CONCLUDING REMARKS

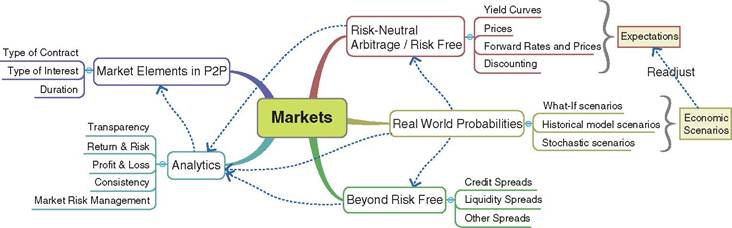

There are two main views in looking at and analyzing markets where both have unique and important roles. The first point of view is based on the risk neutral concept serving the need of applying arbitrage risk-free in the discounting process and pricing financial instruments.

Thus, terms and rates of yield curves and the estimation of their future performance, e.g., by using forward rates, are trying to include the expected losses that may arise due to market risks. However, the future performances of markets may be slightly different or even far from the initial expectations and the ideal risk-free assumptions may turn to reduce the value, provide negative income and experience liquidity distress, all resulting in unexpected losses. This is the main reason why practitioners are taking a second view point by considering the real-world probabilities. Based on such probabilities market risk factors may change to a certain degree. These changes can be based on historical observation or by defining deterministic or stochastic scenarios. The former scenarios are mainly based on what-if future paths, and the latter on algorithmic evolution of a great number of possible paths. The results of these economic

FIGURE 6.5 Detailed elements considered in financial analysis of markets

scenarios are used to readjust the initial arbitrage free assumptions. Thus, beyond the risk-free expectations additional spreads should also be applied, i.e., to include the counterparty, credit, liquidity and other types of risks, as well the consideration of earning profit, i.e., via profit spreads. Such analytics is aimed to increase the profitability and reduce the financial risks in order to provide transparent and consistent analytics in financial systems. It can also be the main toll used in designing the strategies for defining the types, interest and durations of contracts constructing the P2P credit portfolios.

Figure 6.5 illustrates the elements and their relation considered in financial analysis of markets.NOTES

1. Also known as implied forward rates.

2. The FX rates are applicable to deals that refer to different markets.

3. Commodities are physical assets that need to be stored and preserved.

4. Depending on the applied valuation rule.

5. A way to determine forward credit spread is by considering a risk-free benchmark security and spot prices for the risky security; then the forward yield can be derived from the forward price of these securities. Moreover, the difference of forward yields on a risk-free and a risky security is considered. The forward credit spread is estimated by employing the yields of the forward date and the yield to maturity. See An Introduction to Credit Derivatives, by Moorad Choudhry (Elsevier, 2004); and Credit Derivatives Pricing Models by Philipp J. Schiinbucher (Wiley, 2003).

6. Gregory, Jon (2012) Counterparty CreditRiskandCreditValueAdjustment:A Continuing Challenge for Global Financial Markets (New Jersey: John Wiley & Sons).

7. Liquidity spread is usually assigned and defined by the treasury.

8. E.g., based on the funds transfer pricing (FTP) system the liquidity premium is defined as the cost of carrying liquidity cushion averaged over total assets of the bank; see BIS occasional paper No 10 on “Liquidity transfer pricing: a guide to better practice” (http://www.bis.org/fsi/fsipapers10.pdf).

9. An extensive literature is available in regards to detailed explanation on how such cash flows are estimated; a good theoretical as well as practical description can be found in the book Unified Financial Analysis, The Missing Links of Finance (Wiley, 2009).

10. Also known as interest rate term structure.

11. Lending Club (2015a) “What is the minimum investment amount to open an account?”, http://kb.lendingclub.com/investor/articles/Investor/What-is-the-minimum-investment-amount-to- open-an-account/?l=en_US&fs=RelatedArticle, date accessed 23 July 2015.