ONBOARDING PROCESS

Marketplace lending platforms cater to both lenders and borrowers. Therefore, usually the first thing they do is segment both target groups and provide each with the services they are looking for.

Depending on the role visitors of a platform assign themselves—borrower or lender—they immediately enter a customized onboarding process. This process starts with getting users to sign up for accounts on the platform as they would on a social network. Additionally, and more importantly, it is also a mechanism for users to understand the risks and rewards of marketplace loans and the obligations of borrowers. In organizational psychology, onboarding describes the process through which new hires learn necessary skills and behaviors to become effective members in the organization.18 Marketplace lending platforms use onboarding in a similar way. Rather than having subscribers with just a vague idea of how to use it, the platform only offers full functionality to verified users. This is done through a series of questions; the answers given by the users enter into an automated cross-check. User verification is instant, but if a check fails, the application will not be complete. There are also several disclaimers where users must confirm that they have read and understood how the platform will operate.Because platforms distinguish between accounts for borrowers and lenders, if a visitor has signed up as either one, a second account will be necessary to become both a borrower and a lender.

2.6.1 Borrower onboarding

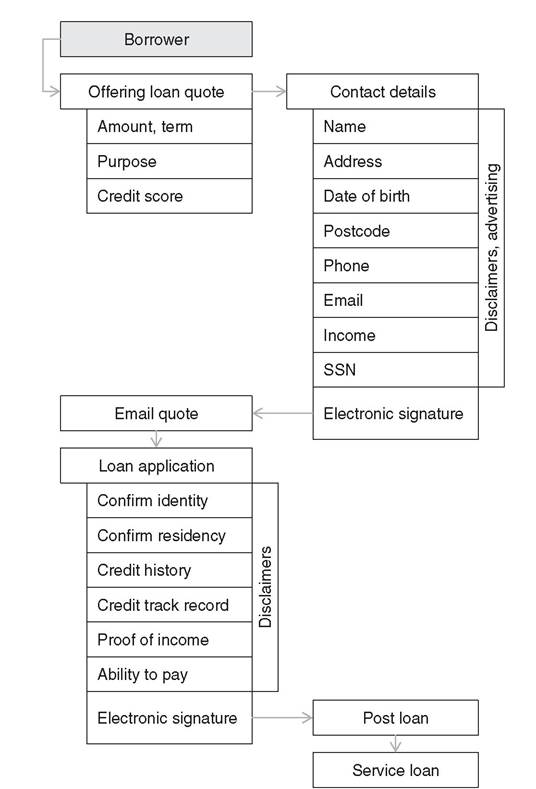

Figure 2.8 shows the onboarding process for borrowers, which most platforms follow in one form or another. Some might ask for certain kinds of information later in the process but, all in all, the process follows a similar logic.

Most platforms offer a quote for a loan by email on their landing page. Prospects will only receive this quote when their details have been verified.

The level of detail at this stepTABLE 2.3 Challenges for marketplace lending platforms

| Challenge | Description |

| Market risk | Market conditions hardly affect borrowers and lenders because of fixed rates. However, the fixed rate may be an unexpected disadvantage when it falls below the real interest rate when market conditions change. |

| Market conditions | Platforms thrive on the gap between normal and stress conditions after the financial crisis 2007/8. In markets with persistently low interest rates, can platforms compete with banks who make longer term loans at lower rates? |

| Credit risk and counterparty risk Operational risk | Lenders are directly exposed to credit and counterparty risks of borrowers without a buffer in between. There is additional operational risk such as fraud when dealing with platforms, due to lack of high security systems. This is especially important in less developed financial markets. |

| Concentration risk | Platforms do not assess or report concentration risk at the level of the counterparty or individual exposure. |

| Trust | Counterparties need to build trust in each other bilaterally in addition to trust between the counterparties and the platform. |

| Virtual presence | Operations of platforms are entirely web-based. Service providers of the back-end infrastructure play a secondary role. |

| Lack of collateral | In most instances, borrowers provide no collateral to secure credit exposures. |

| Intransparency and market fragmentation | Each platform has its own definitions, conventions, models, scoring algorithms, and analytics. This makes comparison between platforms difficult. |

| Counterparty rating | Rating process for identifying the credit worthiness of counterparties varies from platform to platform and is relatively intransparent. Banks, on the other hand, share the ratings provided by rating agencies; for retail portfolios, they disclose ratings via regulatory reports. |

| Design of contracts | The contracts defining the exchange of cash flows among the counterparties are relatively simple; they are short-term annuities with fixed interest rates. |

| Liquidity | The only assessment of liquidity is funding liquidity—the ease with which borrowers can obtain funding. |

| Loan valuation Profit and loss analysis | Valuation rules applied to loan contracts during the term are intransparent. Platforms do not conduct profit and loss analysis on the level of each counterparty; they do not estimate economic capital. |

| Speculation and securitization Regulation | Speculation by lenders against securitized exposure may undervalue risk on the platform. Currently, only limited regulation applies to marketplace lending platforms. |

varies from platform to platform. Depending on the country in which they do business, there are different registers against which platforms can verify the identities of potential borrowers. Once the information has checked out, prospects will receive an email with a quote that they are free to reject or accept. At this point, they already have an account on the system, and they can log in and submit a formal loan application at any time. When they accept a loan, platforms undertake further verification of the ability and the willingness of borrowers to pay.

FIGURE 2.8 Borrower onboarding process of marketplace lending platforms

Finally, when borrowers have complied with this step, their loan request enters the system, and interested lenders can fund the loan fully or partially.

The time from the first visit to receiving the decision about the loan via email also varies by platform. It normally takes about 48 hours, and several days more until the money arrives in the borrower’s account. Overall, borrowers may receive credit within a week on marketplace lending platforms.2.6.2 Lender onboarding

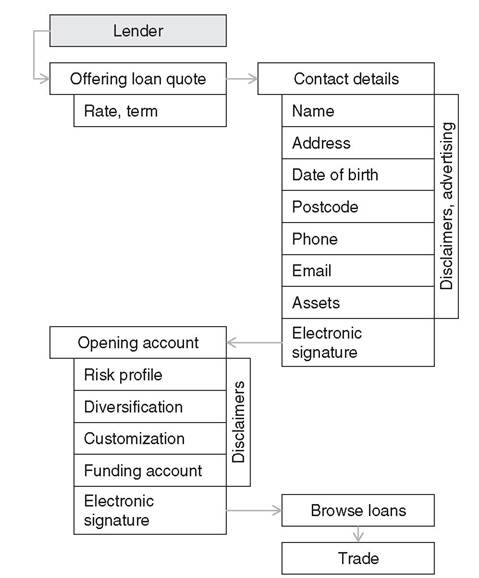

Signing up potential lenders follows a similar process, but it is generally much faster and requires less information. Figure 2.9 shows the onboarding process for lenders.

FIGURE 2.9 Lender onboarding process

When a visitor shows interest in becoming a lender, most platforms offer her a detailed quote of expected returns. To send the quote via email, they collect enough information to confirm her identity. By accepting a platform’s terms and conditions, potential lenders automatically open an account. Platforms will then remind them periodically to fund their account and add details to become lenders on the system. As soon as lenders have linked a bank account to fund loans, they are ready to go. Many platforms offer the option of diversifying across several loans, sometimes with an investment of as little as $25 per loan. Highly diversified lenders often have no idea about the individual loans in their portfolio, nor do they care to know about the particulars. Because platforms classify loans by grades, lenders often construct their portfolio by selecting exposure to a certain grade, rather than to individual loans.

2.7