COMPARING MARKETPLACE LOANS WITH BANK CREDIT OR CREDIT CARD DEBT

From the perspective of borrowers, marketplace loans compare to credit card debt and short-term consumer loans in terms of interest rate. However, this comparison is less fitting that it might seem, as there exist important differences between these loan products and marketplace loans.

2.7.1 How do marketplace loans differ from bank credit?

Marketplace lending platforms have streamlined the process to get both borrowers and lenders to sign up. For example, all of the large marketplace lending platforms offer online and mobile loan applications that potential borrowers can complete in under 30 minutes. These are not just quotes and inquiries but actual loan applications. Compare this to an average of 26 hours that small businesses will spend on filling out paperwork at several conventional banks before securing some form of credit.19

Banks also offer ways for borrowers to apply for loans online. Their turnaround is usually slower but some banks, such as Wells Fargo in the U.S., offer same-day loans that allow the borrower to leave the branch with a check in their pocket. Still, bank loans usually cost more, and the chance that the application will be declined, especially for smaller loans, is high. When we compare the process of getting credit on a marketplace lending platform with getting a bank loan, both sides offer advantages and disadvantages. Table 2.4 compares a loan from popular marketplace lending platform Lending Club with a similar loan from Wells Fargo Bank.20

After banks have validated a borrower’s credit history, the most important difference lies in how they mitigate their credit exposure. When banks underwrite a loan, they protect themselves from losses in two areas, as we will discuss later in Chapter 9 about credit exposures. First, banks calculate the expected loss under expected normal conditions and compute what they have to charge the borrower to hedge this loss.

With collateralized loans, this step is very straightforward: the lender simply calculates the default probability as well as whether the value of the collateral is high enough to cover losses when they occur. When loans are uncollateralized or unsecured, such as in marketplace lending, the lender needs to compensate through the interest rate and spreads. Secondly, banks calculate the unexpected loss under stress conditions and ask themselves what they can do to minimize losses, survive, and remain profitable. This may include portfolio restructuring, optimizing collateral, hedging, increasing capital reserves, and other steps.Conversely, does the interest rate of marketplace lending platforms cover loss from default under stress conditions? Should they charge more, or are they in fact destroying the market by undercutting prices? The interest rate in online lending is actually not market interest, but a counterparty spread. Under normal conditions, these spreads are fine because they cover credit losses. But under stress conditions, they fall short. This is markedly different to the way banks operate: banks hedge their exposure with higher interest and derivatives and optimize their portfolio with risk management techniques. When they are rolling over, they restructure and optimize their portfolios. Contrary to the practice of marketplace lenders, banks avoid

TABLE 2.4 Comparison of a personal loan for a borrower with perfect credit from Lending Club with a loan from Wells Fargo Bank in 2014

| P2P lending platform21 | Wells Fargo Bank | |

| Amount Term Interest rate Turnaround time Convenience | Up to $35,000 36 or 60 months 6.78% Faster Higher, the entire process is online, with less paperwork involved | Up to $100,000 12 to 60 months 7.23% Slower, except for same-day loans Lower, more paperwork involved |

TABLE 2.5 Comparison of a personal loan from Lending Club with credit card debt

| P2P lending platform22 | Credit card23 | |

| For excellent credit | 6.7% | 10.4% |

| For good credit | 7-16% | 14.91% |

| For fair credit | 17-30% | 23-30% |

| Interest rate | Fixed | Variable |

| Term | Fixed | — |

| Late fees | $15, no impact on interest rate | About $30, impacts interest rate |

using their interest income as collateral to cover losses. They use actual collateral in the form of financial assets, hard assets, or guarantees.

Then they hedge the remaining exposure with derivatives.2.7.2 How do marketplace loans differ from credit cards?

Things look a little different when comparing a marketplace loan with credit card debt.24 Table 2.5 shows some characteristics of each.

Credit card debt is not a loan but a credit line with a pre-approved limit. Credit lines are convenient to create and hard to pay down. Even though it is deceptively easy to max out a card, it takes much more discipline to pay down credit card debt than a loan with a designated term and a fixed interest rate. Most marketplace lending platforms are less expensive than credit cards, both in terms of the interest they charge and their fees. This is the reason why lenders use marketplace loans to refinance or consolidate credit card debt.

Credit cards provide free credit with no payments on interest for a certain term, for example for 45 days. A credit card owner may or may not use the agreed principal of the credit facility up to the credit line. Marketplace loans provide medium-term loans of 3 to 6 years. In bank credit, this hardly qualifies as a long-term loan, which would be a mortgage lasting 30 years or more. Regardless, marketplace loans are also not necessarily short-term loans in the classic sense, which might be a credit facility or short-term loans, such as payday loans.

Credit cards as short-term credit facilities have, under normal market conditions, insignificant market risk. The interest rate includes no market risk premium, with is the case also in marketplace loans. The interest rate is, in fact, a premium against counterparty credit risk, or in other words, the probability of default. Marketplace loans with a set amount of principal are exposed to both market and counterparty risks. Therefore, they should include a market risk premium and a counterparty risk premium. The rate should include the risk-free rate of the market and the risk-neutral probability of default. The expected loss drives the risk premium.

Most of the debate about marketplace lending platforms circles around the benefits for borrowers. However, banks currently offer no access to consumer credit or small business loans to lenders. There are some credit hedge funds that invest in this asset class, however, they are out of reach of retail investors. Marketplace lending offers them a chance to access credit and integrate it as a new asset class into their portfolio. Democratizing the investment in credit without securitization may be one of the most significant innovations that marketplace lending has brought about.

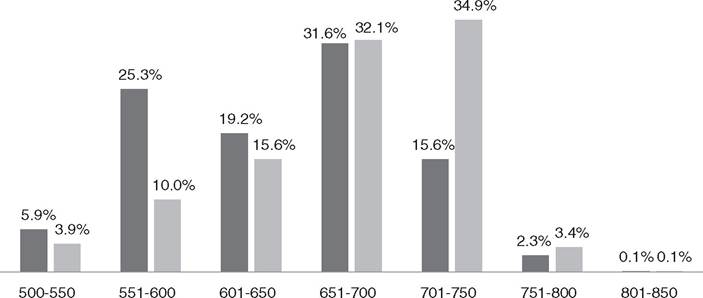

Alternative lending by credit score

■ % of Cases ■ % of Amount

FIGURE 2.10 Alternative lending by credit score

Data source: Biz2Credit

2.8