EVOLUTION OF THE GROSS AND NET EXPOSURES

Credit exposure can be estimated based on the current market, counterparty credit and behavior conditions. The value of credit exposures, over time, is not static, either at single contract or at credit portfolios levels.

In fact, the future credit exposure is a time-sensitive measure. Thus, an important consideration for managing credit portfolios is modelling and estimating the evolution of credit exposure over time.Different analysis elements drive the evolution of credit exposure, for instance:

■ Evolution of market conditions.

■ Counterparty credit status.

■ Behavior.

■ Type of contract.

■ Valuation principles.

■ Strategies.

The evolution of market conditions will impact the value of the contract at future, default, or trading time; for instance the present value of a variable loan is driven by the future interest rates. Moreover, market conditions will impact the value of market based credit enhancements, e.g., stocks, commodities, etc. and thus will modify the future net exposure accordingly. The expected potential exposure at future time t can be estimated based on its sensitivities to underlying risk factors. A general function for defining such sensitivity is shown in 9.2. The evolution of these factors should be derived using what-if or Monte Carlo simulation techniques, which are based on real-world expectations as discussed in Chapter 6.

where

VE is the value of the exposure,

RF is the underlying risk factor,

orf is the volatility of the risk factor within a time horizon, and

p is defining the confidence interval.

The counterparty credit status has some probability of change at future time(s). A counterparty downgrading will change the value of the traded exposure as well as any counterparty based credit enhancement; for instance, in the case of the guarantor having a lower credit rating than the obligor, the particular credit enhancement will entirely lose its applicability impacting directly the net exposure.

The sensitivity of the potential future exposures, in absolute terms, to counterparty credit risk factors, e.g., PD is given by the equation 9.3.

The behavior of the obligor may change the exposure in financial contracts when for instance options can be exercised, e.g., prepayments, use of credit lines/facilities (see Chapter 8) etc., as well as recoveries may be expected after the default event. A prepayment at future PIT will change the remaining exposure; moreover, the use of facilities based on liquidity needs will also impact the credit exposure. Note that when such usage is exercised to avoid a default event, it will dramatically increase the overall exposure and credit losses. In the defaulted contracts, the actual recovery will drive the net exposure and credit losses.

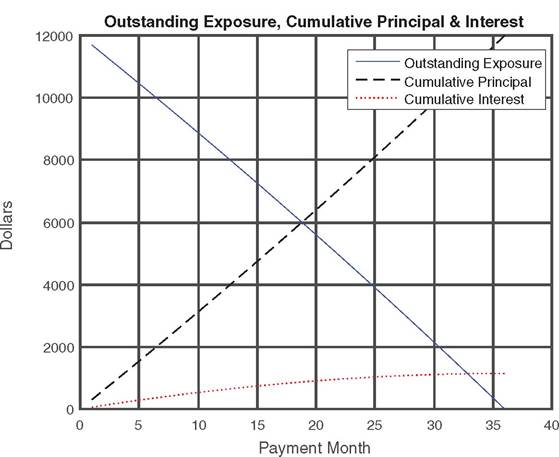

FIGURE 9.2 Evolution of credit exposures concerning principal and interest payments in annuity contract

Depending on the valuation principles applied to exposures and credit enhancements the future exposure may change. Thus, by applying mark-to-market, fair value, amortized cost, historic/write-off at the end, etc. will obviously result in different values of the exposure.

The type of contract which sets the evolution of principal plays an important role in exposure evolution. Consider, for instance, a loan contract, e.g., used in a project, where the principal will be provided according to the project schedule. The exposure could follow the corresponding project cash flow patterns and be mapped as discussed in Chapter 5 and illustrated in Figures 9.2 and 9.3, i.e., it increases till the completion of the project and reduces by paying back the principal until the maturity.

In the annuity type the interest and principal payments are reduced and increased correspondingly during the lifetime of the contract.

As illustrated in Figure 9.2 the exposure and expected losses are reduced accordingly.The exposure of a credit portfolio is very much driven by the strategies applied during the rollover process. In a portfolio, some contracts mature, some others default or downgrade. Portfolio managers decide about their reinvestment or replacement, i.e., new types of contracts, defining therefore the evolution of the portfolio. The absence of old contracts and the appearance of the new ones will therefore impact the credit exposure of the portfolio overall.

Finally, credit exposures can be changed according to strategies for the limits used to minimize the expected credit losses.

Based on the above, both gross and net credit exposures may change through time, e.g., from t0 to tn, as illustrated in Figure 9.3. Imagine the case of a variable interest loan used for a construction project. The nominal value of the loan is agreed between the lender and the borrower. The principal, however, will be provided at future times based on the project needs, e.g., at each project phase capital is needed and thus the exposure rises accordingly.

FIGURE 9.3 Evolution of credit exposures

In other words, the behavior (project need) is driving the evolution of the gross exposure. After the completion of the project the borrower pays back the principal capital, plus the interests, reducing the outstanding credit exposure. The borrower may also decide to prepay a percentage of the outstanding principal amount. The value of the contract also changes according to market conditions. Moreover, the physical collateral in this exposure is the actual building. The value of this collateral is driven by the phase of the project as well as the market conditions defining the corresponding market price. Any changes in the value of the collateral will modify the net credit exposure.

9.4