EXPOSURE DISTRIBUTION

The evolution of the credit exposure through time is not static as it is very much driven on analysis elements as mentioned above. However, there is no certain known path for such exposure evolution.

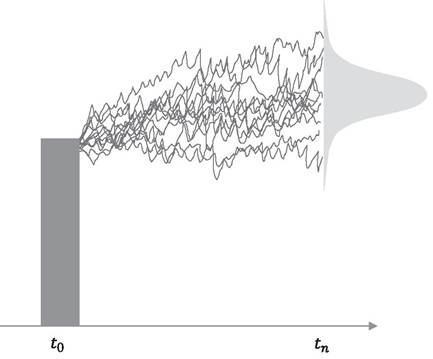

In fact it depends on the future performance of the underlying parameters of these elements. For instance the performance of the market and counterparty credit risk factors will impact both gross and net future credit exposures.A good way to identify the different possible paths of the credit exposure is to define a number of scenarios referring to the risk factors. Such scenarios are usually simulated, resulting in a distribution of the possible exposures at future time t as illustrated in Figure 9.4. Based on such distribution the Expected Exposure (EE) is estimated based on the mean (average) of the distribution of exposures at any particular future dates, defined by the simulation time intervals.

Typically, the expected exposure value is to consider many future dates up until the longest maturity date of the underlying instruments. Thus, a calculation of an expected exposure requires thousands of paths by simulating many future scenarios of risk factors for the given

FIGURE 9.4 Evolution of credit exposures based on several scenarios

contract or portfolio. Once a sufficient set of scenarios has been simulated, the contract or portfolio can be priced on a series of future dates for each scenario. The result will be a matrix, or “cube,” of contract values. The prices are converted to exposures after taking into account credit enhancements, e.g., collateral agreements as well as netting agreements where the values of several contracts may offset each other, lowering their total exposure.

The expected exposure is one of the main parameters in the calculation of the value adjustments of the credit portfolio as well as in the estimation of the expected credit losses, discussed in the next paragraphs.

There are more types of exposures that can be estimated based on the expected exposures, e.g., peak exposure PE, effective exposure EE, expected positive exposure (EPE), effective EPE, etc., which serve different purposes for measuring credit exposures. For instance, PE is a high quantile within the expected exposure distribution based on a certain confidence level, e.g., 99% at any particular future date which clearly is used in risk measurement.

9.5