Imported Inflation and Mainland China’s Currency Reform

Taiwan was returned to Chiang Kai-shek’s Nationalist government by the Japanese on November 1, 1945. The Bank of Taiwan then set up a special deposit program to withdraw the old Japanese notes and prohibited the circulation of notes issued after the Japanese surrender.

By the beginning of December 1945, the money issued had decreased 20% from the level in October and this deposit program seemed to be effective in reducing the pressure to print money for deficit finance. However, the Bank of Taiwan was soon faced by new loan demands from China’s Nationalist Government. In May 1946, the loans debited to the Taiwan Provincial Government equaled 62.8% of the Bank of Taiwan’s total loans. On May 22, 1946, the Bank of Taiwan was authorized by the Nationalist Government to issue a new local currency, called the taipi, in an amount equivalent to 5.3 billion fapi. There were no reserves for the taipi and its circulation was limited to Taiwan with issuance remaining subject to Nationalist government approval. Makinen and Woodward (1989, p. 91) state that, after this point, “the public finance practices of the Taiwanese government paralleled those on the mainland in that a major source of revenue was derived from the inflation tax.” Not only did the Bank of Taiwan face the huge burden of financing the expenses of two governments (the Taiwanese Provincial government and the Nationalist government on the mainland) but also loans to the government were augmented by unsecured loans to state-owned enterprises (Lin and Wu, 1989, pp. 932-933).The monthly rate of inflation gradually increased during 1947 and early 1948 before accelerating dramatically in the second half of 1948 to over 107% in October and November. This dramatic change was a direct consequence of the August 19,1948, monetary reform in mainland China that replaced the old fapi currency with the “gold yuan” as the official currency on the mainland.

Under this reform, private holdings of gold and silver were prohibited and all specie had to be turned into the central bank in exchange for gold yuan notes. Gold yuan notes could not be converted back into gold, however, and even the promised partial gold backing evaporated as increasingly large note issues were undertaken well in excess of the promised 2 billion yuan maximum.Prices and exchange rates in mainland China were initially frozen at the August 19 levels, and extreme penalties were adopted against hoarders and black marketeers. In Shanghai, Chiang Kai-shek’s eldest son stringently enforced these restrictive measures using the secret police. However, the government’s perilous financial and military position fueled everincreasing inflationary pressures. Losses to Mao Tse-tung’s Communist forces had severely disrupted production and transportation and depleted the government’s tax revenue. Spurred also by rising military spending, the budget deficit rose from 29 thousand billion fapi in 1947 to 434 thousand billion fapi in January-July 1948, while the money supply soared by 1,029% between December 1947 and July 1948 (Table 6.1). Notwithstanding the Minister of Finance’s August 1948 announcement that the budget deficit “would be reduced from 70 per cent to 30 per cent of government expenditure” (Chang, 1958, p. 80), the actual reliance on deficit spending reached 75% of spending in November 1948 and 83% of spending in December 1948 (Table 6.1). It was soon obvious that there were no grounds for confidence in the new monetary standard. Whereas deposits in private banks in Shanghai initially rose after the reform, and the velocity of circulation of money declined, Chang (1958, p. 274) states that by

the end of October the index of the note issue was four and a half times that of August, price and wage ceilings were in the process of disintegration, and it was abundantly clear that inflation could no longer be contained by the expedient of the currency change...

In November the value of checks cleared in Shanghai rose to more than three times the note issue, and the velocity of circulation of money jumped nearly six times the October figure... The black-market rate of interest leapt to 120 per cent per month...Besides simply unloading unwanted gold yuan notes by purchasing goods and services, mainland Chinese sought to transfer funds to South China en route to Hong Kong.[97] However, the exchange rate arrangements adopted in August 1948 gave a special impetus to capital flight to Taiwan. Prior to August 19, the exchange rate system adopted between the fapi and taipi currencies was an adjustable (or managed) exchange rate system. OnAugust 18, 1948, the exchange rate between these two currencies was 1:1,635 (one taipi was equal to 1,635 fapi). On August 19, 1948, the exchange rate between the gold yuan notes and fapi was set at 1:3,000,000 (one gold yuan note was equal to 3 million fapi). The official exchange rate between the taipi and the gold yuan thus became 1,835:1 (1,835 taipi equal to one gold yuan note).

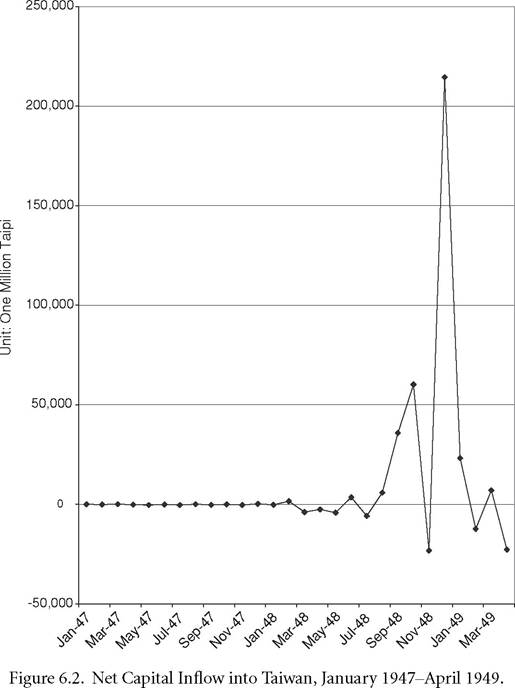

With the official exchange rate between the gold yuan and the taipi held unchanged in spite of the growing loss of confidence in the gold yuan, the attraction of exchanging gold yuan for taipi was obvious.[98] The accelerating net capital inflows into Taiwan after the August 1948 reform are depicted in Figure 6.2. Perhaps reflecting the fact that the “failure of the monetary reform seemed to be anticipated by the public” (Li and Wu, 1997, p. 7), the net capital inflow over August, September, and October 1948 amounted to close to 100,000 million taipi. This capital inflow was the major force causing the money supply to double over this same period, accounting for 86.8% of the M1 money supply increase in September 1948 and 97.9% of the October increase (Lin and Wu, 1989, pp. 935-936). The Bank of Taiwan finally stopped accepting deposits in gold yuan notes from the mainland on October 23,1948.

And, on November 1,1948, the Nationalist government belatedly adjusted the exchange rate between the taipi and the gold yuan - quickly adjusting it again on November 11. Also, from November 12, the exchange rate was allowed to change more often in response to market forces (Li and Wu, 1997). The exchange rate adjustment was accompanied by a capital outflow that grew 8.8-fold between October and November 1948 and created the first net capital outflow since the August 1948 reform was enacted. Deflation of -9.01% was recorded in Taiwan during December 1948, showing how sensitive inflation rates were to the Nationalist government’s exchange rate policy at that time.However, Taiwan’s respite at the end of 1948 was short-lived. Capital flight to Taiwan reaccelerated in the face of the Nationalists’ crumbling military position on the mainland and the Nationalist government itself began to transfer its remaining resources to Taiwan. In the face of mounting deficits on the mainland, the 2 billion yuan maximum for the gold yuan notes was formally set aside on November 11, 1948. Meanwhile, the price controls in Shanghai unraveled during the middle of October 1948 in the midst of panic buying when retailers “withheld their goods from sale rather than sell them at official prices, and even the restaurants refused to do business” (Chang, 1958, p. 80). Prices were formally freed on November 1,1948 under a Financial Emergency Executive Order. Although nearly 3.4 billion gold yuan (equivalent to more than 10,182 thousand billion fapi) were in circulation on November 30, 1948, by the end of April 1949 total note issue had risen to more than 5 thousand billion gold yuan (equivalent to a staggering 15,483,720 thousand billion fapi - see Table 6.1). Shanghai wholesale prices rose 59,374 times between September 1948 and April 1949 before rising a further 85 times between April and May 1949 on the eve of the fall of that city to the Communists on May 27, 1949.

On July 3, 1949, the director of the People’s Bank of China at Shanghai claimed that the total issue of gold yuan notes had actually reached 60,000 billion on May 25, 1949 - equivalent to 180,000 quadrillion fapi, or 11.6 times larger than the April 1949 figure given by the Nationalist central bank (Table 6.1).

Although not coming close to the inflationary spiral under the Nationalists, the Communist takeover still saw the beleaguered city of Shanghai endure a further tenfold increase in wholesale prices before stabilization was finally achieved in March 1950 (Chapter 3). Although Nationalist forces remained on the field in mainland China until 1950, Chou (1963, p. 27) states that after the fall of Shanghai “the gold yuan notes were rejected by the public.” Attempts to replace the gold yuan notes with a new “silver yuan” standard on July 1,1949 were an utter failure. Reportedly, the budget deficit in the second half of 1949 totaled 88% of expenditures - a deficit that “had to be met with gold, silver, and foreign exchange since bank notes no longer enjoyed the people’s acceptance” (Chang, 1958, p. 169).Taiwan’s November 1948 net capital outflow of -23,277 million taipi reversed to a capital inflow of 214,495 million taipi in December 1948. And this December capital inflow amounted to 73.4% of the total increase in currency in that month (Li and Wu, 1997, p. 8).[99] The Taiwanese money supply grew 1.27-fold between November and December 1948. Pressures on the money supply increased when many divisions of the Nationalist army began moving to Taiwan in 1949. The overall growth rate of the money supply increased to 37.3% in January 1949 and then, after settling back to 8.4% in February, rose again to 19.5% in March, 17.2% in April, and 39.5% in May. Inflation reaccelerated during this period, reaching 36.2% in January, 48.7% in February, 33.9% in March, 51.4% in April, and 102.1% in May. This increase, however, still paled in comparison to the depreciation of the gold yuan. By late April and early May 1949, the gold yuan’s initial official exchange ratio of 4 gold yuan to the US dollar had fallen to the point that open market quotations ranged from 5 million to 10 million gold yuan per US dollar (US Department of State, 1949, p. 401).