BEYOND MARKET RISK-FREE RATES

Both approaches of risk-free rates and risk-neutral probabilities are used to analyze financial contracts. They work well in spot and forward markets. However, market arbitrage free models and risk neutrality do not consider other types of risks such as counterparty credit and liquidity risks that impact the value and liquidity of the contracts and investment portfolios.

Markets fail to consider such factors at the contract level. For this reason, they introduce the concept of spreads. In theory, we may imagine spreads as the links between market, credit, liquidity and other risk-free rates, for which risk neutrality cannot be assumed only with market arbitrage free models. In other words, spread encodes the specific credit, liquidity and possibly other risks of the individual contract.There are some important characteristics of spreads defined by the markets that we should highlight:

■ Spread curves have the same properties as yield curves, i.e., containing terms and rates; spreads, however, display additional dynamics and may change independently of market risk-free rates. Therefore, they are independent risk factors and have to be modelled as such. Modelling spreads risk factors with the same properties as yield curves also allows the same risk analysis techniques to be applied as are available for yield curves, e.g., risk, sensitivity and stress scenario techniques.

■ They are applied as an add-on on discounting risk-free rates impacting the value, income and liquidity.

■ They normally refer to whole classes of contracts such as loans.

■ They rarely move as much as risk-free rates; having said that however, spreads can be moved violently under uncertain and turbulent conditions.

■ They can be represented as coupon or zero rates and it is possible to derive forward spreads in similar ways as in forward rates.

■ Spreads are changing over time. However, under normal conditions, spreads are expected to move less than market risk-free rates.

Spreads aim to include credit, liquidity and possibly other types of risks linked to financial contracts. Therefore, spreads ł are additive to the market risk-free rates r (τ) to finally determine the rate R used for pricing or discounting process, e.g., LIBOR plus ł, as illustrated in 6.6:

where the index i indicates the add-on spreads, including credit discount, liquidity and other types of spreads.

6.4.1 Credit discount spreads based on risk-neutral default probabilities

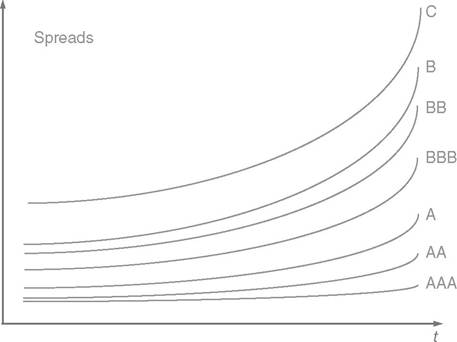

Credit discount spread applied as an add-on factor above market risk-free is the indicator of the risk premium demanded by the investor, e.g., lender, against expected losses resulting from the credit event of the obligor, e.g., the borrower. Credit risk-free spreads are estimated from the losses considering the risk-neutral default probabilities discussed in Chapter 7. Moreover, as illustrated in Figure 6.3, credit spreads are associated with the counterparty credit ratings, which are a reflection of the risk-neutral default probabilities and the resulting expected credit losses within a time horizon. Used as discount factor such spreads directly influence the value and liquidity of the financial contracts.

FIGURE 6.3 Example of spread evolution related to credit ratings

As explained in Chapter 9, the calculation of both gross and net credit exposures, and their evolution through time, will give good estimations of credit losses used in defining the premium through credit discount spread. Therefore, such spreads should consider current and/or expected4 net exposure at the time of the revaluation process; we should avoid linking directly the spreads with credit enhancements, but rather with net exposures.

Recoveries, which are driven by behavior characteristics, should also be avoided in defining discounting credit spreads unless they are very well measured.The evolution of discounting credit spreads can be approached in a similar way as in market forward rates deriving the forward spreads.5 Finally, using the analysis of the real-world probabilities, where spreads are stochastically changed or deterministically stressed, discounting credit spreads can be adjusted. The approaches of Credit Value (valuation) Adjustments6 fall into this category.

6.4.2 Liquidity spreads

The failure to receive the expected contractual cash flows, i.e., the rise of funding liquidity risk, as well as the unfavorable trading of liquid assets due to market liquidity risk leads to unexpected losses as explained in Chapter 12. Even though liquidity risk is a result of market, counterparty/credit and behavior risks, practitioners7 employ liquidity spreads in discounting process for evaluating financial instruments.

Thus, assets that are expected to be illiquid, i.e., not saleable or buyable, at a favorable price due to stress conditions will have high liquidity spread and vice versa. A similar concept could also be applied to the probability of continuation of the expected cash flows and capability of applying roll-over process.

Thus, the liquidity spread determines a premium8 that counterparties need to pay, against market and/or funding liquidity risk. Such spreads can basically be applied to most investment, trading, hedging, credit enhancements, financial contracts/investments, e.g., loans/bonds, stocks, index futures, securities, options, credit derivatives, etc.

The liquidity spreads could somehow consider all financial risk factors and their integration; moreover, in many cases such spreads include future strategies and operational issues. They are adjusted by the real-world market expectations and default probabilities of the underlying market and credit risk factors. They are also driven by the market dynamics and thus are expected, over time, to be very volatile.

Additional spreads, on top of the ones mentioned above, could refer to profit and cost coverage, e.g., salaries, taxes, but also premiums paid for hedging or mitigating unexpected losses due to both financial and operational risks.

6.5

More on the topic BEYOND MARKET RISK-FREE RATES:

- Money market interest rates in the Financial Times

- The market simulates the FX market trading activity on at the level of a market-maker market.

- Rates of return and investment rates in poor countries

- Understanding rates of return and investment rates in poor countries: aggregative approaches

- Understanding rates of return and investment rates in poor countries: non-aggregative approaches

- Market Research: Finding the Market Gap

- Market Research: Finding the Market Gap

- Allianz Research. Country Risk Atlas 2024: Assessing non-payment risk in major economies. Allianz,2024. — 179 p., 2024

- Comparing interest rates

- RISK FACTORS

- CONCEPTION RATES

- CAUSES OF LOW CONCEPTION RATES

- Free Marriage

- A. Free Range

- Nutrients cycle at different rates according to element identity and ecosystem type

- Extinction and colonization rates often vary among patches

- Real Good for Free

- Homicide Rates

- The diversity of life reflects both speciation and extinction rates

- Culture and Free Speech