DISCOUNTING CASH FLOWS

As we mentioned earlier, risk-neutral expectations reflected by yield curves and discount spreads are used as factors in the discounting process. Then we are employing real-world expectation to readjust the risk-free discounting rates and spread.

Risk-free is mainly applied on static analysis whereas real world is driven by dynamic simulations which are not always easy to obtain.Based on the discounting factors we are defining9 the discounted cash flows and the present value of future cash flows. In this process we are considering the time value of money as well as the risk or uncertainty of future cash flows within the investment time horizon.

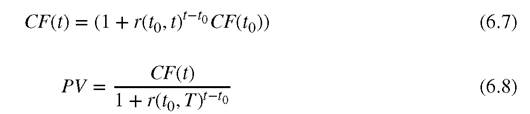

Interest rate cash flows are the most important attribute in loans. Based on time value of money an investor is making at time t0 an investment of CF(t0) and is expecting (or demanding) a higher return when the investment matures at time t as defined in 6.7. In fact interest rate r(t0, t) can be seen as the price the borrower has to pay to the investor for using the capital during the credit period. Moreover, by discounting the investment cash flow using the appropriate interest rate, the present value PV of the investments at t0 that pays a cash flow CF(t) at a future time t is obtained by using 6.8.

The main driver of the interest rates is the time horizon or, in other words, the term of the investment which is expressed by the yield curves.10 There are many models proposed by the financial industry to construct yield curves. However, as they are also driven by the markets they are inherently following some assumptions—such as that they are following positive growth which only under uncertain conditions could turn to negative sign. The expected upward slope of yield curves implies a bias which is the case when arbitrage-free models are applied.

The term structure of risk-free interest rates, which excludes credit, liquidity and any other types of risks, makes the analysis rather easy and convenient. Thus, the single risk-free interest term structure is useful for estimating the interest cash flows and the value of the instrument. Moreover, deterministic shocks and stochastic evolution of risk-free risk factors can be applied in an easy and “clean” concept. In fact, a deterministic stress on a single term structure gives the ability to observe the effect across all financial contracts denominated in the same risk-free factor.

6.3