RISK FACTORS

Several factors impact the performance of a portfolio of marketplace loans, namely market risk, credit and counterparty risk, and behavior. Below, we look at these variables and their drivers to understand how they might influence the performance of the loan portfolio.

13.2.1 Market risk

Interest rates of marketplace loans are fixed over the term of the loan, and counterparty ratings set the amount of the initial rate. However, these interest rates2 include both market risk-free rates and discounting spreads, as we discussed in Chapter 6. Because market risk-free rates can be very low or negative in an interest-rate environment that follows a crisis, spreads may make up most of the interest income. As the rates are fixed,3 contracts are not repricing over time. This implies that market volatilities will have no impact on the value and future cash flows. In a sense, fixed interest rates intrinsically neglect market volatilities, but they may increase counterparty and behavior risks as well as the strategies applied in new production or restructuring existing portfolios. When stress in the market increases, and the market becomes volatile, market interest rates for new loans will either increase or decrease, but they will hardly remain the same.

Higher interest rates have a negative effect on borrowers. Because they have to pay a higher rate on new loans, they come under stress as they see the alternative credit system, their lifeline for capital, at risk. New loans under these conditions are unattractive. Those borrowers who agree to new—and in effect, worse—conditions might have a higher probability of default because they will be shouldered with high payments for the entire term of the loan, normally three to five years. However, lower interest rates may also have a negative effect on loans. If a gap opens up between existing rates and those on new loans, this may have an effect on default and prepayment probabilities.

Imagine that interest rates on new loans were lower than rates in the previous period, perhaps because marketplace lenders must compete with new entrants who threaten to undercut them. In this case, some borrowers might get a loan elsewhere and prepay their existing obligations. Other borrowers may decide to default on their existing loans because they perceive the conditions as unfair compared to those for new borrowers. Prepayments and defaults lead to a loss of interest income to lenders.Marketplace lending platforms depend almost exclusively on their credit scoring algorithms for risk management. They consider a wider spectrum of data than credit scores alone, so they often get a better picture of potential borrower behavior. Because they offer fixed interest rates, marketplace loans may become a bad investment if the interest falls below the real market interest rate. Regardless, next to predicting borrower behavior, platforms take little account of expectations of how market conditions might change. The margin between the lender and borrower is steady, but accounting considerations, such as measuring fair value, are also absent.

Fixed rates may matter little when banks pay no interest at all. Lenders will be happy to get at least some interest and pay little attention to whether it is fixed or variable. However, when the market improves, or when inflation sets in, fixed rates are a bad deal for lenders. It remains to be seen how lenders will react to this feature of marketplace loans when they find themselves locked into deals that lose money in comparison to other investment options.

Of course, one could contend that fixed rates have worked fairly well in the bond market. Because marketplace loans are similar to a corporate bond market for private lending, they might as well use the same recipe and offer fixed rates. Bond markets offer zero coupon loans, or fixed loans, where the interest rate is often lower than inflation. The difference between the bond market and marketplace loans is that in the bond market, all counterparties are professional investors who do their homework regarding profitability and risk management.

To expect the same from retail investors in marketplace loans is impossible. Even though some data and analytics are available on some of the larger marketplace lending platforms, investors will hardly have the capacity to program an advanced risk model which would allow them to price risk fully.13.2.2 Counterpartycreditrisk

Default probabilities and credit ratings often have a strong connection with spreads and expected recoveries. As discussed above, the interest rate in marketplace loans consists of the market interest rate and a credit spread. We assume that the market risk-free rate is small,4 whereas the counterparty credit spread defines the bulk of the rate in marketplace lending.5

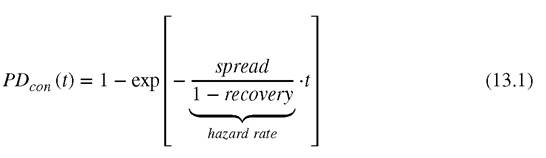

We apply intensity models, discussed in Chapter 7, to estimate the conditional default probabilities6 driven by frequency of the events arriving within time interval,

where, the first part of the exponential function implies the hazard rate of default defined by discounting the credit spreads and recovery rates, whereas the second part, i.e., t, defines the future periods.

In Chapter 7 we looked at how conditional default probabilities7 through time8 can be estimated based on a hazard rate function. In this analysis, spreads are derived from the available interest rates. The recovery rate is defined as the expected interest income earned through the interest payment cycles. Any stress in credit rating will result in a shock in credit spreads, which impacts the default probabilities through the hazard rate function. This function assumes that default probabilities (PD) of counterparties can increase exponentially from year to year, based on spreads and recoveries. It may seem overly harsh, but the degree of risk is indeed changing exponentially under stress conditions; this explains why regulators9 also require banks to assess their credit portfolios under such an assumption.

In bank loans, counterparty spreads are relatively small because they mostly lend to high-quality borrowers. However, in marketplace lending, counterparty spreads are extremely high in comparison. A 5-year low rated loan contract with a PD of 20 percent in the first year could easily reach 100 percent probability of default in the final year if we apply the hazard rate function. In marketplace lending, applying a hazard rate therefore only makes sense for stress conditions, not expected market conditions.13.2.2 Behavior

The only behavioral characteristics in our analysis are prepayment and the change of the probability of default discussed in Chapter 8. Both of these characteristics have underlying drivers. For instance, markets and idiosyncratic factors drive prepayments. Past observations indicate expected prepayment rates and times under normal and expected conditions. However, under stress conditions, prepayment rates may change in regards to the time intervals. Moreover, borrowers may use prepayments as a strategy for rolling over their loans for better conditions.

Market and idiosyncratic borrower characteristics drive changes in the probabilities of default. For lenders, probabilities of default indicate changes in the expected credit exposure and losses. Borrowers may decide to default if they recognize that their payment rates are higher than market rates and the contractual conditions have tilted against them. If the terms of an individual loan agreement diverge significantly from the terms that have become the new standard in a market, the willingness of borrowers to fulfill their obligations may deteriorate rapidly.

13.3

More on the topic RISK FACTORS:

- Diagnosis of Bovine Tuberculosis in Zambia

- Historical Perspective of BTB in Nigeria

- Allianz Research. Country Risk Atlas 2024: Assessing non-payment risk in major economies. Allianz,2024. — 179 p., 2024

- Prevention and Control of BTB in Sudan

- Diagnosis of Bovine TB in Ghana

- Conclusion and Recommendations

- The Lesions and Diagnosis of BTB in Sudan

- Other Mycobacterial Infections in Livestock and Wildlife in Tanzania

- Bovine Tuberculosis (BTB) in Cattle in Zambia

- Post-mortal Diagnosis of BTB in Nigerian Abattoirs