CREDIT EXPOSURE CONCENTRATION RISK

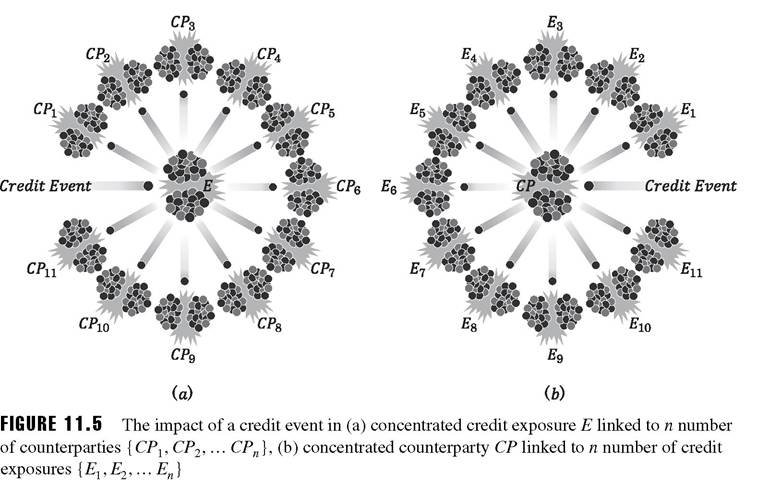

In regards to the credit exposure or cluster of exposures belonging to a single portfolio, concentration risk indicates the concentrated interlinkages and interdependencies between the following two factors:

1.

Particular exposure or cluster of credit exposures with severala. Assets or cluster8 of assets

b. Counterparties and/or cluster of them (Figure 11.5(a)).

For instance, the former case could be when a number of assets (e.g., stocks) are used as collaterals to a single or to a portfolio of exposures; in case of a defaulted exposure such assets will be under immediate liquidation which may impact their value. The latter case could be when a number of counterparties are acting as guarantors or protection sellers to a particular exposure. A default event of such exposure will impact these counterparties.

2. Several credit exposures or clusters of them, linked to particular

a. Asset or cluster of assets

b. Counterparty and/or cluster of them (Figure 11.5(b)).

For example, think of a case where several exposures are collateralized by a single asset or cluster of assets driven by a single market risk factor, e.g., gold commodity; this refers to the above first point. For the second point we could think of a case where many exposures may use a single guarantor/protection seller or cluster of guarantors belonging to the same sector. Finally, assume a more general case where exposures belong to a counterparty with the same or similar credit rating. This could be the case in marketplace lending, especially when ratings converge under stress.

In regards to credit risk analysis, we focus on the default and the non-default but downgrading events of the concentrated elements. In such credit events, the concentrated exposure

will have a direct impact on the concentrated assets and/or counterparties that are directly linked to each other. Thus, all linked counterparties and assets will be impacted directly; for instance where they are used as credit enhancements, they will have to cover the losses of the credit event. A simple way to measure the concentrated risk in regard to credit exposures is by applying the formula9 as defined in 11.1. H fluctuates between 0 and 1 indicating well diversified and highly concentrated exposures respectively.

In a credit event applied to concentrated asset or counterparty there will be expected losses in the credit exposures that they are linked to. This may be due to a loss in value of the exposure.

The total losses in both cases can be significant and will depend mainly on the type of the event, value of the exposures, the number of the links and the possible systemic risk that may result.

11.5