Introduction

Whereas the preceding chapter considered the deflationary damage exerted by an artificially overvalued exchange rate in the 1930s, Taiwan’s experience at the end of the 1940s offers a vivid illustration of the inflationary pressures that can be generated by an excessively undervalued exchange rate.

Resisting upward pressure on the currency in such a case fuels inflation, inter alia, as undervaluation of the domestic currency triggers capital inflows that drive up the money supply. As discussed in Chapter 1, there were fears that central bank loss of control over the money supply in the face of surging capital inflows would lead to this scenario being repeated in mainland China in 2004. “Hot flows” of funds into China appeared to subside in the face of the gradual appreciation effected during 20052007, however, and the actual degree of recent renminbi undervaluation remained subject to considerable doubt (Chapter 1). China’s accelerating accumulation of foreign exchange reserves has nevertheless required massive sterilization efforts by the People’s Bank of China (Chapter 4), and ongoing concerns about imported inflationary pressures prompted a variety of tightening measures, including a succession of reserve requirement increases and interest rate hikes. This chapter uses an example from China’s own history to demonstrate how dangerous such imported inflation can be - albeit under circumstances far more extreme than anything that is likely to unfold today.During the twilight of Nationalist rule in mainland China in 1947-1949, there was a large outflow of funds from mainland China to Taiwan as excess money supply growth on the mainland was translated into excess money growth in Taiwan. A fixed exchange rate between mainland China’s new “gold yuan” and Taiwan’s currency, coupled with Nationalist control over both the Central Bank of China and the Bank of Taiwan, created an almost ideal vehicle for massive capital flight.

Rising capital inflows into Taiwan reflected not only the deteriorating conditions on the mainland but also excess money growth that had, as a major outlet, the exit strategy offered by the fixed exchange rate imposed by Chiang Kai-shek’s Nationalist regime. Holders of gold yuan took advantage of the fact that the Bank of Taiwan was forced to accept the weakening Nationalist currency and exchange it for the separate Taiwanese currency at an artificially overvalued rate - that is, seriously overvaluing the gold yuan while undervaluing the Taiwanese currency. Indeed, the worse conditions became on the mainland, the greater the incentive to capitalize on the fixed exchange rate and move funds into Taiwan.One way of assessing the magnitude of the overvaluation of the gold yuan against the Taiwanese currency is to consider how the gold yuan fared in black market trading. On October 15,1948, the US Ambassador to China, John Leighton Stuart, observed that the US dollar was exchanging for 16 gold yuan in Beijing even though the official rate was only 4:1 - whereas an ounce of gold was selling for 1,000 gold yuan, similarly up dramatically from the official rate set at 200 gold yuan per ounce.[94] The fixed rate of exchange with the Taiwanese currency remained available through the fall of 1948, however, in spite of rapidly accelerating money growth on the mainland reflected in the plunging black market currency values. The resultant exporting of hyperinflation to Taiwan suggests that the policies of

Table 6.1. NationalistGovernmentFinances, 1936-1949

| Expenditure | Revenue | Budget Deficit | Note Issue Outstanding | |

| 1936-1937 | 1,894 | 1,972 | -78 | 1,410 |

| 1937-1938 | 2,091 | 815 | 1,276 | 1,730 |

| 1939 | 2,797 | 740 | 2,057 | 4,290 |

| 1940 | 5,288 | 1,325 | 3,963 | 7,870 |

| 1941 | 10,003 | 1,310 | 8,693 | 15,100 |

| 1942 | 24,511 | 5,630 | 18,881 | 34,400 |

| 1943 | 58,816 | 20,403 | 38,413 | 75,400 |

| 1944 | 171,689 | 38,503 | 133,186 | 189,500 |

| 1945 | 2,348,085 | 1,241,389 | 1,106,696 | 1,031,900 |

| 1946 | 7,574,790 | 2,876,988 | 4,697,802 | 3,726,100 |

| 1947 | 43,393,895 | 14,064,383 | 29,329,512 | 33,188,500 |

| Jan-July 1948 | 655,471,087 | 220,905,475 | 434,565,612 | 374,762,200 |

| Aug 1948 | - | - | - | 890,400,000 |

| Sept 1948 | 1,030,242,000 | 326,562,000 | 703,680,000 | 3,606,000,000 |

| Oct 1948 | 848,499,000 | 435,270,000 | 413,229,000 | 5,550,000,000 |

| Nov 1948 | 2,024,832,000 | 517,230,000 | 1,507,602,000 | 10,182,000,000 |

| Dec 1948 | 7,948,827,000 | 1,340,241,000 | 6,608,586,000 | 24,960,000,000 |

| Jan 1949 | - | - | - | 62,466,000,000 |

| Feb 1949 | - | - | - | 178,932,000,000 |

| Mar 1949 | - | - | - | 588,207,000,000 |

| Apr 1949 | - | - | - | 15,483,720,000,000 |

Notes: All numbers are given in millions of fapi. Data from August 1948 forward have been converted by applying the official three-million-to-one exchange rate between fapi and the gold yuan.

Note issues outstanding are end-of-period values.Sources: Chang (1958, pp. 16, 40, 51, 71, 84, 124, 168); Wu (1958, p. 122); and authors' calculations.

Nationalist leader Chiang Kai-shek might well have the dubious, and quite possibly unique, honor of being responsible not just for one hyperinflation but rather for two. The initial hyperinflation in mainland China was itself fueled by wartime expenditures, with the Sino-Japanese War that began in 1937 melding into World War II and then, with no respite, an escalating civil war against the Communist forces of Mao Tse-tung. The associated massive budget deficits and increasing reliance on the printing press are clearly evident in Table 6.1 However, it is the interrelationship between inflation in mainland China and inflation in Taiwan that adds a most unusual, and novel, twist to this hyperinflation experience. Capital inflows from mainland China played a key role in the process by which Taiwan's resources and the Bank of Taiwan's printing press were used to help finance the failing Nationalist war effort.

Formal tests of how Taiwan's inflation was affected by events on the mainland have been surprisingly sparse. However, the single study by Lin and Wu

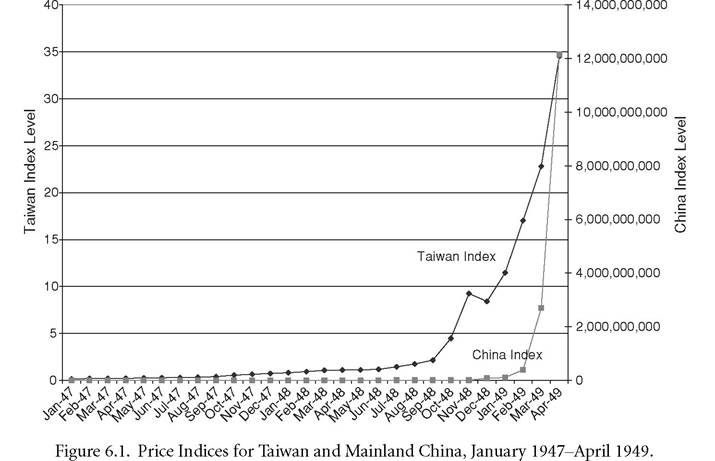

(1989) does find that mainland inflation (as measured by the inflation rate in Shanghai) Granger causes Taiwanese inflation over the January 1946- April 1949 period.[95] This chapter assesses both the importance of mainland Chinese variables to Taiwan’s inflation and the effects of capital inflows from mainland China to Taiwan over the 1947-1949 period. We also allow for a structural break following the monetary reform in mainland China in August 1948 that is thought to have spurred capital inflows and inflationary pressures in Taiwan.[96] The acceleration in Taiwanese prices following this reform is shown in Figure 6.1, which plots Taiwan and mainland China price movements over the 1947-1949 period (based on wholesale price indices from the cities of Taipei and Shanghai). Our empirical work confirms the importance of the August 1948 reform to Taiwan and shows Taiwanese inflation rates to be significantly affected by capital inflows and mainland China inflation and money growth rates. Taiwanese money growth is itself driven by such external factors, leaving it with no apparent independent role in the inflation process.