Innovation the mesin fintech

The following paragraphs give an overview of the main innovation themes.

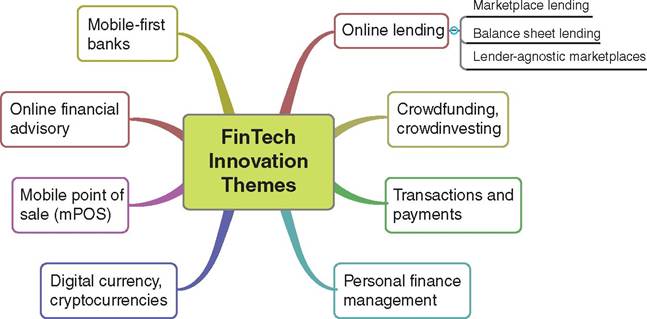

1.1.1 Online lending

Online lending is about creating a platform for borrowers to access loans outside the established credit system.

Lenders are often individuals or professional investors such as funds and institutions. Authors Karen Gordon Mills and Brayden McCarthy identify three kinds of

FIGURE 1.1 Innovation themes in FinTech

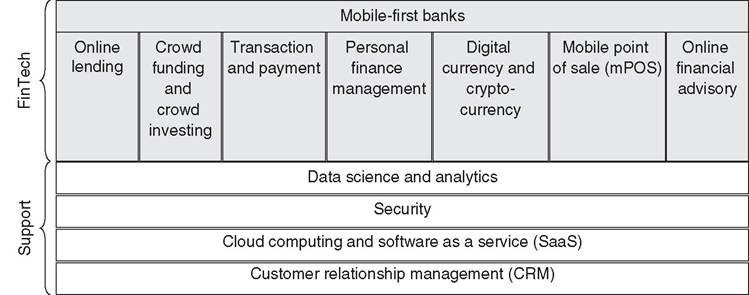

TABLE 1.1 The main innovation themes in financial technology

| Sector | Description Business model |

| Online lending | Lending to borrowers outside the established Credit against interest, credit system, either for small businesses or lead generation, fees consumers; Includes several approaches to and commissions lending, such as balance sheet lending, P2P/marketplace lending, or lender-agnostic marketplaces |

| Crowdfunding and crowdinvesting | Raising funds from backers in exchange for Capital or debt against rewards, debt, convertible debt or equity equity, fees and commissions |

| Transactions and payments | Cashless payment processing, involving credit Credit against interest, cards or proprietary systems; Store of value service against fees on the cell phone or smartphone, either in official currency or credits (phone credits) |

| Personal finance management | Allows users to consolidate their financial Annual subscription fee, statements, net worth, banking cross-selling relationships, credit cards, and so on |

| Digital currency and cryptocurrency | Alternative stores of value to established Bitcoin mining, trading currencies, many of them encrypted, so exchanges transfers are without a trace and anonymous |

| Mobile point of sale (mPOS) | The ability to process payments with credit Service against fees, credit cards or contactless with a smartphone and against interest a credit/debit card reader |

| Online financial advisory | Automated portfolio management and Service against fees optimization according to a client mandate, also called “robo-advisory” |

| Mobile-first banks | Branchless banks that process all client Service against fees, credit interactions and services through a software against interest storefront |

online lenders: online balance sheet lenders, peer-to-peer transactional marketplaces, and lender-agnostic marketplaces.1 Chapter 2 describes all three of them in detail.

Online lending is one of the most promising segments of FinTech and potentially the most disruptive, with large amounts of venture capital pouring into existing and newly emerging platforms.1.1.2 Crowdfunding and crowdinvesting

Crowdfunding describes raising capital for ventures or projects by collecting contributions from different individuals via the internet. Every crowdfunding project consists of at least three parties: the project initiator, backers who fund the project, and a platform that facilitates transactions. In 2013, the crowdfunding industry grew to be over $5.1 billion worldwide.2 Different kinds of crowdfunding exist. In reward-based crowdfunding, entrepreneurs either pre-sell a product to customers without giving up equity or they are selling debt. Equity-based crowdfunding (also called crowdinvesting) describes the case where a backer receives unlisted shares of a startup in exchange for cash. Both terms are often used interchangeably, but they describe different approaches. Crowdinvesting can also entail funding with debt or convertible debt. In either case, crowdinvestors receive a residual financial claim of future cash flows in a startup, while crowdfunders don't.

1.1.3 Transactionsandpayments

Since its very beginning, the internet has facilitated commercial transactions. According to author John Markoff, the first e-commerce transaction took place when students at Stanford University and MIT used Arpanet accounts to quietly arrange the sale of an undetermined amount of marijuana in 1971 or 1972.3 Likewise, e-commerce solutions that allowed credit card processing online are hardly a novelty. However, enabling online transactions and payments without needing a credit card, or making the service available to individuals and small businesses without the need of an expensive IT infrastructure, is relatively new. PayPal, one of the first providers of mainstream online payments, boasts 152 million user accounts at the time of this writing.

Its total value of transactions in Q2 2014 was $55 billion.4Mobile payments (also called mobile money, mobile money transfers, or mobile wallets) are payment services via a mobile phone. Although the concept of online payment has a long history, the technology to support such mobile payments and wallets has become widely available recently with the proliferation of smartphones. Online companies like PayPal, Amazon Payments, and Google Wallet also have mobile options. Large potential for mobile payments exists in the developing world. For example, Vodafone's M-Pesa, a mobile-phone based money transfer service, launched in 2007 in Kenya and Tanzania. It allows users with a national ID card to deposit, withdraw, and transfer money easily with a mobile device. M-Pesa has since expanded to Afghanistan, South Africa, India, and Eastern Europe.5 People use such services often for micropayments. Mobile payments have a large potential to extend financial services to “unbanked” people, estimated at up to 50 percent of the world's adult population.6

1.1.4 Personal Financial Management

Personal Financial Management (PFM) describes software or online services that help people manage their finances. PFM lets users categorize their transactions and add different accounts from banks or credit card processors into a single view. Services often include data visualizations such as spending trends, budgets and net worth. One of the first pieces of PFM software available was Intuit's Quicken. Online startups entered the field in 2006, with Mint on the vanguard (acquired by Intuit in 2009). Several competitors offer comparable services free of charge, including the calculation of personal finance scores based on how well people manage their money. Some startups in the field also aim at helping users manage their debt.

1.1.5 Digital currency and cryptocurrency

Digital currency describes a medium of exchange that is electronically created and stored, as an alternative to physical currencies, which exist in the form of banknotes and coins.

Digital currency can buy physical goods and services like traditional money, or the currency may be valid only inside an online game or a social network. Such restricted currencies are also called virtual currencies. Because they rely on the transmission of code across the internet, digital currencies promise a fast, secure, and inexpensive method of wealth transfer, independent of existing payment systems and banks. A subset of digital currencies are cryptocurrencies, where transactions are recorded, time-stamped, and displayed in a public ledger, called the “block chain.” Public-key cryptography ensures that all computers in the network have a constantly updated and verified record of all transactions within the Bitcoin network, which prevents double-spending and fraud.7 What irks governments about cryptocurrency is its decentralized control: the entire cryptocurrency system creates new currency in a “mining” process at a defined and publicly known rate. In centralized banking, such as the Federal Reserve System, governments control the supply of currency by printing units of fiat money or demanding additions to digital banking ledgers. Because governments cannot produce units of cryptocurrency they have no influence on its supply, which results in the loss of an important policy tool. Bitcoin emerged in 2008 as the first fully implemented cryptocurrency,8 but several hundred other cryptocurrencies and digital currencies exist.1.1.6 Mobile point of sale (mPOS)

A mobile point of sale is a smartphone, tablet or other wireless device that serves as a cash register to process payments. It allows individuals and small business owners to accept transactions without having to buy an electronic register or pay a traditional vendor such as Visa or Mastercard to supply a card reader and processing software. Any smartphone or tablet can become an mPOS with a downloadable mobile app. When installing the app, the user normally receives a card reader in the mail that plugs into the audio socket of the device.

Some providers even offer additional devices that can print receipts. Every smartphone user can thus become a professional vendor with minimal fees and overhead.1.1.7 Onlinefinancialadvisory

Online financial advisors (also called robo-advisors) are financial advisory firms that provide automated portfolio management while relying on limited human intervention, which results in lower fees for account holders. Robo-advisors do not fully automate portfolio management: financial professionals make forecasts for investment performance of portfolio assets, so the investment strategies vary between different online advisors. However, for account management functions such as portfolio optimization, tax harvesting, or rebalancing, robo- advisors depend on similar algorithms. Among them are modern portfolio theory (MPT), or strategies to derive market assumptions such as the Black-Litterman model or the Gordon growth model.9 Such algorithms have found wide application in conventional financial advisory firms for years. The novelty of robo-advisors is that they offer comparable financial services, rigorous mathematical models, and similar performance to established account managers but at a lower cost. In a robo-advisor, a small team with comparatively small overhead may compete with large wealth management divisions of established banks.

1.1.8 Mobile-first banks

Characteristics of mobile-first banks (also called mobile banks) are the absence of physical branches, transparent conditions, no minimum account balance requirements, and free service. Clients can open accounts quickly and securely, and they can manage their financial affairs online or on a mobile app without ever setting foot in a branch. Account balances are still held in a partnering bank that has conventional branches, but this partner bank exists entirely on the backend. Mobile-first banks may combine several FinTech services under one umbrella. The promise of mobile-first banks is that online services may gradually encroach on the business of traditional banks, to the point where mobile-first banks will challenge existing banks offline.

An example of a mobile bank is Simple. Banco Bilbao Vizcaya Argentaria (BBVA), a Spanish banking group, acquired Simple in early 2014, when the startup had 100,000 customers. Users feared that the acquirer would shut down Simple's operation and merge its accounts into its existing business, but BBVA knew better. Instead of integrating Simple into its existing operations, BBVA states that its goal is to take advantage of a different way of thinking that the startup has achieved, namely how it has changed consumer behavior and engagement. Users of Simple conduct banking in a distinctly different way from traditional banking. About 25 percent of customers post pictures or tag transactions, like on a social network.10 With Big Data and social network analysis (SNA) making forays into credit scoring, owning the platform could prove helpful for banks when assessing the quality of borrowers in the future.111.1.9 Adynamicandfragmentedspace

What becomes apparent is that the term FinTech is dynamic and evolving. Startups in the space offer a wide variety of services, from tools for retail customers to consolidate financial data to complex analytics for investment funds. Many of them blend several innovation themes, such as online transactions, mPOS, and mobile wallets. The approach to doing business varies widely between different FinTech companies: a startup producing a CRM system for banks may have a completely different culture and different customers than a disruptive cryptocurrency venture in Silicon Valley. Without trying to complicate the discussion, it is clear that FinTech is dynamic, fragmented and complex. At the same time, the classification by innovation theme from Table 1.1 and Figure 1.2 allows us to structure the discussion about the financial technology landscape. Because the focus of this book is marketplace lending, it is important to separate this segment from the others. Startups in the online lending space may still service several innovation themes at the same time and, if they do, we will recognize it by overlaying the classification we established.

FIGURE 1.2 The main financial technology innovation themes and their supporting technologies in relationship with each other

1.2