capitalism altogether. In February 1919, during a severe wave of securities swindles that targeted individuals with modest financial resources, witnesses at a federal government hearing depicted such crimes as “a prime cause of social unrest.” Amid the early years of the Russian Revolution and a postwar period of intense labor conflict, as well as unprecedented political success by the American Socialist Party, business elites feared that the pervasive experience of becoming a sucker created political openings for radicals. The danger was only sharpened by the tendency of fraudulent stock promoters to levy sharp public attacks on the power of industrial corporations and New York City investment banks. As the headline writers at the New York Times framed the possibility, “Stock Frauds Seen as Spur to Bolshevism.”11

One might question how much the specter of unbridled swindling threatened to turn large numbers of post-World War I Americans toward the Leninist banner. But leading capitalists became sufficiently anxious about the issue of deceptive commercial speech to create a series of nonprofit business organizations between the mid-1890s and the early 1920s, all primarily dedicated to rooting out fraud in the American marketplace. In 1896, the executives responsible for credit extension by manufacturers and large wholesalers founded a new professional organization, the National Association of Credit Men (NACM), which sought to reduce credit fraud. Roughly a decade and a half later, a group of prominent advertising executives joined forces through the Associated Advertising Clubs of the World to create a “truth in advertising” movement, which emerged out of a series of local “vigilance committees” organized by urban advertising associations. Within a few years, the Investment Bankers of America had instituted an analogous committee focused on the challenges of securities fraud, followed by the New York Stock Exchange’s (NYSE) creation of the Business Men’s Anti-Stock Swindling League. In the early 1920s, these institutional responses to deceptive merchandising and investment-peddling merged into a nationwide network of metropolitan Better Business Bureaus (BBBs), coordinated by a National Better Business Bureau (NBBB).12

All of these initiatives predated the “second wave” consumer movement, which was triggered by the seminal muckraking exposes It’s Your Money (1927), 100,000,000 Guinea Pigs (1933), and Skin Deep (1934), and given real momentum by the creation of independent advocacy groups such as Consumer Research (1929) and the Consumers Union (1936). Consumer activists eventually launched withering attacks on mainstream advertising practices, which intensified the inclination among business leaders to bolster confidence in advertising through mechanisms of self-regulation. But such critiques came too late to motivate the initial movement to foster greater honesty in marketing.13

There were abundant precedents for American business organizations to tackle the problem of economic deceit. One important touchstone involved the stock and commodities markets, an important sponsor of several new antifraud groups. Since the 1870s, the nation's leading stock and commodity exchanges had maintained internal rules against “obvious fraud,” whether attempted against other exchange members or outside customers.14 As memoirs and exposes by participants in the financial markets attest, such prohibitions did little to protect investors from gross manipulations by insiders.15 But especially egregious duplicity, such as appropriating a client's funds or adulterating already-inspected loads of grain, did occasionally lead exchanges to expel members.16 Urban chambers of commerce also sought to curtail misrepresentations in trade or investments, as with the creation of arbitration boards by several Southern chambers to address allegations of fraudulently packed cotton. Many of these rule-making and disciplinary bodies had short lifespans, however, and almost all of them were limited to oversight of firms that belonged to parent organizations.17 By contrast, the NACM, BBBs, and American Medical Association (AMA), which began to target quackery and medical swindles in the early twentieth century, embraced much more ambitious goals. These organizations wished to combat duplicitous commercial practices throughout the economy, among member and nonmember firms alike.

Funded through annual subscriptions, mostly by large corporations, the new antifraud institutions soon came under the direction of individuals who built careers on the work of curbing commercial deception. J. Harry Tregoe and H. J. Kenner illustrate this pattern. Tregoe initially worked in banking and as the credit manager for a Baltimore shoe company, jobs that exposed him to the costs resulting from dishonest debtors. In the three decades after helping to found NACM in the 1890s, he served the organization as president, executive secretary, general manager, and editor of its primary publication.18 Kenner spent his early career as a North Dakota retailer, serving as an officer for a local mercantile association. In 1914, at the age of twenty-six, he was tapped by Minneapolis ad executives to direct their new vigilance organization, making him the first person to receive a salary for such work. After a year of regional travel preaching the gospel of truthful advertising, he took a job with the National Vigilance Committee (NVC), an early coordinator of local groups. In the early 1920s, he moved to New York City to head its new BBB, which he proceeded to manage for the next quarter-century.19

Constructing a vision of fraud prevention as a calling, Tregoe, Kenner, and their fellow antifraud specialists arrived at similar conclusions about commercial fraud’s origins, as well as the most effective means of addressing it. Their sensibilities reflected the era’s pervasive embrace of professionalization. Like so many other highly educated economic and cultural brokers, ranging from industrial engineers, accountants, and personnel managers to social workers and public-health officials, antifraud careerists claimed that expertise and commitment to the common good prepared them to tackle the problems created by rapid economic and social change.20

Like other early twentieth-century experts, the band of nascent antifraud professionals began with systematic analysis of causes before constructing programs of action. In doing so, they echoed many arguments common within the previous century’s commentary about business fraud, while more deeply probing the relationships among deceptive marketing practices, socioeconomic structures, and social norms. Swindling flourished in modern America in part, they reasoned, because the growth unleashed by industrialization had put savings and disposable income in the hands of unsophisticated consumers and investors. These neophytes struggled to navigate the informational challenges of a modern economy, and they often chased after the latest consumer goods or investment fads on the basis of cursory investigation. Whether unscrupulous retailers tried to attract customers to mail-order offerings or retail stores, their beguiling ads zeroed in on the allure of the bargain. Financial hucksters similarly took advantage of pervasive aspirations for affluence in a society that lionized Horatio Alger figures but had narrowed paths to independent proprietorship. Focusing on the latest technological wonders or booms in oil, mining, or real estate, these promoters pitched penny stocks to “the discontented janitress and the ambitious elevator boy,” to the salaried clerks and struggling professionals “who are obsessed by an easy road to wealth.”21

Antifraud professionals stressed that the financing of America’s participation in World War I accelerated this process, as the mass marketing of Liberty Bonds acculturated millions of wage- and salary-earners to the securities markets. From the first days of peace, swindlers sent brigades of “chipper salesmen” to go “from door-to-door in city and farming communities, enticing Liberty Bonds from hiding and giving in return lithographed certificates bearing marvelous artists’ dreams of derrick after derrick, gusher after gusher, spreading as far as the eye can see.” Yet credulity and situational ignorance, antifraud organizations argued, extended far beyond those Americans who were less accustomed to the ways and wiles of twentieth-century capitalism. In bulletins and annual reports, the BBBs continually marveled at “the gullibility of the business public,” who were frequently burned by the pitchmen for sham collection agencies and fake commercial directories. NACM officials constantly harped on the susceptibility of so many suppliers to fraudulent requests for credit. Even the New York Stock Exchange had to caution its employees against their propensity for playing the sucker, biting at some spurious “inside” tip or seeking to ride a wave of public fascination with a worthless stock, hoping to get out at the top.22

Antifraud crusaders further emphasized that prevailing legal prohibitions against duplicitous commercial speech posed only slight risks to swindlers. Institutional and cultural dynamics that had stymied nineteenth-century fraud prosecutions continued to shape the criminal justice system. The ethos of caveat emptor retained a strong allure among many early twentieth-century Americans, who still prized individualism, identified citizenship with the ability to look after their own affairs, and viewed governmental paternalism with abiding skepticism. As a result, con artists frequently received “admiration” for their “cleverness and dexterity,” as in George Randolph Chester's best-selling novels about “Get-Rich-Quick Wallingford.” Swindlers operating petty mailorder scams sometimes mocked the individuals who fell for their pitches, explicitly informing them that they had been taken for a ride and suggesting that they had received something of value for their money—a bit of experience that would wise them up for the next commercial go-round. Given these widely held social norms, a swindler's victim might be more likely to experience psychological denial (especially in the case of investments gone awry or medical treatments that proved worthless) or keep quiet to avoid the embarrassment of “advertising] the fact that he had permitted a ‘slicker' to best him.”23

When individuals nonetheless did complain to the authorities about instances of alleged swindling, successful prosecutions proved to be the exception rather than the rule, for much the same reasons as during the 1840s or the 1880s. Early twentieth-century fraud cases often turned on complex factual questions about the nature of misrepresentation and the evidence showing fraudulent intent. As a result, convictions depended on investigatory and prosecutorial expertise, which was often in short supply at every level of government. Moreover, in the rare circumstances in which authorities charged individuals with fraud, prosecutors all too often found themselves outgunned by high-priced defense attorneys, while juries frequently protected local businessmen whose deceit attracted outside capital into their communities. In the even rarer instances in which fraud prosecutions culminated in convictions, the judiciary almost always handed out fairly minimal sentences—either modest fines or relatively short jail stints. If convicted swindlers possessed good political connections, as they often did, even those slight penalties could be wiped away by pardons. As one early twentieth-century legal expert observed, the perpetrator of credit fraud “may be punished with no greater severity than the man who expectorates on the floor of a public conveyance.” The result, critics complained, was that fraud enforcement still only slightly increased most swindlers’ requirements of working capital, essentially imposing a “license fee”24

Antifraud organizations identified one further contributor to widespread economic duplicity: the tendency of business owners to respond to short-term incentives, without regard to the long-term implications of their actions for broader commercial culture and public confidence. In this regard, the early twentieth-century analysis of fraud incorporated a more sophisticated appreciation for economic sociology than was present in prior discourse about commercial deceit. Especially within NACM, activists observed that the pressures of competition encouraged far too many wholesalers to extend commercial credit without sufficient investigation, making them likely candidates for credit fraud. Analogous pressures pushed far too many retailers and promoters to flirt with deceptive advertising, and far too many newspapers and magazines to accept such ads. When business owners were taken in by scams, they often proved willing to accept compromise settlements from a swindler’s “squawk fund,” securing their own financial interests rather than insisting upon criminal prosecutions that would improve the deterrent value of fraud laws.25

These diagnoses guided NACM and the BBBs as they developed strategies to protect American markets from duplicitous commercial speech. In their early years, antifraud organizations focused particularly on lobbying state and federal governments to tighten legal prohibitions against deceptive economic conduct. Thus NACM’s central purpose during the 1890s was to agitate for a new federal bankruptcy law that its leaders hoped would curb fraudulent conveyances and the concealment of assets by failing debtors, an endeavor that yielded legislative success in 1898. In addition to calling for periodic amendments to the federal bankruptcy code, NACM moved on to press for uniform state laws that would criminalize two common tactics of credit fraud schemes— the signing of a false financial statement in order to obtain credit and the selling of retail inventory in bulk without furnishing notice to commercial creditors. By the same token, the Associated Advertising Clubs of the World (AACW) concentrated much of its initial energy on pushing a model state statute to punish false advertising claims. Spearheaded by the advertising journal Printer’s Ink, this campaign led to the passage of statutes in forty-three states by 1930. Throughout the 1920s, moreover, the Investment Bankers Association, the NYSE, and the BBBs all worked for the adoption of state securities laws that would facilitate prosecutions of fraudulent stock promoters.26

At the national level, antifraud organizations also pressed the new Federal Trade Commission (FTC) to interpret its jurisdiction as including the authority to combat duplicitous business practices. The chief impetus behind the commission’s 1914 creation lay with worries about the waxing power of monopolies and trusts, as well as more specific frustrations with a series of Supreme Court opinions, including the 1911 decision in the Standard Oil case, that narrowed the reach of the Sherman Anti-Trust Act and fostered uncertainty about which anticompetitive strategies the courts would view as illegal. Section 5 of the FTC Act, however, also empowered the new agency to investigate “unfair methods of competition,” language that at least some members of Congress assumed would encompass misleading or untrue marketing claims. These members of the antitrust coalition viewed the emergence of concentrated corporate power as at least partly the result of pervasive deceptions and frauds committed by aggrandizing monopolists.27

Almost immediately after the passage of the FTC Act, the AACW’s National Vigilance Committee (the precursor to the National BBB) lobbied the new commission to tackle cases involving false advertising, sending it a series of formal complaints. Stymied by the federal courts in many of its attempts to regulate industrial structure, but allowed in most cases to proceed against duplicitous business tactics, FTC lawyers gradually made deception cases a central element of their docket. By the mid-1920s, they brought several hundred such cases a year, involving misrepresentations of product quality, quantity, newness, or origin, or falsehoods about business status, supposed testimonials, or fictitious price cuts. By the end of the decade, nine of ten docketed cases were of this type.28

In addition to these efforts to expand the ambit of antideception policies, antifraud organizations embarked on massive public education campaigns. If a pivotal explanation for pervasive fraud lay with insufficient skepticism and savvy among ordinary Americans, then surely any sensible attempt to prevent fraud had to teach those people how to resist the siren song of the swindler. As one financial journalist with years of experience covering fraud argued in 1919, the most sophisticated antiswindling statutes could not “safeguard people from their own foolishness, and in the last analysis, education in these matters is the individual’s best and surest protection.”29

The BBB network pursued that goal with a vengeance. During the 1920s the antifraud publicity blitz was impossible to avoid in urban America. From Los Angeles to Atlanta to Boston, industrial workers encountered a rotating stream of posters on factory bulletin boards and educational articles in company mag-

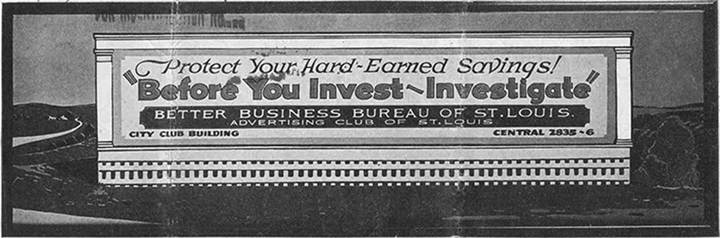

Figure 7.2: A typical BBB billboard, St. Louis, 1926. From St. Louis Better Business Bureau, Telling the Public, courtesy of NACM.

azines. BBB messages bombarded commuters on buses, trains, subways, and streetcars, while its billboards repeated key slogans for the benefit of automobile drivers and passengers. Individuals who visited banks to make deposits or withdrawals found BBB advice cards tucked into their account books. Newsletters and bulletins from local Bureaus filled the nation’s mailbags, mirroring the prodigious output of swindling stock tip sheets and fraudulent mail-order catalogues. As the pitchmen of worthless stocks and boom-related real-estate ventures turned to revival-style sales lectures, BBB officials countered with hundreds of annual speeches to women’s clubs, business groups, labor organizations, and civic associations. Thousands of newspapers, magazines, and trade publications donated advertising space to the “truth in advertising” movement and ran articles written by BBB leaders. Once radio stations gained a commercial footing, they quickly followed suit, offering free access to the airwaves for short spots and longer segments.30

One can get a more concrete sense of this publicity onslaught by considering its scale in the city of St. Louis. In 1926, the local BBB claimed that each month it placed the equivalent of thirty-eight full newspaper pages of free commentary in fifty-one different papers, which included three major metropolitan dailies, the local African American paper, twelve foreign-language publications, and a host of suburban weeklies. Together, these sheets counted over 290,000 subscribers. Thousands of free ads in trade journals, labor sheets, company magazines, and religious newspapers amplified the message, as did a slew of billboards (such as the one in Figure 7.2) and neon signs, over one hundred talks by BBB officials to community groups, free movie announcements and placements in theatre programs, and regular radio chats by representatives of the Women’s Advertising Club. Finally, through close relationships with newspaper editors and the managers of the St. Louis News Service,

BBB officials ensured that their work received ongoing coverage in regional news outlets.31

These media blitzes mirrored the strategic approaches of nineteenthcentury publications that regularly exposed frauds and humbugs. Like those earlier sentinels, twentieth-century organizations broadcast specific cautions about prevailing scams and misrepresentations, warning the public to avoid specific stores, investments, business deals, and promoters. The BBBs also disseminated general advice about how to invest and consume wisely, emphasizing the crucial importance of eschewing retailers who offered supposedly first- rate goods at enormous discounts, promoters who dangled visions of easily attained wealth, or anyone who made a big show of offering something for nothing. Above all else, antifraud campaigners pleaded with the public to rely wherever possible on expert assistance, particularly when selecting investments. “Before you invest, investigate,” became the BBB’s best known mantra, by which its officials meant that Americans should have the good sense to follow the advice of respectable bankers or brokerage firms in deciding where to place their savings.32

An analogous logic underpinned more focused endeavors to reshape America’s commercial culture. Here, antifraud activists again broke new conceptual and strategic ground. Because entrenched business practices aided and abetted those who perpetrated scams, antifraud organizations also tried to persuade firms to reject such practices. NACM leaders continuously advocated the adoption of credit policies that accorded with its view of the shared long-term interests of all wholesalers and manufacturers. At its annual conventions and through its monthly publication, the association’s leaders called for more sustained scrutiny of credit requests and greater willingness to exchange intelligence about the creditworthiness of retailers, including the creation of cooperative credit bureaus that would provide more up-to-date information than did standard credit-reporting firms. With regard to merchandising, the BBB network pressured newspapers and periodicals to reject advertisements that did not meet strict standards for candor, and eventually helped to organize a series of trade conferences in order to adopt unambiguous standards for the categorization of materials such as furs, textiles, and woods.33

The Imperative of Organized Vigilance

For all the faith that early twentieth-century antifraud reformers placed in reconfigured statute books and educational campaigns, they also viewed the parlous state of law enforcement as requiring urgent attention. By the early 1900s, the NACM had set up local investigating committees composed of volunteer credit men to examine instances of questionable behavior by debtors, and passed along evidence of credit fraud to relevant authorities. Beginning in the 1910s, advertising clubs created similar mechanisms to look into allegations of false advertising, deceptive merchandising, and fraudulent securities promotions. “Putting swindlers in jail for what they have done,” the president of the NYSE explained in a 1922 speech, “will give far more protection to the public than a hundred laws warning criminals of what they may not do”34

These moves into private law enforcement, like the efforts to create clearinghouses for news about prevailing swindles and scams, built on longstanding American traditions. In addition to the periodic turn to organized vigilantism in places as varied as northern Indiana, central Texas, Montana, San Francisco, and throughout the South, nineteenth-century Americans frequently turned to nongovernmental associations in order to supplement government policing, in many cases with explicit sanction from state legislatures. The anti-horse thief associations in late nineteenth-century America stood as examples of this impulse, as did banks’ anticounterfeiting associations and, later, antivice societies such as the New York Society for the Suppression of Vice and the New England Watch and Ward Society, which played such a central role in the Post Office’s campaigns against mail fraud and obscenity. Typically, such initiatives came from elite and middle-class Americans who embraced the use of law to constrain what they saw as socially or economically dangerous expressions of individual license, but who despaired of the government’s capacity to enforce law on its own, either because of endemic corruption or lack of capacity. These self-appointed enforcers also wished to retain influence over the investigative and prosecutorial process.35

In the years surrounding World War I, corporations in several industries that confronted serious crime problems updated this strategy, as did a number of new voluntary agencies concerned about working-class family dynamics or a perceived rise in urban lawbreaking. Within the business world, railroad corporations established a detective bureau to break up freight thefts by rings of insiders. Fire insurance companies did the same to investigate arson gangs, guarantee companies to look into cases of embezzlement, and department stores to combat shoplifting. At roughly the same time, middle-class reformers were creating nationwide “desertion bureaus” to track down husbands who had abandoned their families, as well as local groups such as the Chicago Juvenile Protection Association. The latter organization sought to reshape the rules governing the treatment of adolescent criminal offenders and to provide a battalion of social workers who could take psychological profiles of defendants and monitor convicted teens on probation, thereby magnifying the disciplinary capacity of urban courts.36

As occurred with most of the era's enforcement campaigns by nongovernmental groups, antifraud organizations experienced a steady process of expansion and professionalization. The early volunteer committees soon found themselves overwhelmed by complaints, mostly from affected businesses, but also from disgruntled members of the general public. They responded to a crippling workload by lobbying successfully for the creation of independent organizations with salaried staffs, all funded by subscriptions, primarily from big business. After years of debate over issues of practicality and institutional control, NACM supplemented its local vigilance groups in 1916 with a national committee, for which it raised $25,000. By 1926, the newly renamed Investigation and Prosecution Department boasted a multiyear Prosecution Fund of nearly two million dollars—an equivalent share of American GDP in 2016 would be around $330 million—regional offices throughout the country, and a corps of forty experienced investigators who could draw on the services of local credit men's associations in more than forty states. This unit pursued as many 750 investigations annually and referred hundreds of cases to state and federal prosecutors, with most resulting in indictments and convictions. The local and national BBB network, though starting later than the NACM, also built hefty administrative capacity. In 1916, the AACW's National Vigilance Committee, the direct forerunner of the National BBB, ran on a shoestring budget of $15,000 and had two employees, while many local Bureaus still operated primarily on a voluntary basis. By the mid-1920s, total annual expenditures by all the BBBs approached $1 million (roughly equal to $165 million as a share of 2016 GDP), as forty-t hree local bureaus, spread across nineteen states, handled tens of thousands of complaints about securities fraud, catchpenny scams, and misleading or false advertising. Most also maintained “shopping systems” to monitor retail establishments in their communities, sending out paid female shoppers in order to assess the extent to which department stores and other retailers lived up to advertised promises and followed ethical sales practices.37 These multifaceted initiatives dwarfed the endeavors of the late nineteenth-century editors who carved out a role as arbiters of legitimate mail-order enterprise.

BBB spokespersons such as Boston department store executive Louis Kir- stein emphasized that scrutiny by independent shoppers served as a salutary check on retail marketing campaigns. These evaluations, Kirstein stressed, offered a means of correcting inevitable mistakes and demonstrated to smaller competitors that the BBB commercial standards applied to all sellers in the urban marketplace. The mechanics of the shopping systems, however, suggest that they additionally sought to police the behavior of a growing retail workforce, including not only in-house advertising staff, but also buyers and sales personnel. In Boston, for example, the form that Bureau shoppers had to fill out included numerous questions about the deportment and level of service provided by salespersons, as well as the queries, “Did representations of S. P. [salesperson] agree with representations in advertisement?” and “Did S. P. misrepresent merchandise?” Employees of large-scale retailers often received commissions as an element of their compensation, and so had strong incentives to move merchandise, even if their characterizations of goods or other sales tactics violated store policies. The shopping system thus furnished a means of keeping store workers from ignoring dictates about the treatment of customers, compensating for imperfect lines of authority. As such, it constituted a companion mechanism to the pervasive reliance on store detectives, whom managers charged with preventing both shoplifting and employee theft.38

Especially in the case of the BBBs, the emphasis on independent monitoring and policing also reflected an attempt to make public education campaigns more effective. For specific cautions about prevailing scams to have real value, they had to occur before too many individuals had taken the bait. “If the information comes to the Bureau only after a number of prospects have already parted with their money,” an article in a trust company magazine explained in 1927, it would be much more difficult “to retrieve for them their vanished funds,” or to “save loss for others.” Such timeliness depended not only on efficient channels of communication, but also on an extensive warning system of “listening posts” that would allow fraud monitors to pick up early signals of commercial or financial chicanery, and on the willingness of the “public... to report immediately anything that appears at all questionable or doubtful.”39

Antifraud organizations further recognized that heightened enforcement was a crucial precondition to strengthening deterrence against fraud, and that such enforcement would have to overcome the daunting barriers to collective action that were rooted in administrative incapacity and an individualistic commercial culture. The tendency of fraud victims to avoid the time and expense associated with criminal proceedings, especially if they were able to extract some restitution from a swindler’s squawk fund, presented companion difficulties for law enforcement. Silent suckers furnished authorities with no basis to launch an investigation, no oral testimony or documentary evidence on which to base a prosecution.

In their public education initiatives, antifraud institutions repeatedly chipped away at the common disinclination to bring swindlers to justice. NACM leaders implored members to maintain good recordkeeping practices, which eased evidence-gathering should any debtors turn to fraud. It also extolled the civic-mindedness of executives who treated credit swindlers with the contempt that they deserved, and heaped scorn on those who ignored their civic responsibilities by accepting compromise offers in fraud cases. “DON'T let apathy and supinity rule when you have been victimized by a credit crook,” the editors proclaimed in one 1914 issue. “Remember, he has made a raid, not on you alone, but on the great business organization of which you are but a part. Arouse yourself; do all in your power, cost it little or much, to rid the commercial commonwealth of those who would assault that relationship of faith and confidence... which is the basis of solid business growth” The credit man with a spine, the manly credit man, worked to send fraudulent debtors to prison, even at significant short-term cost, just as the manly retailer lived up to the promises in advertising spreads.40

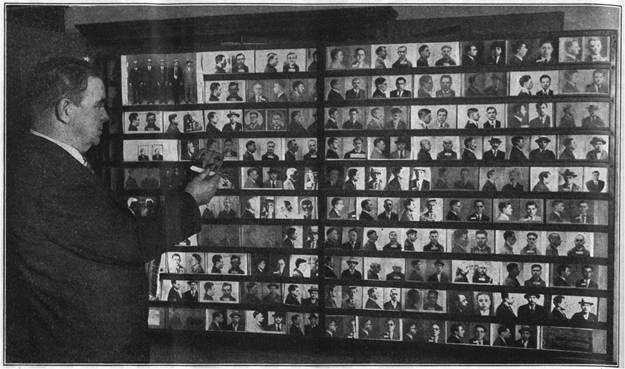

Even when defrauded individuals or businesses wished to assist law enforcement, though, investigative complexities often strained the capacity of early twentieth-century police forces and prosecutors' offices, especially when swindles operated across state lines. By building up a corps of professional investigators, many of whom had experience in district attorneys' offices or as postal inspectors, antifraud organizations attempted to match the sophisticated tactics and geographic reach of the most successful perpetrators of fraud. By the early 1920s, both NACM and the NVC had developed national evidentiary clearinghouses. They kept track of evolving scams and the careers of prominent swindlers and maintained “Rogues' Galleries” in the form of photographic collections that helped identify individuals who had a penchant for skipping town and changing names and life stories (Figure 7.3). The national antifraud network thus facilitated the sharing of intelligence about transient fraud and fraudsters. Once antifraud investigators amassed what they viewed as clear-cut evidence of criminal activity, they passed along the findings to governmental officials in the appropriate jurisdiction.41

The cultivation of investigative capacity dovetailed with the NACM's and Better Business Bureaus' goals of public education. A network of seasoned detectives facilitated arrests, indictments, and prosecutions, all of which received extensive coverage from a sympathetic press corps. The resulting stream of enforcement-related stories offered additional opportunities to inform the public about the telltale signs of fraud, while signaling to both outright swindlers and legitimate enterprises that deceptive marketing brought consequences. Such attention, BBB officials maintained, generated “public indignation,” which in turn “spurred prosecuting authorities and juries to a less lenient frame of mind where swindlers are concerned.” Fundraising campaigns, such

Figure 7.3: An NACM investigator compares a photograph of a credit-fraud suspect with the pictures in the organization’s Rogue’s Gallery, which it kept in New York City. From Credit Monthly, March 1928.

as the NACM’s effort to raise nearly $2 million to support investigative efforts in 1925, furnished similar opportunities to heighten awareness of antifraud messages.42

By keeping initial fraud monitoring and investigations within their own institutions, antifraud organizations maintained flexibility in law enforcement— and likely far more than would have been feasible through a strategy of lobbying to place more public detectives and prosecutors on the fraud beat. In cases where an established firm embarked on a marketing campaign that flirted with misrepresentation, the BBBs initially approached it quietly, “endeavor[ing] to impress the advertiser with the desirability and the advisability of raising the standard of his own copy.” Most of the time, managers accepted proposed adjustments, even agreeing to retract advertising. BBB publications teem with overviews of these settlements achieved through “friendly persuasion.” The 1928 Annual Report of the Kansas City Bureau, for instance, reported that it had “secured changes in 670 inaccurate advertisements,” ranging from instances of “Underwear Over-valued” and “Furniture Cut Deceptive” to “Deceptive Comparative Prices” and “Real Estate Exaggerations.” If advertisers rebuffed efforts at moral suasion, Bureau officials often progressed to public disclosure, using their publications, connections, and public relations to shine a spotlight on a given business’s problematic tactics. Cases went to state or federal prosecutors only when BBB administrators confronted what they viewed as recalcitrance, which occurred only once or twice for every hundred legitimate complaints.43

One needs to keep the scale of the business establishment’s war on fraud in perspective. After two decades of rapid expansion, the persons collectively employed by the BBB network likely totaled fewer than a thousand, a workforce roughly similar in size to that employed by a single large-scale advertising firm such as N. W. Ayer & Co., and less than 3 percent of the employees at a leading national retailer such as Sears, Roebuck & Co.44 At no point did the bureaucratic resources of NACM and the BBBs approach those of the largest corporate enterprises. Indeed, the corps of store detectives working for the nation’s large urban department stores probably exceeded the full complement of BBB employees and NACM’s Prosecution and Investigation Department combined, while the force of private railroad police, totaling ten thousand in 1930, certainly did so.45 Nonetheless, the number of fraud monitors and educators compared favorably with the administrative infrastructure at the Federal Trade Commission. In 1930, the FTC employed only 450 persons and possessed an annual budget of approximately $1.5 million, with which it had to carry out its legal mandates to enforce not only federal prohibitions against deceptive advertising, but also violations of the antitrust laws. If one adds the considerable in-kind contributions of advertising space by publications and radio stations to the BBBs, the educational and disciplinary footprint of the antifraud organizations greatly outstripped that of the pre-New Deal Federal Trade Commission.46

The Scope of Capitalist Collectivism

Suffusing all of these various activities—lobbying to extend statutory prohibitions of deceptive commercial communications; campaigns to inoculate the public against scams and schemes and convince businessmen to resist the inclination to adopt or accommodate such deceptions; articulation and dissemination of commercial standards and best practices; construction of private, professional antifraud bureaucracies—was an extraordinary degree of confidence. Leaders of the maturing antifraud establishment were not bashful about asserting their expertise in matters concerning fraud, which they expressed most commonly in the idiom of public health. NACM officials characterized their endeavors as “sanitary work” or “organized credit hygiene,” and insisted that “communities should be vaccinated against commercial crime just as they are against smallpox.” Credit Monthly represented the association’s spokespersons as credit physicians who safeguarded the country’s businesses from the

Figure 7.4: Dr. NACM takes on the credit crook. Credit Monthly cover, February 1926.

poisonous depredations of the “credit crook.” BBB managers received an analogous message from NYSE President E.H.H. Simmons in September 1927. The Bureaus, Simmons declared, had obligations in the “economic and business field closely resembling [those] which medical men [have] in the field of public health and sanitation.” Just as physicians had “educated the public in matters of health... rendering it immune to the scourges of disease which formerly worked such havoc with human life” so antifraud leaders had the fundamental tasks of “educating] the American investor into a similar condition of immunity from... the swindling profession, and... clear[ing] up the conditions where these parasites on our national business establishments lurk and breed.” Like public health officials who combated the environmental conditions that bred tuberculosis, yellow fever, and malaria, antifraud professionals portrayed their labors as rooted in scientific understanding and aimed at protecting the public from dangerous scourges.47 Depictions such as a 1926 rendition of “Dr. NACM” (Figure 7.4) expanded upon the rhetoric that had animated regulation of adulterated fertilizers and foodstuffs. Now all antifraud work took on the sheen of science.

Accompanying such self-presentations were insistent claims that antifraud organizations represented the United States writ large and looked out for the “public welfare” without fear or favor. NACM publications characterized its members as crusaders for the economic commonweal, on occasion depicting them in the garb of medieval Crusaders, upholding the ancient virtues of Vigi- Iantia and Fidelitas. BBB officials proclaimed that they had “no axe to grind” and no interest to protect, that their “methods have been scientific,” that, perhaps most strikingly, they were “literally of, by, and for the public.” The Oklahoma City Bureau declared in 1930 that the organization was “[u]nprejudiced, unbiased, and adher[ing] strictly to its own work and purposes” and that it “never allowed its facilities or influence to be used to further selfish or personal rights.” One president of the National BBB similarly pronounced that antifraud work sounded “the undoubted note of patriotism... which adds to the general prosperity of our country.”48 Indeed, antifraud professionals often asserted de facto jurisdiction over fraudulent behavior, a move that the media tended to ratify, as through a 1926 New Orleans Times Picayune cartoon depicting NACM as a motorcycle cop hot on the heels of a band of commercial swindlers (Figure 7.5). The cartoonist added a “U.S.A.” nameplate and titled his drawing “The National Policeman,” clothing this private association of business executives with the legitimacy of the state.49

Throughout the 1920s, America's dominant Republican Party blessed the quasi-public character of antifraud institutions, with the country's highest officials giving them full-throated endorsements. President Calvin Coolidge observed that “wherever deception, falsehood, and fraud creep in, they undermine the whole structure,” a calamity to “our commercial life” that could only be prevented “by the businessmen themselves.” His successor, Herbert Hoover, praised the BBB network for greatly “contributing to the economic stability and progress of the country.” Treasury Secretary Andrew Mellon, Attorney General John Sargent, Secretary of the Post Office Harry New, and many lower-level political appointees expressed similar sentiments.50

The standing of antifraud professionals with Republican leaders translated into influence over key legal appointments. The New York City and National BBBs, the Investment Bankers of America, and the NYSE all had significant say over prosecutorial positions in their bailiwicks, such as the United States attorney for New York's Southern Federal District or the New York State assistant attorney general responsible for enforcement of securities fraud law. Government detectives and prosecutors who had experience with fraud cases also frequently accepted employment at private antifraud agencies. With such strong connections, it should come as no surprise that the era's law enforcement officials leaned heavily on these organizations, especially when embarking on high-profile fraud crackdowns such as the Post Office's campaigns

Figure 7.5: NACM as the national vindicator of the law. New Orleans Times Picayune, reprinted in Credit Monthly, May 1926.

against fraudulent Texas oil companies and Florida real-estate scams during the 1920s.51

The antifraud crusade wished to remake commercial culture across the United States. As such, it constituted something of a social movement within the confines of American business, though one emanating from the ranks of the elite, rather the social or cultural margins. The campaign’s leaders and troops embraced the challenge of convincing corporate bigwigs, small-scale entrepreneurs, middle managers, securities promoters, and advertising professionals that they should eschew the quick buck, and rather act with regard to long-term reputation, the stability of their industries, and the health of the

Figure 7.6: Attendees at a 1929 Better Business Bureau Conference in San Diego. Courtesy of Western History and Genealogy Division, Denver Public Library.

broader economy. As the members of the antifraud vanguard fine-tuned this pitch, they put forward numerous sober arguments. But they also conjured evangelical visions of manly commercial fellowship and self-consciously infused their creed into the business establishment’s evolving social rituals.

Toward these ends, NACM and the BBBs annually convened national conventions, like the 1929 BBB meeting in San Diego depicted in Figure 7.6, where members of the antifraud fraternity deliberated over new tactics, expanded networks of information-sharing, and mutually testified to the righteousness of their “Crusader Spirit” and “nation-wide effort.” They made periodic fundraising campaigns into collective expressions of esprit de corps, through which participants could offer tangible evidence of commitment. Even more frequently, local chapters held lunches and dinners or dispatched speakers to the monthly meetings of Rotary Clubs. At such gatherings, business leaders shared a good meal at a local hotel, and then, “after cigars had been lighted,” listened to a talk that harangued the fraudster and those who abetted his machinations, while extolling the business community’s exertions to rid itself of confidencekilling deception. Tellingly, antifraud activists did not shy away from the language of communitarian action, characterizing their initiatives as a “movement” for truth-in-advertising. The commercial establishment’s fight against fraud depended as much on personal contexts of fellowship as it did on sophisticated lobbying campaigns, impressive public relations machinery, and ever more extensive bureaucratic techniques of commercial surveillance.52

Movement-building events could attain an impressive scale, reflecting the seriousness and financial commitment that undergirded the early twentiethcentury antifraud war. A gala annual dinner thrown by the St. Louis BBB in the spring of 1941 exemplified pivotal dimensions of communal occasions. On the main floor, BBB leaders and invited guests sat at head tables on the side, while representatives from BBB member firms and local dignitaries shared tables in the center. On the mezzanine level, scores of students from more than fifty high schools had the chance to listen to the speechifying, and to begin the process of identifying with the battle against cheats and swindlers. Large American flags festooned the mezzanine railing, reminding participants that the antifraud fight was America’s fight. Over one thousand St. Louisans purchased tickets to this gathering, a testament to the “sincerity and determination on the part of legitimate business to rid the community of improper practices.”53

The early twentieth-century drive against commercial fraud tracks patterns evident in most social movements. Whether arising out of evangelical rejection of prevailing institutions and practices, working people’s demands for greater economic security and political power, disfavored social groups’ insistence upon equal citizenship rights, or the concerns of economic elites about pervasive commercial humbuggery, such collective undertakings have faced similar challenges. The historical enemy might be slavery, alcohol consumption, unequal bargaining power, discrimination on the basis of race/gender/ sexual orientation, or business fraud. In all these contexts, movement leaders had to fashion a new sense of identity around issues of shared concern and build deep commitment to the cause, often by creating new kinds of emotional experience. Invariably, modern social movements have sought to subordinate individual concerns and interests to broader communitarian norms. Such endeavors have always required the construction of engrossing narratives that pull individuals into the movement, connect personal identities to the cause, and convince participants that their actions will make a difference.54

To purge American marketplaces of chicanery, officials such as J. Harry Tre- goe and H. J. Kenner tried to reframe the emotional stakes of day-to-day marketing practices. Through their organizations’ publications, public narratives, and social events, these standard-bearers sought, in the language of behavioral economics, to leaven “market norms” with “social norms,” to inject communal values into business culture.55 In doing so, antifraud leaders contributed to a broader effort by interwar business interests to impose order on the dizzying transformations within America’s industrial economy, chiefly by confining the channels of permissible competition.56

In many respects, the work of the NACM and the BBBs reflected the antipathy of corporate America to administrative agencies that could bog down enterprises with endless rules and bureaucratic processes.57 The new business- funded antifraud organizations, like so many of their corporate patrons, rejected most proposals to create large and intrusive government bureaucracies as a strategy of addressing the social ills, economic instability, or other externalities generated by modern industrial economies. In the securities arena, for example, BBB leaders vigorously criticized any suggestion that the state ought to protect investors by licensing stockbrokers or, even worse, by vetting public securities offerings to ensure their legitimacy. Indeed, the founding of the New York City BBB formed a central element of Wall Street's efforts to deflect state legislative proposals for “blue-sky” legislation that would create such administrative authority. As the AACW argued forthrightly in 1919, “if an industry does not clean house for itself, the law will do it, and the law often operates in such a manner as to injure the legitimate while seeking to stop the faker.”58

Visceral antagonism to the heavy-handed administrative state was accompanied by a hearty embrace of the post-World War I Republican call for asso- ciationalism. NACM's efforts constituted a leading example of the Republican preference for trade groups that responded to economic challenges through mutualistic standard-setting (in this case, with regard to evaluating credit requests and exchanging credit intelligence). Although the BBBs had a much wider purview than most trade groups, they facilitated associationalism in a host of contexts. Most importantly, the Bureau network defined and continually refined principles for truth in advertising, which they disseminated among newspapers, magazines, radio stations, advertising agencies, and frequent advertisers, such as urban department stores. In the latter half of the decade, the National BBB also joined with the Federal Trade Commission to convene conferences among leading retailers of furs, furniture, and numerous other lines of goods, to hammer out transparent standards for the use of trade names that would avoid confusion among manufacturers, dealers, and the buying public.

Again and again, the antifraud establishment characterized their initiatives as forms of “home rule” by American business, paralleling the sentiments that drove associationalism in so many other corners of the post-World War I American economy. As H. J. Kenner emphasized in a 1926 speech, the organized business community had pledged to keep “its own house in order.” Through the BBB's educational efforts, impartial monitoring of the marketplace, and disinterested cooperation with the authorities in law enforcement, Kenner argued, “[b]usiness will impress Government and the public alike with its determination to police its own domain. Respect for Business and for Law will then grow apace.” This preference for commercial and financial selfgovernment greatly influenced the BBB's approach to fraud policing, which stressed, wherever possible, flexible adjustments or reliance on the pressure of public disclosure, rather than a turn to the all-too-cumbersome disciplinary power of the state.59 In fashioning a discourse of “home rule,” the antiswindling brigade mirrored the contemporaneous language of Southern segregationists. Like their political counterparts in the Southern Democratic Party, who demanded unchallenged jurisdiction over race relations in their states, business elites asserted their right to deal with issues related to fraud on their terms, through their own administrative and investigative authority.60

The dilemmas posed by duplicitous commercial speech, however, convinced a broad cross-section of American business leaders of the need for an additional layer of governmental oversight. The specter of diminished public confidence led corporate leaders, especially within the sectors of large-scale retailing, finance, and the media, to turn to the state for retrospective economic regulation through the criminal code. Through vigorous enforcement of a tighter set of criminal fraud laws, the business establishment expected to clamp down on dodgy small-scale enterprises and outright fly-by-night firms. Such enforcement centrally involved the state—indeed, it entailed increased resources for investigative and prosecutorial manpower and led to the creation of several new divisions focused specifically on fraud, such as within the offices of New York’s attorney general and the US attorney in Southern New York. Such public fraud-fighters, however, worked in conjunction with the new nonprofit organizations created by business elites. Those entities often had greater financial resources and administrative capacity and increasingly served as an investigative filter, handling initial complaints and deciding which cases merited governmental attention.

The cozy relations between antifraud organizations and law-enforcement officials faced no sanction from the American judiciary, in sharp distinction to the cold shoulder that the era’s judges gave to price-fixing agreements and efforts to share information about prices and costs. American cartels and openprice associations had to struggle against age-old legal suspicion of restraints of trade.61 NACM and the BBBs, by contrast, could and did portray their endeavors as attempts to vindicate American law, to breathe life into longstanding common-law precepts against economic deceit that had remained mainly dormant because of practical barriers to fraud prosecutions.

In both state and federal courts, judges typically endorsed such activities. As one member of the federal bench argued in a 1941 case concerning the obligation of the Oklahoma City BBB to pay Social Security taxes,

The Bureau carries on a continuous campaign of fraud prevention work. It warns the public against fraudulent plans and schemes. It endeavors to induce the local advertising agencies not to accept advertisements from the promoters of such plans and schemes. Through newspaper advertisements, radio talks, bulletins, and posters, it acquaints the public with fraudulent practices. It exposes specific fraudulent practices being carried on in Oklahoma City. It also endeavors to induce merchants to refrain from misleading advertising, extravagant claims, and price comparisons, and to conform to a high standard of business ethics. It endeavors to educate the consumer to buy wisely.62

This supportive depiction might as well have been authored by a BBB official. In 1929, New York City magistrate George W. Simpson penned a perhaps even more revealing note to H. J. Kenner in advance of the latter's appearance at a Rotary Club luncheon, imploring Kenner to “enlist Rotary in our cause,” by which he meant the effort not only to “stop outright fraud,” but also to “head off... border-line fraud.” Simpson signed the note, “Fraternally yours,” an epistolary gesture that helps to explain judicial deference to the strategies of public-spirited businessmen and antifraud professionals, who, after all, possessed similar socioeconomic and educational backgrounds as the prototypical mid-twentieth-century American jurist.63

Unsurprisingly in light of such sentiments, American judges shied away from placing roadblocks in the path of the antifraud campaign. When businessmen shamed by Bureaus for fraudulent practices brought libel suits, courts rejected them.64 As a result of this legal acceptance, early twentieth-century business-government associationalism reached its apex in the arena of regulating commercial speech. Here, the cooperative impulse among business elites skirted the typical judicial preference for economic competition. Here, the relationship between business and the American state more closely approximated the situation across the Atlantic, where European governments tended to ratify price-fixing agreements in order to stabilize a tumultuous economic environment.

Because the early twentieth-century antifraud campaign received such strong support from American government, it represented an ambitious experiment in business self-regulation. Its champions did not hesitate to trumpet its successes, which they depicted as a vindication for business “home rule” and “self-government.” Antifraud leaders missed few opportunities to broadcast achievements, especially in bringing the individuals, businesses, and rings who engaged in fraud to face the criminal justice system. Both NACM and the BBBs kept careful track of investigations through monthly updates and annual reports, partly to justify their effectiveness to business subscribers. The two institutions also highlighted evidence of significant contributions to law enforcement, and even some indications of deterrence. Between 1925 and 1929, the labors of NACM's Investigation and Prosecution Department resulted in nearly 1,600 indictments from either state or federal grand juries; of the cases that had gone to trial by June 1929, prosecutors had secured more than 734 convictions, achieving a success rate of over 80 percent. Government prosecutors reported that this showing reflected considerably better conviction rates than before NACM began assisting in evidence-gathering, both for fraud cases and for criminal complaints generally.65 It certainly reflected a vast improvement over the paltry nineteenth-century conviction rates for fraud-related prosecutions.

Over the course of the 1920s, BBB managers could point to an even wider array of accomplishments. In addition to the standardization of trade names through industry conferences, local and national Bureaus had assisted the print media and radio stations in assessing suspicious requests for advertising space, culminating in the rejection of thousands of proposed ads, including nearly all pitches for “get-rich-quick” schemes in respectable publications. They had collectively handled several million complaints about either securities promotions or the marketing practices of advertisers, and had negotiated tens of thousands of adjustments in marketing policies by urban retailers in every region of the country. Such adjustments occurred more readily because of the credibility that the Bureaus possessed in local business communities, and because of their capacity to operate flexibly and, when they so chose, outside the glare of publicity. Like NACM, the BBBs also made a significant mark on the enforcement of fraud laws. Investigations undertaken by Bureaus across the country led to hundreds of indictments and convictions, especially under the federal mail fraud statutes and state securities fraud laws such as New York’s Martin Act, which criminalized deception in securities promotions.66

The nation’s chief fraud opponents further claimed that their undertakings had cut down the numbers of suckers taken for a ride and dramatically improved business ethics. NACM oversaw the founding of dozens of credit exchange and adjustment bureaus across the country, which its officials portrayed as reducing the susceptibility of suppliers to credit fraud. Repeated BBB warnings helped to limit public losses in a host of post-World War I investment and employment scams. Within the realm of merchandising, executives at several large department stores became convinced that the Bureau’s outside monitoring of advertising served as a useful check on store practices, leading to “the improvement of retail stores as public institutions.” As a result of the outside prodding, these executives encouraged their buyers and division managers not only to exercise greater care in formulating advertisements and to cooperate with any BBB investigations, but also to engage in their own surveillance of competitors.67

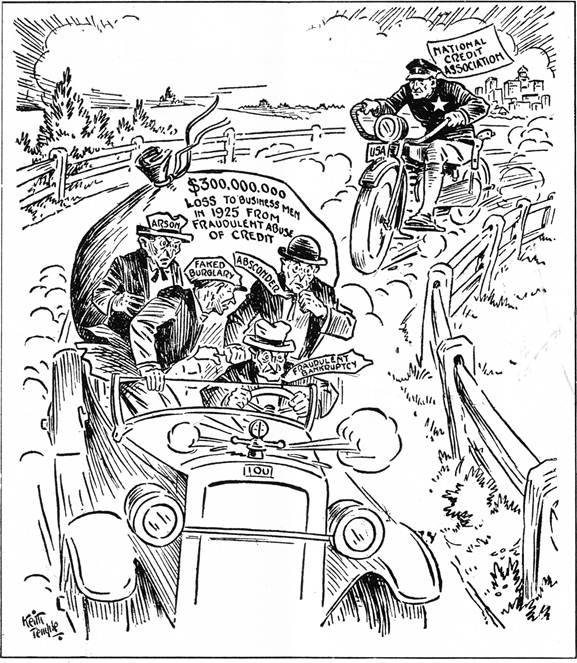

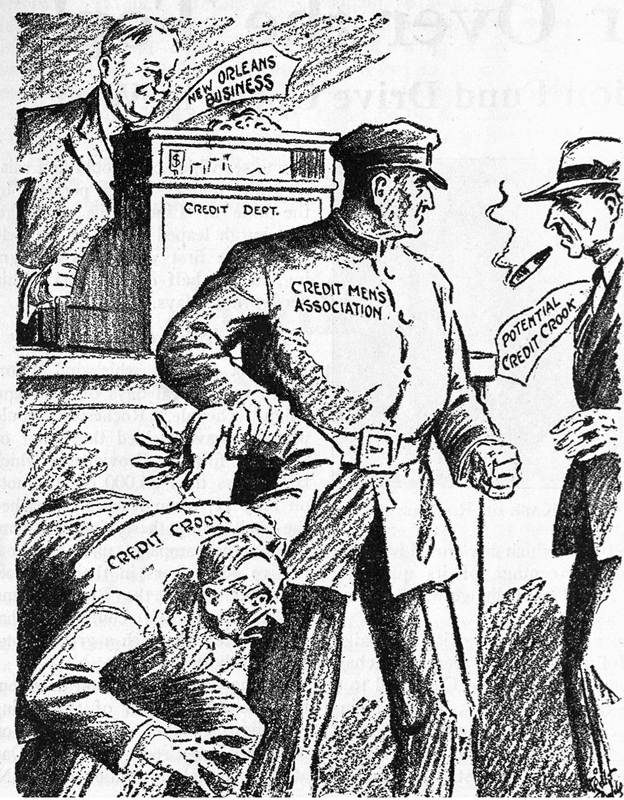

Antifraud professionals could even point to indications that their labors had created a more substantial deterrent to commercial skullduggery. According to NACM, tighter credit standards and heightened prosecution of credit fraud resulted in a 32 percent decline in the number of cases referred to its Investigation and Prosecution Department between 1925 and 1928. As early as 1926, the group's general manager, J. H. Tregoe, assured its members that “ ‘Watch your step' has become the motto of the commercial crook.” The BBBs pointed to assessments of retail advertising in St. Louis that reported only 2 percent error rates by the mid-1930s, and a study of two fraudulent stock promotions that found a disproportionate number of suckers lived outside the areas served by a Bureau. According to BBB officials, such findings suggested that swindlers had learned to avoid their territory.68 Whether or not all of these assertions had a solid factual basis, they gained currency in the nation's print media, as suggested by a 1929 cartoon in the New Orleans Times Picayune (Figure 7.7). Depicting the apprehension of a “credit crook” by a robust “Credit Men's Association,” figured again as a policeman, the cartoon includes as onlookers both a very pleased representative of “New Orleans Business” and a fearful “potential credit crook.”

By the mid-1920s, the growing influence of the American antifraud movement encouraged some of its key leaders to think in transnational terms. Within NACM, officials envisioned an international credit bureau that would monitor relations between commercial creditors and debtors across national boundaries, while fostering “international co-ordination of credit methods and ideals.” Leaders in the “truth in advertising” movement similarly wished to expand abroad, targeting Europe, and especially England, as propitious ground for antifraud bureaus. Such confident proposals for extensions of “soft” American power dovetailed closely with the dramatic expansion of Rotary International and the effort to bring US retailing strategies to Europe during the 1930s. The latter initiatives broadly shared the ideological predispositions of the campaign for economic truthfulness, as well as the participation of many of the same business elites. To commercial leaders such as Louis Kirstein, American “self-government of industry” deserved emulation by other industrialized nations.69

For all the successes of the Credit Men's Associations and the BBBs, the handling of deceptive commercial practices through self-regulation and retrospective law enforcement had some serious limitations. NACM's entreaties that credit managers no longer prefer short-term profits to the longer-term health of the overall commercial credit system clearly did not persuade a great many executives. Otherwise, the Credit Monthly would not have had to continue issuing insistent pleas throughout the 1920s for credit managers to per-

Figure 7.7: A portrayal of deterrence from effective fraud enforcement. From New Orleans Times Picayune, June 1929, courtesy of NACM.

form due diligence in vetting potential mercantile customers, to share their knowledge about problematic debtors, and to refuse to accept compromise payments from dishonest debtors. All of the BBB’s public warnings, all the rejected advertisements and negotiated adjustments of marketing policies, all of the arrests and convictions, did not put that much of a dent in BBB estimates of overall fraud incidence. Cut off from easy access to established media organs, swindlers merely turned in greater numbers to the production of their own tip sheets and financial papers, which they distributed widely throughout the country. No longer able to unload a given worthless stock or real-estate development because of public exposure, promoters moved on to another town, another scheme, often pursuing some twist on well-known scams that kept the sucker bait fresh. At no point in the 1920s did either law enforcement officials or representatives of antifraud organizations estimate actual declines in the annual losses resulting from fraud. Furthermore, the onset of economic depression sharpened the incentives for deceptive advertising, as retailers chased ever more elusive consumer dollars and created new avenues for stock swindling, chiefly through attempts to reorganize bankrupt companies.70

Throughout the interwar period, antifraud campaigners sought to solidify their newly gained authority, often through a kind of rhetorical alchemy. These individuals had to show a business constituency increasingly drawn to quantitative assessments of success that contributions to antifraud organizations led to appropriate and predicted results. But they also had a predisposition to find new threats to commercial confidence and to magnify the nature of such dangers. Like “police” in a variety of contexts, and like modern organizational consultants, antifraud professionals had a powerful incentive at once to crow about their impact and warn about the fearful consequences of not receiving ongoing funding and support.

In addition, antiswindling campaigns consistently cast suspicions on Americans from the commercial and social margins. These undertakings were funded by large-scale enterprises whose managers believed that small firms constituted the gravest threat to standards of fair-dealing. Leaders at NACM and the BBBs came from America's native-born, Protestant establishment, and their worldviews were shaped by the values and expectations of that establishment. J. Harry Tregoe, the most important leader at NACM during its first thirty years, offers an instructive example. A fixture of Baltimore's Presbyterian community and a stalwart Republican, he devoted considerable attention to his city's (Baltimore) Young Men's Christian Association, expressed deep- seated hostility toward alcohol consumption, and imbibed the waxing nativ- ism of the post-World War I era. His political and cultural sensibilities had a great deal in common with that of a nineteenth-century antifraud crusader such as Anthony Comstock. To Tregoe, the basis of American civilization was under siege from both the “low-thinking foreigner” and the labor radical. As he explained when denouncing the labor leader Samuel Gompers for criticizing a Supreme Court decision in 1922, “the safety of America is threatened by barbarians like those who caused the downfall of Rome.”71