THE PROMISES AND PITFALLS OF FINTECH BUSINESS MODELS

Now that we know the main sectors and innovation themes in FinTech, we can group them by other attributes as well. FinTech companies take different approaches to disrupt the financial sector.12 We may separate them into business models with a higher chance at disruption and those less likely to succeed.

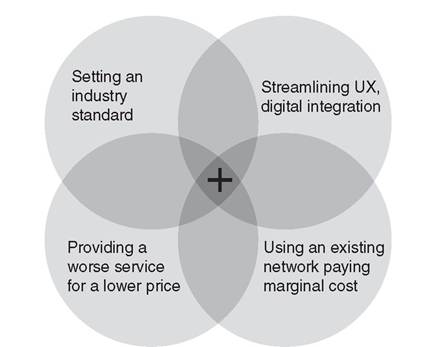

We begin by describing four business models with a better chance at disrupting the status quo. There are certainly more, but the ones we discuss here include streamlining the user experience (UX) and digital integration, setting an industry standard that the financial industry previously failed to get off the ground, using someone else's network while only paying marginal cost, and providing a worse service to customers at a lower price.13 These business models overlap, as Figure 1.3 shows.

FIGURE 1.3 FinTech business models with high disruptive potential

1.1.10 Streamlining the user experience (UX) and digital integration

Banks have been notoriously slow to bring their services into the digital age. Even though most banks offer internet banking and mobile banking, loan application and decisioning are still miles apart from the ease of use and convenience that consumers appreciate in online services. Banks are hardly a cozy place to visit, and the mistrust between banks and the general public is hard to overcome. On the other hand, FinTech has the air of “new, cool and pure,” and streamlining the user experience is one of the main selling points of FinTech services. Their interfaces are slick and clean, and they give users control of the experience at all times. Some mobile-first banks resemble more a social network or messaging service than a financial institution. Taking the pain and tedium out of banking is a huge niche that still has much room to grow, especially in payments and lending.

1.1.11 Setting an industry standard that the financial industry failed to get off the ground

Even though banks have global transaction networks, they often insert unnecessary steps in global transactions that reduce speed and ease of the customer experience at an additional cost. For instance, the reason an international bank transfer takes five business days is hardly that it takes money that long to travel around the globe. By holding money for several days before they transfer it into a recipient's bank account, banks get credit for free, which they can lend out for a fee. Customers have less and less tolerance for such shenanigans, and some FinTech companies have proven that money transfers can be instant. Whenever a startup manages to improve a financial service by orders of magnitude, this should be a wake-up call to banks. Much less because it is a new way of doing business, than because the established incumbents could have easily implemented it themselves had they made an honest effort at improving the service for their customers.

1.1.12 Using someone else's network while only paying marginal cost

Many FinTech companies depend on existing infrastructure that is often in the hands of incumbents in the financial sector. Online lending is an example, and so are payments. It seems surprising that the owners of the existing financial networks allow small companies to use them to offer competing services. The reason this is possible is that regulators seem to be keen on encouraging competition and entry in financial services markets. Several FinTech companies undercut incumbents for payment services. Even though they might compete in the short term, they actually stand a good chance for an acquisition later down the road. Customers love to pay less for a similar service, so paying only marginal cost plus a small fee can be a successful business model for new entrants in financial services.

1.1.13 Providing a worse service to customers at a lower price

Unbundling services that banks provide can be a viable business model for FinTech companies. Some customers may wish to pay for only a small segment of the bundled product offering that banks sell for a high price. The discount brokerage industry is an example for successful execution of this approach. Even though their service is more limited than that of a fullservice broker, it is still good enough for many customers. This has allowed online brokerage to become the industry standard that has severely disrupted traditional brokers. Customers often have no need for up-market innovation that the incumbent provides. Instead, they want something new that gives them a similar experience for a lower price. In essence, this is the promise of disruptive innovation, and it seems to be one of the most promising approaches in FinTech.

1.3