CONSIDERING MARKET ELEMENTS IN P2P FINANCE

You may have wondered why we treat markets and how banks use them in lending in a relatively detailed way. Establishing a baseline for discussion of P2P loans is important, otherwise we keep comparing apples with oranges.

Let's now overlay what we discussed about markets in this chapter with the characteristics of P2P loans. When we look at them through the lens of established credit markets and the way banks lend, loans originated from marketplace lending platforms have a number of strange characteristics and oddities, some of which are red flags or stand in stark contrast with how the market actually works. For example:■ Loans are relatively risky, so lenders seem to be risk takers. This goes against what we discussed earlier in this chapter, where we implied that most people wish to avoid risk. A reason for taking risks could be the small exposure of individual loans, often as small as $25, as advocated by LendingClub.11

■ P2P loans have a fixed rate, and they never re-price. This implies that the market never changes, which is incorrect, of course. Fixed rates only work precisely with short-term loans, for example, loans that last only one day and that roll over continuously under new terms. This makes sense in markets that are very liquid or where there exists a lot of trust between borrowers and lenders, none of which applies to the market for P2P loans. Fixed rates are profitable when they are much higher than actual rates. Nevertheless, in volatile markets they may result in great losses.

■ Fixed loans also make sense in frozen markets where rates have nowhere to go. But because markets are not effectively frozen, applying real-world economic scenarios to P2P loan portfolios makes sense.

■ The maturities of P2P loans are short to medium term. For this reason, there exists market risk because of potential high market volatility.

■ High spreads between lending and borrowing rates imply high credit losses and a low credit rating for most counterparties.

■ It is unclear how platform operators estimate the value of contracts. It is also unclear how they apply discounting. They consider risk-free yield curves and credit spreads; thus they should be available together with the applied valuation and accounting rules.

What does this mean, and what should we conclude from this list? If a loan portfolio at a bank had the characteristics that we just identified for P2P loans, a bank would advocate the following recommendations to deal with the portfolio:

■ Apply analytics to estimate all returns, i.e., profits, fully understand all risks and calculate resulting losses of the loan book and achieve transparency about market risk.

■ When looking at the entire portfolio of an individual or bank, short-term loans should be used for liquidity only, but not to generate long-term investment returns. Return projections should therefore not center on short-term loans, and they should only make up a small portion of the entire portfolio.

■ Manage market risks by hedging fixed interest rates with interest rate swaps.

Because analytics are still a long way from providing the entire picture of the risk and return potential of P2P loan portfolios, this seems to be an ideal starting point to improve the

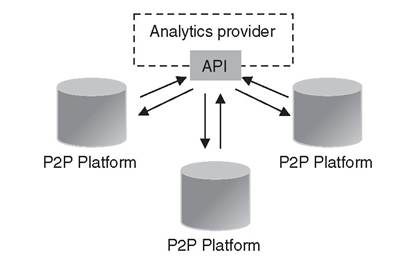

FIGURE 6.4 Analytics provider with API

sector. Only when retail and professional investors can compare potential investments across different platforms, both in the FinTech space and in traditional credit finance, will they be making informed decisions with their money. At the moment, each platform provides its own analytics, some better than others, but all of them a far cry from how banks and professional investors analyze their loan portfolios. A reason for this may be the lack of knowledge within marketplace lending platforms on how to do this, or the high cost involved in programming and deploying analytics.

Analytics talent still resides in banks and professional financial services providers that cater to them. A full suite of industrial strength is costly to purchase and maintain, even for large banks. Unified analytics that P2P platforms could subscribe to would be an excellent opportunity to make marketplace lending more transparent. Such a system does not exist yet, perhaps because the current market leaders in the analytics space lack interest in the relatively small P2P lending space, or because platforms themselves fail to see the need. We imagine a system similar to how banks already use services of third parties. They normally provide an Application Programming Interface (API) through which clients can pipe in their data and then offer the output that they can display on their website. Figure 6.4 outlines how this works, and how different platforms could have comparable data.6.7